Dynamische adaptive Momentum-Breakout-Strategie

Übersicht

Die Dynamische Adaptive Momentum-Breakout-Strategie ist eine fortschrittliche quantitative Handelsstrategie, die einen adaptiven Momentum-Indikator und die Erkennung von Kerzenformationen nutzt. Die Strategie passt den Momentum-Zyklus dynamisch an die Marktvolatilität an und kombiniert mehrere Filterbedingungen, um Trendausbrüche mit hoher Wahrscheinlichkeit zu identifizieren. Der Kern der Strategie liegt in der Erfassung von Momentum-Veränderungen, während das Engulfing-Muster als Einstiegssignal dient, um die Genauigkeit und Rentabilität von Trades zu erhöhen.

Strategieprinzip

-

Dynamische Zyklusanpassung:

- Die Strategie verwendet einen adaptiven Momentum-Indikator, der den Berechnungszyklus dynamisch an die Marktvolatilität anpasst.

- In Phasen hoher Volatilität wird der Zyklus verkürzt, um schnell auf Marktänderungen zu reagieren; in Phasen geringer Volatilität wird der Zyklus verlängert, um Überhandel zu vermeiden.

- Der Zyklusbereich liegt zwischen 10 und 40, wobei der ATR-Indikator zur Beurteilung der Volatilität herangezogen wird.

-

Momentumberechnung und Glättung:

- Der Momentum-Indikator wird mit dem dynamischen Zyklus berechnet.

- Es kann wahlweise eine EMA-Glättung des Momentums durchgeführt werden (Standard: 7-Perioden-EMA).

-

Trendrichtungserkennung:

- Die Trendrichtung wird durch die Berechnung der Momentum-Steigung (Differenz zwischen aktuellem und vorherigem Wert) bestimmt.

- Eine positive Steigung signalisiert einen Aufwärtstrend, eine negative Steigung einen Abwärtstrend.

-

Erkennung von Engulfing-Mustern:

- Benutzerdefinierte Funktionen erkennen bullische und bärische Engulfing-Muster.

- Es werden die Beziehungen zwischen Eröffnungs- und Schlusskurs der aktuellen und der vorherigen Kerze berücksichtigt.

- Ein minimaler Kerzenkörper-Filter wird eingeführt, um die Zuverlässigkeit der Muster zu erhöhen.

-

Generierung von Handelssignalen:

- Long-Signal: Bullisches Engulfing-Muster + positive Momentum-Steigung.

- Short-Signal: Bärisches Engulfing-Muster + negative Momentum-Steigung.

-

Handelsmanagement:

- Einstieg bei Eröffnung der nächsten Kerze nach Signalbestätigung.

- Automatischer Ausstieg nach einem festen Haltezyklus (Standard: 3 Kerzen).

Strategievorteile

-

Hohe Anpassungsfähigkeit:

- Dynamische Anpassung des Momentum-Zyklus an unterschiedliche Marktumgebungen.

- Schnelle Reaktion in Phasen hoher Volatilität, Vermeidung von Überhandel in ruhigen Phasen.

-

Mehrfache Bestätigungsmechanismen:

- Kombination von technischen Indikatoren (Momentum) und Preisformationen (Engulfing) erhöht die Signalgüte.

- Nutzung von Steigungs- und Kerzenkörpergrößen-Filtern reduziert Fehlsignale.

-

Präziser Einstiegszeitpunkt:

- Nutzung von Engulfing-Mustern zur Erfassung potenzieller Trendwenden.

- Kombination mit der Momentum-Steigung stellt sicher, dass in einen aufkommenden Trend eingestiegen wird.

-

Angemessenes Risikomanagement:

- Fester Haltezyklus verhindert übermäßiges Halten und reduziert Drawdowns.

- Kerzenkörper-Filter verringert Fehlinterpretationen durch kleine Kursschwankungen.

-

Flexibel und anpassbar:

- Mehrere einstellbare Parameter ermöglichen eine Optimierung für verschiedene Märkte und Zeitrahmen.

- Optionale EMA-Glättung balanciert Sensitivität und Stabilität.

Strategierisiken

-

Risiko von Fehlausbrüchen:

- In Seitwärtsmärkten können gehäuft Fehlsignale auftreten.

- Abhilfe: Hinzufügen zusätzlicher Trendbestätigungsindikatoren wie gleitende Durchschnittskreuze.

-

Verzögerungsproblem:

- Die EMA-Glättung kann zu Signalen mit Verzögerung führen, wodurch der optimale Einstiegspunkt verpasst wird.

- Abhilfe: Anpassung des EMA-Zyklus oder Verwendung sensiblerer Glättungsmethoden.

-

Begrenzte Ausstiegsmechanik:

- Der feste Ausstiegszyklus kann einen profitablen Trend vorzeitig beenden oder Verluste verlängern.

- Abhilfe: Einführung dynamischer Stop-Loss/Take-Profit, z. B. Trailing-Stop oder volatilitätsbasierter Ausstieg.

-

Übermäßige Abhängigkeit von einem einzigen Zeitrahmen:

- Die Strategie ignoriert möglicherweise den übergeordneten Trend höherer Zeitrahmen.

- Abhilfe: Integration einer Multi-Timeframe-Analyse, um die Handelsrichtung mit dem übergeordneten Trend abzustimmen.

-

Parameterempfindlichkeit:

- Zu viele einstellbare Parameter können zu Overfitting historischer Daten führen.

- Abhilfe: Verwendung schrittweiser Optimierung und Out-of-Sample-Tests zur Validierung der Parameterstabilität.

Optimierungsrichtungen der Strategie

-

Integration mehrerer Zeitrahmen:

- Einführung einer Trendbeurteilung auf höheren Zeitrahmen; nur in Richtung des übergeordneten Trends handeln.

- Grund: Erhöhung der gesamten Erfolgsrate, Vermeidung von Trades gegen den großen Trend.

-

Dynamischer Stop-Loss/Take-Profit:

- Implementierung dynamischer Stop-Loss basierend auf ATR oder Momentum-Änderungen.

- Verwendung eines Trailing-Stops zur Maximierung von Trendgewinnen.

- Grund: Anpassung an die Marktvolatilität, Gewinnsicherung, Reduzierung von Drawdowns.

-

Volume-Profile-Analyse:

- Integration von Volume Profile zur Identifizierung wichtiger Support- und Widerstandszonen.

- Grund: Verbesserung der Einstiegsgenauigkeit, Vermeidung von Trades an ineffektiven Ausbruchspunkten.

-

Optimierung durch maschinelles Lernen:

- Verwendung von ML-Algorithmen zur dynamischen Parameteranpassung.

- Grund: Kontinuierliche Anpassungsfähigkeit der Strategie, langfristige Stabilität.

-

Integration von Sentiment-Indikatoren:

- Einführung von Marktstimmungsindikatoren wie VIX oder impliziter Volatilität aus Optionen.

- Grund: Anpassung des Strategieverhaltens bei extremer Stimmung, Vermeidung von Überhandel.

-

Korrelationsanalyse:

- Berücksichtigung der gleichzeitigen Bewegung mehrerer verwandter Assets.

- Grund: Erhöhung der Signalgüte, Identifizierung stärkerer Markttrends.

Zusammenfassung

Die Dynamische Adaptive Momentum-Breakout-Strategie ist ein fortschrittliches Handelssystem, das technische Analyse mit quantitativen Methoden verbindet. Durch die dynamische Anpassung des Momentum-Zyklus, die Identifikation von Engulfing-Mustern und die Kombination mehrerer Filterbedingungen kann die Strategie in verschiedenen Marktumgebungen Trendausbrüche mit hoher Wahrscheinlichkeit erfassen. Obwohl inhärente Risiken wie Fehlausbrüche und Parameterempfindlichkeit bestehen, besteht durch die vorgeschlagenen Optimierungsrichtungen – wie Multi-Timeframe-Analyse, dynamisches Risikomanagement und maschinelles Lernen – Potenzial, die Stabilität und Rentabilität weiter zu steigern. Insgesamt handelt es sich um eine klar strukturierte, logisch stringente quantitative Strategie, die Händlern ein leistungsstarkes Werkzeug zur Nutzung von Marktmomentum und Trendveränderungen bietet.

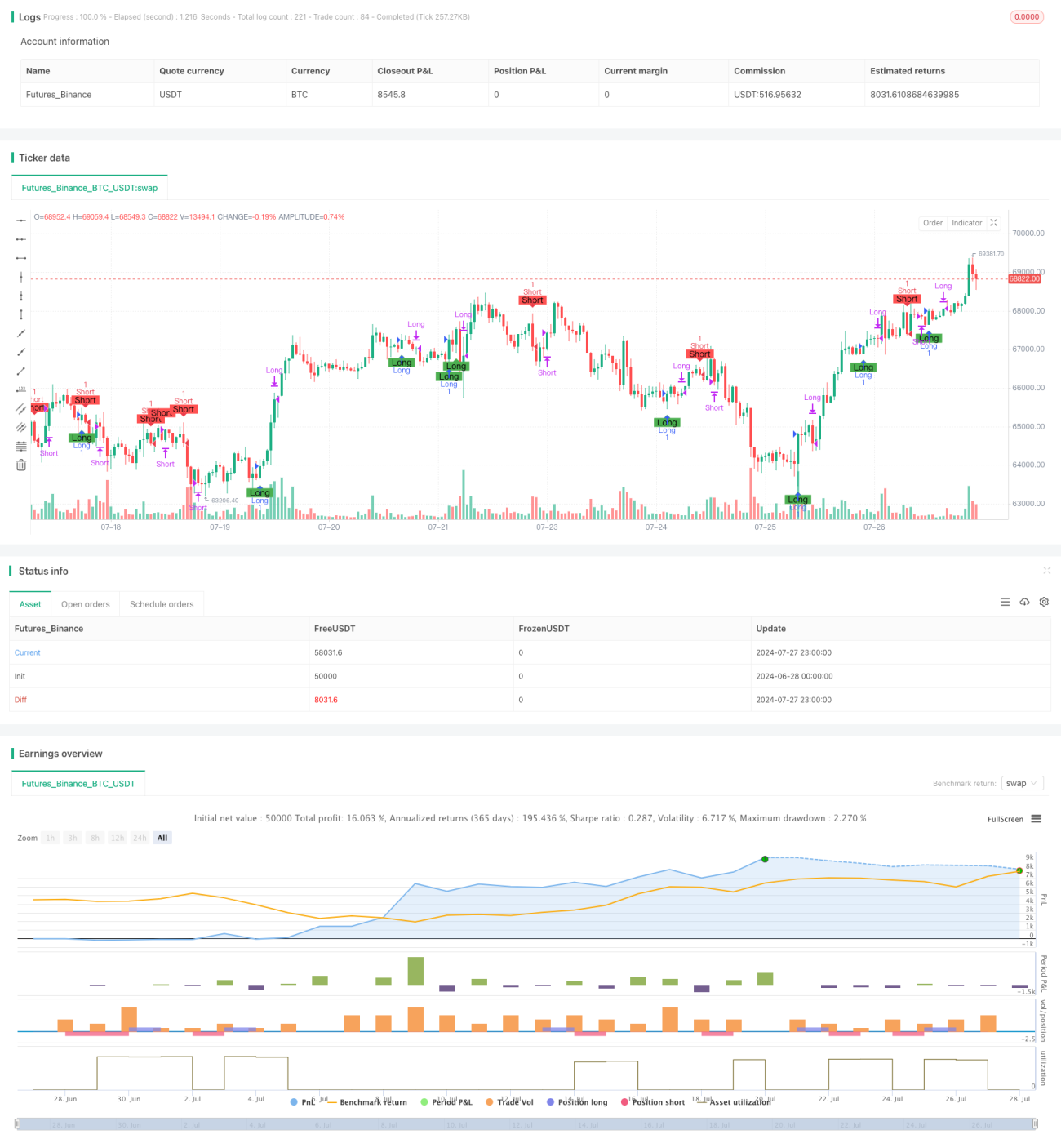

/*backtest

start: 2024-06-28 00:00:00

end: 2024-07-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ironperol

//@version=5

strategy("Adaptive Momentum Strategy", overlay=true, margin_long=100, margin_short=100)- 1