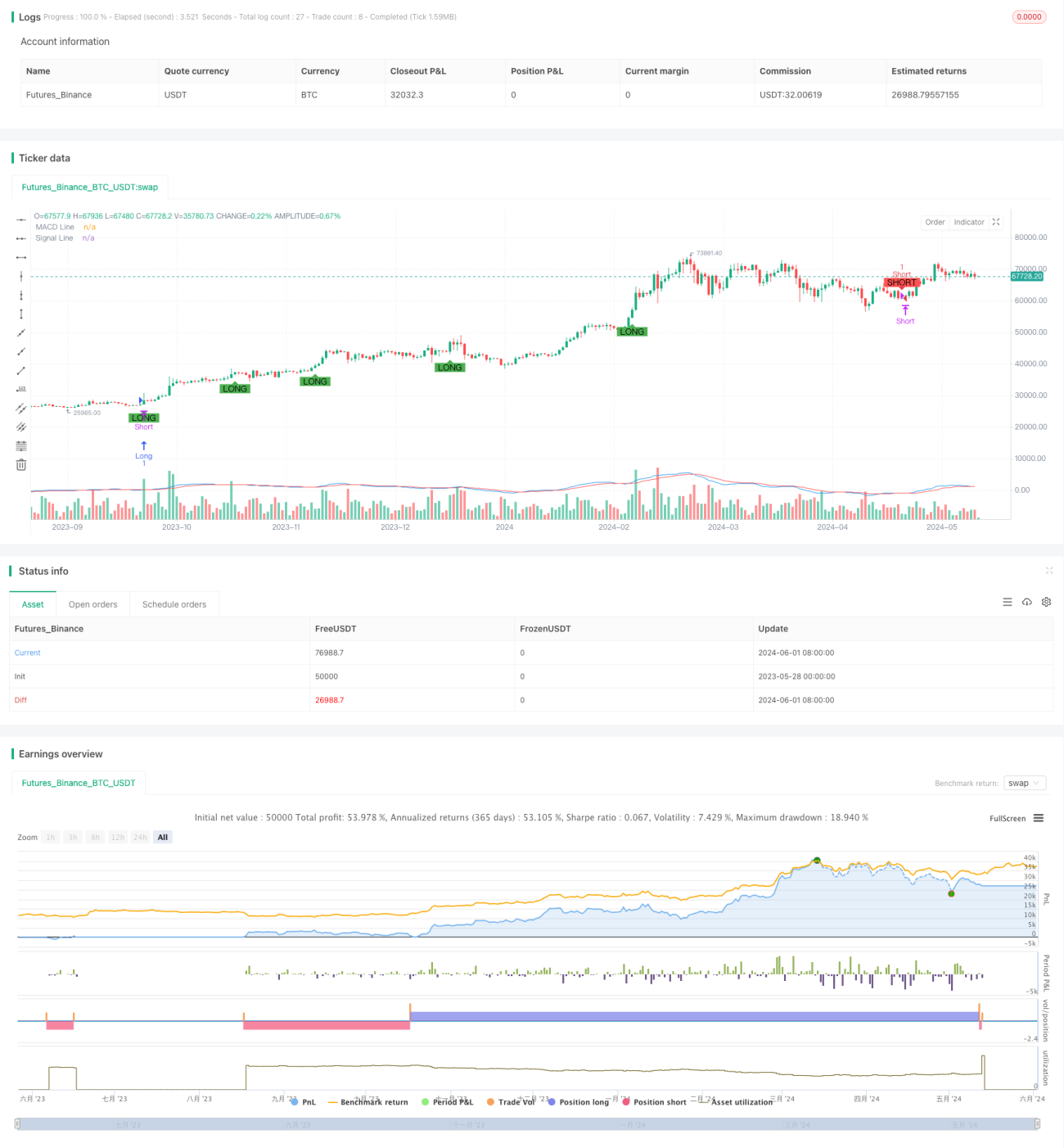

MACD und R:R-Verhältnis Intraday-Limit-Konvergenzstrategie

Übersicht

Diese Strategie basiert auf der Konvergenz und Divergenz des MACD-Indikators zur Generierung von Handelssignalen. Wenn die MACD-Linie die Signallinie kreuzt und der Wert der MACD-Linie größer als 1,5 oder kleiner als -1,5 ist, werden Long- bzw. Short-Signale generiert. Gleichzeitig werden feste Take-Profit- und Stop-Loss-Niveaus festgelegt und das Konzept des Risiko-Ertrags-Verhältnisses (R:R) eingeführt. Darüber hinaus werden ein maximaler täglicher Verlust und maximaler täglicher Gewinn sowie ein strengerer nachlaufender Stop-Loss eingesetzt, um das Risiko besser zu kontrollieren.

Strategieprinzip

- Berechnung der MACD-Linie und der Signallinie des MACD-Indikators.

- Erkennung von Kreuzen zwischen MACD-Linie und Signallinie sowie Berücksichtigung, ob der Wert der MACD-Linie einen bestimmten Schwellenwert (1,5 und -1,5) überschreitet.

- Bei einem Long-Signal wird eine Long-Position eröffnet mit Take-Profit zum aktuellen Höchstpreis + 600 kleinste Preisänderungseinheiten und Stop-Loss zum aktuellen Tiefstpreis - 100 kleinste Preisänderungseinheiten.

- Bei einem Short-Signal wird eine Short-Position eröffnet mit Take-Profit zum aktuellen Tiefstpreis - 600 kleinste Preisänderungseinheiten und Stop-Loss zum aktuellen Höchstpreis + 100 kleinste Preisänderungseinheiten.

- Ein nachlaufender Stop-Loss wird eingeführt: Wenn der Preis gegenüber dem Eröffnungspreis um mehr als 300 kleinste Preisänderungseinheiten gestiegen (Long) bzw. gefallen (Short) ist, wird der Stop-Loss auf den Eröffnungspreis + (Schlusspreis - Eröffnungspreis - 300) (Long) bzw. Eröffnungspreis - (Eröffnungspreis - Schlusspreis - 300) (Short) verschoben.

- Es werden ein maximaler täglicher Verlust und ein maximaler täglicher Gewinn gesetzt: Wenn der Tagesverlust 600 kleinste Preisänderungseinheiten oder der Tagesgewinn 1800 kleinste Preisänderungseinheiten erreicht, werden alle Positionen geschlossen.

Vorteile

- Kombination des MACD-Indikators mit Preisschwellenwerten filtert effektiv einen Teil der Rauschsignale aus.

- Festes Risiko-Ertrags-Verhältnis (R:R) macht das Risiko und den Ertrag jedes Trades kontrollierbar.

- Der nachlaufende Stop-Loss kann nach der Bildung eines Trends Gewinne schützen und Drawdowns reduzieren.

- Die täglichen Verlust- und Gewinngrenzen helfen, das tägliche Risiko zu begrenzen und übermäßige Verluste oder Gewinnrückgänge zu vermeiden.

Risikoanalyse

- Der MACD-Indikator hat eine Verzögerung, was zu Signalverzögerungen oder Fehlsignalen führen kann.

- Feste Take-Profit- und Stop-Loss-Niveaus können sich an unterschiedliche Marktbedingungen nicht anpassen, was bei Seitwärtsbewegungen zu häufigem Auslösen von Stop-Loss führen kann.

- Der nachlaufende Stop-Loss kann bei Trendumkehrungen nicht rechtzeitig stoppen, was zu Gewinnrückgängen führt.

- Die täglichen Verlust- und Gewinngrenzen können dazu führen, dass die Strategie bei klaren Trendtagen vorzeitig schließt und potenzielle Gewinne verpasst.

Optimierungsmöglichkeiten

- Verwendung von MACD-Indikatoren auf mehreren Zeitrahmen zur Bestätigung von Signalen, um die Signalgenauigkeit zu erhöhen.

- Dynamische Anpassung von Take-Profit- und Stop-Loss-Niveaus basierend auf der Marktvolatilität, um sich an unterschiedliche Marktbedingungen anzupassen.

- Optimierung des nachlaufenden Stop-Loss, z. B. durch Verwendung des ATR-Indikators zur Einstellung des Abstands des nachlaufenden Stop-Loss, um besser an Preisbewegungen angepasst zu sein.

- Parameteroptimierung der täglichen Verlust- und Gewinngrenzen, um geeignete Grenzwerte zu finden, die Risiko kontrollieren und gleich versuchen, Trendbewegungen zu erfassen.

Zusammenfassung

Diese Strategie nutzt die Konvergenz und Divergenz des MACD-Indikators zur Identifizierung von Handelssignalen und führt gleichzeitig Risikokontrollmaßnahmen wie Risiko-Ertrags-Verhältnis, nachlaufenden Stop-Loss und tägliche Grenzen ein. Obwohl die Strategie bis zu einem gewissen Grad Trendbewegungen erfassen und Risiken kontrollieren kann, gibt es noch Raum für Optimierung und Verbesserung. Zukünftige Optimierungen könnten aus den Dimensionen Signalbestätigung, Take-Profit/Stop-Loss, nachlaufender Stop-Loss und tägliche Grenzen erfolgen, um stabilere und attraktivere Renditen zu erzielen.

- 1