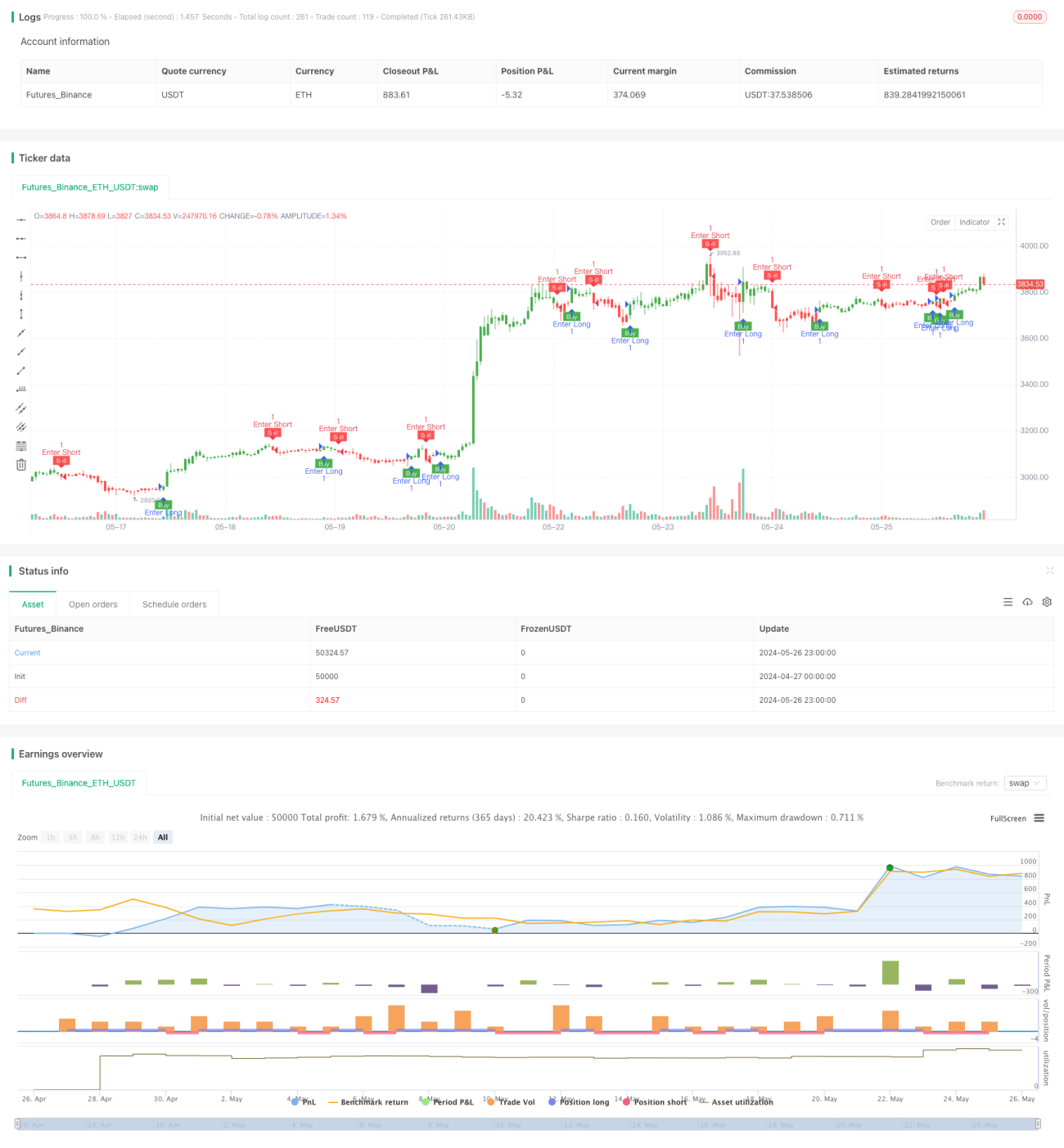

Adaptive Strategie mit dynamischem Take-Profit und Stop-Loss basierend auf ATR und EMA

Überblick

Die Strategie verwendet zwei Indikatoren: ATR (Average True Range) und EMA (Exponential Moving Average), um durch dynamische Anpassung der Stop-Loss- und Take-Profit-Niveaus an die Marktvolatilität anzupassen. Der Hauptgedanke der Strategie ist: Nutzung des ATR-Indikators zur Messung der Marktvolatilität und Festlegung der Stop-Loss- und Take-Profit-Niveaus basierend auf der Volatilität; gleichzeitig wird der EMA-Indikator verwendet, um die Handelsrichtung zu bestimmen: Wenn der Preis den EMA nach oben durchbricht, wird eine Long-Position eröffnet, bei einem Durchbruch nach unten eine Short-Position. Die Strategie kann die Stop-Loss- und Take-Profit-Niveaus automatisch an die Veränderungen der Marktvolatilität anpassen, um eine dynamische Risikosteuerung zu erreichen.

Strategieprinzip

- Berechnung des ATR-Indikators zur Messung der Marktvolatilität.

- Basierend auf dem ATR-Wert und dem eingegebenen Multiplikatorparameter wird das dynamische Stop-Loss-Niveau berechnet.

- Verwendung des EMA-Indikators als Filterbedingung: Bei einem Durchbruch des Preises über den EMA wird eine Long-Position eröffnet, bei einem Durchbruch unter den EMA wird eine Short-Position eröffnet.

- Während der Positionshaltung werden die Take-Profit- und Stop-Loss-Niveaus kontinuierlich an die Preisänderungen und die Änderungen des dynamischen Stop-Loss-Niveaus angepasst.

- Wenn der Preis das dynamische Stop-Loss-Niveau erreicht, wird die Position geschlossen und eine Gegenposition eröffnet.

Strategievorteile

- Hohe Anpassungsfähigkeit: Durch die dynamische Anpassung der Stop-Loss- und Take-Profit-Niveaus kann sich die Strategie an die Volatilitätsänderungen in verschiedenen Marktzuständen anpassen und das Risiko kontrollieren.

- Starke Trendfolgefähigkeit: Die Verwendung des EMA-Indikators zur Bestimmung der Handelsrichtung ermöglicht eine effektive Erfassung von Markttrends.

- Parameter einstellbar: Durch Anpassung der ATR-Periode und des Multiplikatorparameters können Risiko und Ertrag der Strategie flexibel gesteuert werden.

Strategierisiken

- Risiko der Parametereinstellung: Die Einstellung der ATR-Periode und des Multiplikatorparameters hat direkten Einfluss auf die Performance der Strategie; falsche Parameter können dazu führen, dass die Strategie versagt.

- Risiko in Seitwärtsmärkten: In Seitwärtsmärkten kann häufiges Öffnen und Schließen von Positionen zu großen Slippage- und Gebührenverlusten führen.

- Risiko von Trendwenden: Wenn sich der Markttrend umkehrt, kann die Strategie zu aufeinanderfolgenden Verlusten führen.

Optimierungsrichtungen

- Einführung weiterer technischer Indikatoren wie MACD, RSI usw., um die Genauigkeit der Trendbestimmung zu erhöhen.

- Optimierung der Berechnungsmethode für Stop-Loss- und Take-Profit-Niveaus, z. B. durch Einführung von Trailing-Stop, dynamischen Ratio-Take-Profit-Methoden usw.

- Optimierung der Parameter, um die beste Kombination von ATR-Periode und Multiplikator zu finden und die Stabilität und Rentabilität der Strategie zu verbessern.

- Hinzufügen eines Positionsmanagement-Moduls zur dynamischen Anpassung der Positionsgröße basierend auf der Marktvolatilität und dem Kontorisikoniveau.

Zusammenfassung

Die Strategie verwendet die beiden Indikatoren ATR und EMA, um durch dynamische Anpassung der Stop-Loss- und Take-Profit-Niveaus an die Veränderungen der Marktvolatilität anzupassen, und nutzt gleichzeitig den EMA-Indikator zur Bestimmung der Handelsrichtung. Die Strategie verfügt über eine hohe Anpassungsfähigkeit und Trendfolgefähigkeit, kann jedoch bei der Parametereinstellung, in Seitwärtsmärkten und bei Trendwenden bestimmten Risiken ausgesetzt sein. Zukünftig kann die Strategie durch die Einführung weiterer technischer Indikatoren, Optimierung der Stop-Loss- und Take-Profit-Algorithmen, Parameteroptimierung und Hinzufügen eines Positionsmanagements verbessert werden.

- 1