ZLSMA-Erweiterte Chandelier Exit-Strategie mit Volumenimpulserkennung

Überblick

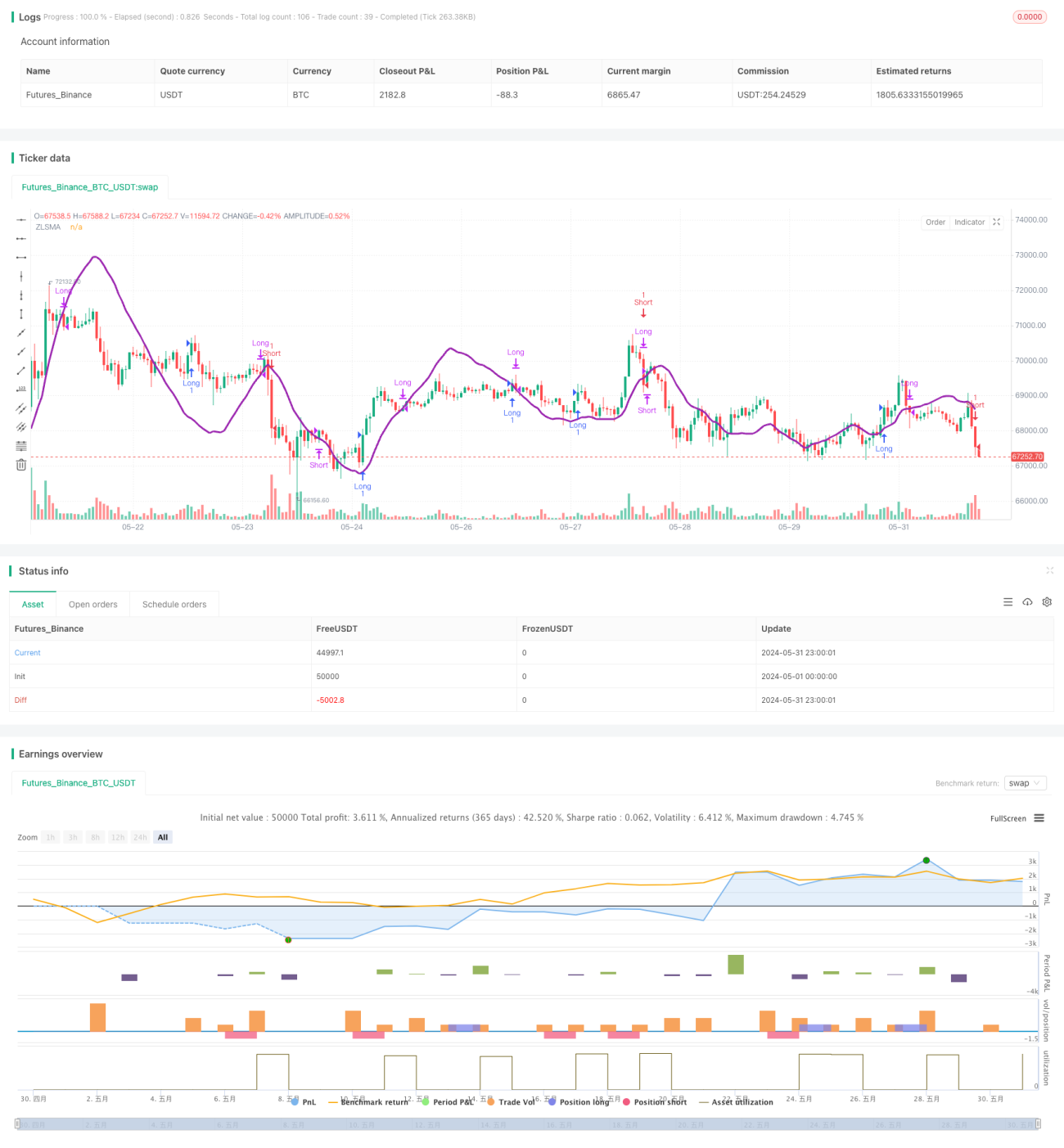

Diese Strategie kombiniert die Chandelier-Exit-Methode, den Zero-Lag Moving Average (ZLSMA) und die relative Volumenimpulserkennung (RVOL) zu einem vollständigen Handelssystem. Die Chandelier-Exit-Methode passt den Stop-Loss dynamisch an die durchschnittliche true Range (ATR) an, um sich besser an Marktveränderungen anzupassen. Der ZLSMA erfasst Preistrends präzise und liefert eine Richtungsvorgabe für den Handel. Die RVOL-Impulserkennung hilft der Strategie, seitwärts gerichtete Märkte mit niedriger Volatilität zu vermeiden und die Handelsqualität zu verbessern.

Strategieprinzip

- Berechnung des ATR und Bestimmung der Long- und Short-Stop-Loss-Positionen basierend auf ATR und Höchst-/Tiefstkurs.

- Berechnung des ZLSMA als Grundlage für die Trendrichtung.

- Berechnung des RVOL; Vergleich des RVOL mit einem festgelegten Schwellenwert, um zu bestimmen, ob ein Volumenimpuls vorliegt.

- Long-Einstieg: Der aktuelle Schlusskurs kreuzt über den ZLSMA, und der RVOL ist größer als der Schwellenwert. Es wird eine Long-Position eröffnet, der Stop-Loss liegt beim jüngsten Tiefstkurs.

- Short-Einstieg: Der aktuelle Schlusskurs kreuzt unter den ZLSMA, und der RVOL ist größer als der Schwellenwert. Es wird eine Short-Position eröffnet, der Stop-Loss liegt beim jüngsten Höchstkurs.

- Long-Ausstieg: Der aktuelle Schlusskurs kreuzt unter den ZLSMA. Die Long-Position wird geschlossen.

- Short-Ausstieg: Der aktuelle Schlusskurs kreuzt über den ZLSMA. Die Short-Position wird geschlossen.

Strategievorteile

- Die Chandelier-Exit-Methode passt den Stop-Loss dynamisch an, was das Risiko eines festen Stop-Loss reduziert.

- Der ZLSMA reagiert schnell auf Preisänderungen und liefert eine zuverlässige Trendeinschätzung für den Handel.

- Die RVOL-Impulserkennung hilft der Strategie, Märkte mit niedriger Volatilität und Seitwärtsbewegungen zu vermeiden, was die Handelsqualität verbessert.

- Die Strategielogik ist klar und leicht zu verstehen und umzusetzen.

Strategierisiken

- In Märkten ohne klaren Trend oder mit häufigen Schwankungen kann die Strategie eine erhöhte Anzahl von Trades auslösen, was die Transaktionskosten erhöht.

- Die Parametereinstellungen der Strategie (z. B. ATR-Periode, ZLSMA-Periode, RVOL-Schwellenwert) haben einen großen Einfluss auf die Performance; ungeeignete Parameter können zu schlechten Ergebnissen führen.

- Die Strategie berücksichtigt kein Positionsmanagement und Risikokontrolle; in der Praxis müssen Grundsätze des Geldmanagements angewendet werden.

Optimierungsmöglichkeiten

- Einführung von Trendbestätigungsindikatoren wie gleitenden Durchschnitten oder Momentum-Indikatoren, um die Trendgenauigkeit weiter zu verbessern.

- Optimierung der RVOL-Impulserkennungslogik, z. B. erst bei mehreren aufeinanderfolgenden RVOL-Impulsen zu handeln, um die Signalqualität zu steigern.

- Hinzufügen einer Gewinnmitnahmelogik zu den Ausstiegsbedingungen: Bei Erreichen eines bestimmten Gewinnziels Position schließen, um erzielte Gewinne zu sichern.

- Optimierung der Strategieparameter basierend auf Marktmerkmalen und dem gehandelten Instrument, um die beste Parameterkombination zu finden.

- Integration von Positionsmanagement und Risikokontrollprinzipien, um die Robustheit und Zuverlässigkeit der Strategie zu verbessern.

Zusammenfassung

Die ZLSMA-verstärkte Chandelier-Exit-Strategie mit Volumenimpulserkennung ist eine trendfolgende Strategie, die durch dynamische Stop-Loss-Anpassung, Trendbestimmung und Volumenimpulserkennung Trendchancen nutzt und gleichzeitig Handelsrisiken kontrolliert. Die Strategielogik ist klar, leicht zu verstehen und umzusetzen. In der Praxis muss sie jedoch an die spezifischen Marktmerkmale und gehandelten Instrumente angepasst und optimiert werden. Durch die Einführung zusätzlicher Signale zur Bestätigung, Optimierung der Ausstiegsbedingungen, angemessene Parametereinstellungen sowie strenges Positionsmanagement und Risikokontrolle kann diese Strategie zu einem robusten und effizienten Handelswerkzeug werden.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Chandelier Exit Strategy with ZLSMA and Volume Spike Detection", shorttitle="CES with ZLSMA and Volume", overlay=true, process_orders_on_close=true, calc_on_every_tick=false)

// Chandelier Exit Inputs

lengthAtr = input.int(title='ATR Period', defval=1)- 1