Doppelte-Gleitender-Durchschnitt-Crossover-Strategie mit Take-Profit und Stop-Loss

Überblick

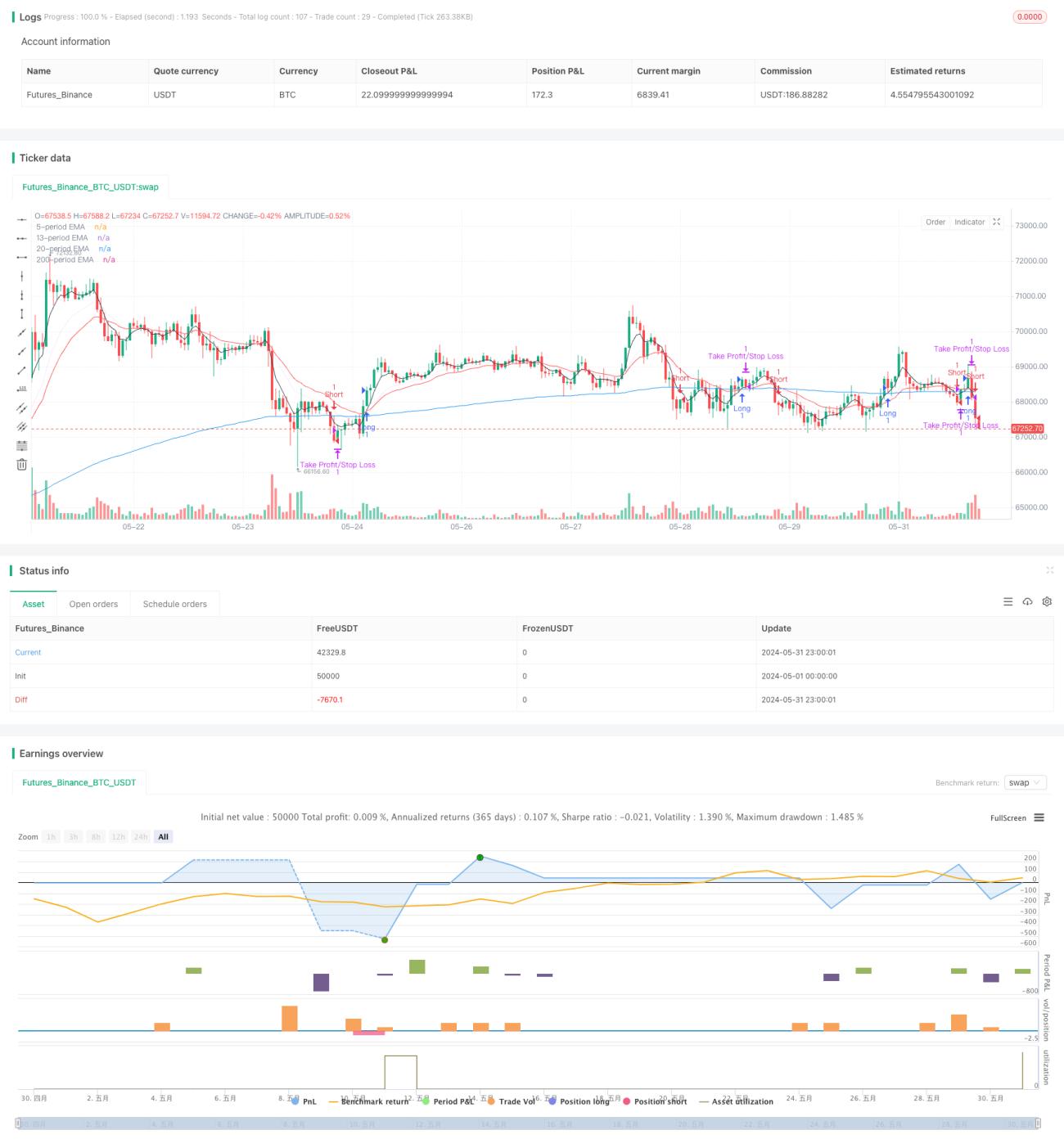

Diese Strategie verwendet den Crossover zweier exponentiell gleitender Durchschnitte (EMA) mit unterschiedlichen Perioden als Handelssignal und setzt gleichzeitig feste Punktzahlen für Take-Profit und Stop-Loss. Wenn der kurzfristige EMA von unten nach oben den langfristigen EMA kreuzt, wird eine Long-Position eröffnet; wenn der kurzfristige EMA von oben nach unten den langfristigen EMA kreuzt, wird eine Short-Position eröffnet. Bei der Eröffnung werden feste Punktzahlen für Take-Profit und Stop-Loss festgelegt, um Risiken zu kontrollieren und Gewinne zu sichern.

Strategieprinzip

- Berechnung von zwei EMA mit unterschiedlichen Perioden, standardmäßig 5 Perioden und 200 Perioden.

- Wenn der 5-Perioden-EMA von unten nach oben den 200-Perioden-EMA kreuzt, entsteht ein Long-Signal; wenn der 5-Perioden-EMA von oben nach unten den 200-Perioden-EMA kreuzt, entsteht ein Short-Signal.

- Nach der Eröffnung werden Stop-Loss-Punkte (standardmäßig 50 Punkte) und Take-Profit-Punkte (standardmäßig 200 Punkte) festgelegt.

- Wenn der Kurs das Take-Profit- oder Stop-Loss-Niveau erreicht oder die Position 200 Handelsperioden gehalten wurde, wird die Position geschlossen.

- Die Take-Profit- und Stop-Loss-Punkte können basierend auf dem Chartvolumen angepasst werden.

Strategievorteile

- Einfach und verständlich: Die Logik der Strategie ist klar und leicht zu verstehen und umzusetzen.

- Trendfolge: Durch die Trendeigenschaften des EMA können Markttrends gut erfasst werden.

- Risikokontrolle: Durch die Festlegung fester Stop-Loss-Punkte wird das Risiko einzelner Trades effektiv kontrolliert.

- Flexibilität: Die Take-Profit- und Stop-Loss-Punkte können je nach Marktvolatilität und persönlicher Risikobereitschaft angepasst werden.

Strategierisiken

- Falsche Signale: EMA-Crossover können falsche Signale erzeugen, was zu häufigen Trades und Verlusten führt.

- Trendverzögerung: Der EMA ist ein nachlaufender Indikator, der möglicherweise erst Signale liefert, nachdem sich ein Trend bereits gebildet hat, wodurch der optimale Einstiegszeitpunkt verpasst wird.

- Seitwärtsmärkte: In seitwärts verlaufenden Märkten können häufige EMA-Crossover zu einer Reihe von Verlusttrades führen.

- Fester Stop-Loss: Ein fester Stop-Loss kann sich nicht an Veränderungen der Marktvolatilität anpassen, was zu einer ungeeigneten Stop-Loss-Platzierung führt.

Strategieoptimierungsrichtungen

- Einführung weiterer Indikatoren: Kombination mit anderen technischen Indikatoren wie MACD, RSI usw. zur Erhöhung der Signalzuverlässigkeit.

- Parameteroptimierung: Optimierung von Parametern wie EMA-Perioden, Take-Profit- und Stop-Loss-Punkten zur Verbesserung der Strategieleistung.

- Dynamischer Stop-Loss: Dynamische Anpassung der Stop-Loss-Punkte basierend auf der Marktvolatilität, um sich besser an Marktveränderungen anzupassen.

- Positionsmanagement: Einführung von Positionsmanagementregeln, z. B. risikobasierte Positionsanpassung, zur Verbesserung der risikobereinigten Rendite.

- Filter: Hinzufügen von Filterbedingungen für Handelssignale, wie Volumen, Preisformationen usw., zur Verbesserung der Signalqualität.

Zusammenfassung

Die Doppel-Gleitenden-Durchschnitte-Crossover-Strategie mit Take-Profit und Stop-Loss ist eine einfach zu verwendende Handelsstrategie, die durch EMA-Crossover Handelssignale generiert und gleichzeitig feste Punktzahlen für Take-Profit und Stop-Loss zur Risikokontrolle festlegt. Der Vorteil der Strategie liegt in ihrer klaren Logik, einfachen Umsetzung und guten Erfassung von Markttrends. Gleichzeitig bestehen jedoch Risiken wie falsche Signale, Trendverzögerung, Seitwärtsmärkte und fester Stop-Loss. Optimierungsrichtungen umfassen die Einführung weiterer Indikatoren, Parameteroptimierung, dynamischen Stop-Loss, Positionsmanagement und das Hinzufügen von Filtern. Händler können die Strategie je nach ihrer Risikobereitschaft und den Marktgegebenheiten entsprechend optimieren und anpassen, um die Robustheit und Rentabilität der Strategie zu verbessern.

- 1