Übersicht

Diese Strategie ist ein umfassendes Handelssystem, das auf mehreren technischen Indikatoren basiert. Es nutzt hauptsächlich exponentiell gleitende Durchschnitte (EMA), den Relative-Stärke-Index (RSI) und das Handelsvolumen, um Handelssignale zu generieren und Positionen zu verwalten. Die Strategie verwendet EMA-Kreuze, um den Markttrend zu bestimmen, gleichzeitig den RSI-Indikator, um überkaufte/überverkaufte Bedingungen zu erkennen, und kombiniert dies mit dem Volumen, um die Signalstärke zu bestätigen. Darüber hinaus enthält die Strategie einen dynamischen Take-Profit- und Stop-Loss-Mechanismus sowie eine feste Haltedauer, um Risiken zu kontrollieren und die Handelsleistung zu optimieren.

Strategieprinzip

-

Generierung von Handelssignalen:

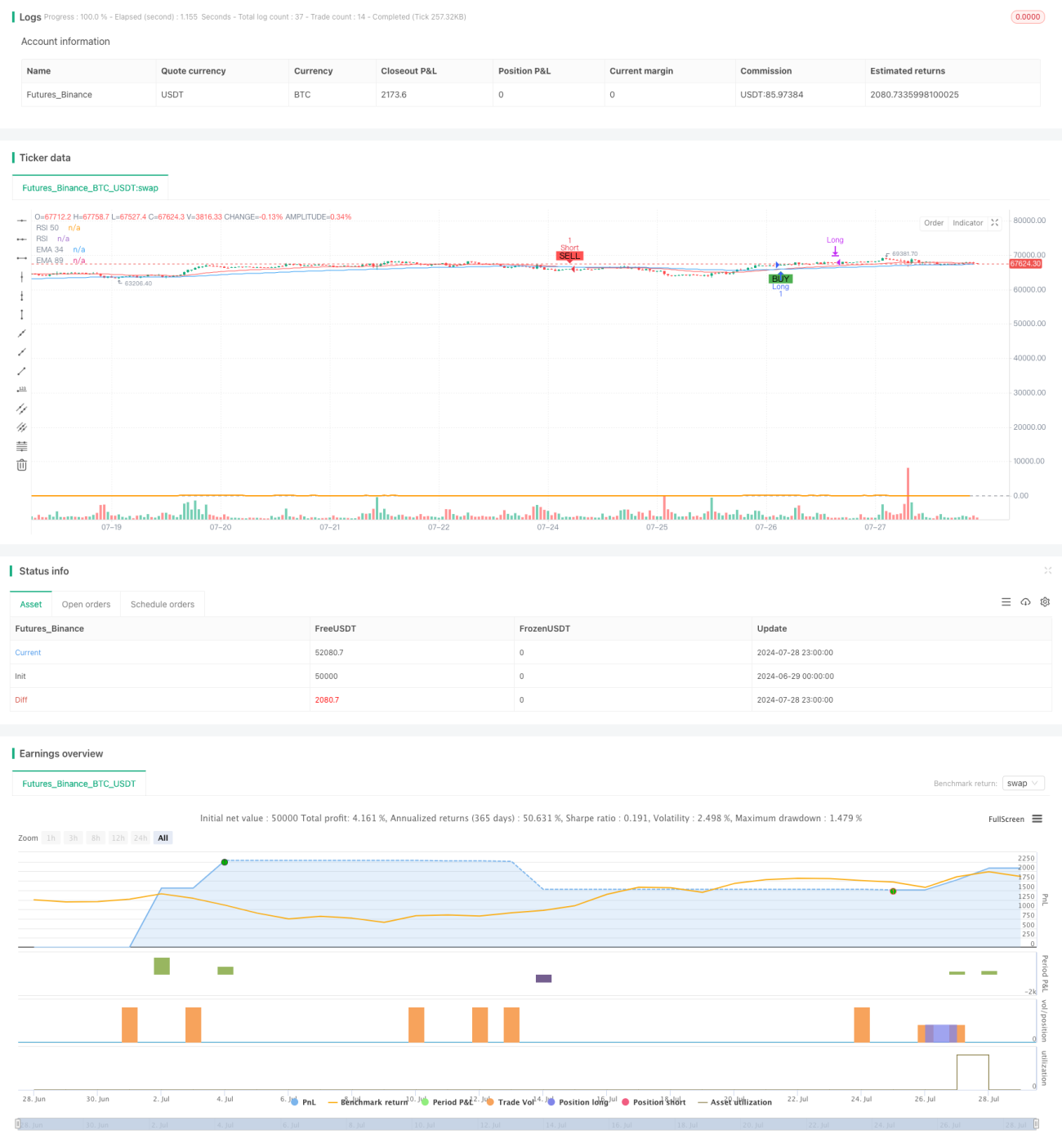

- Long-Einstieg: EMA34 kreuzt über EMA89 und RSI größer als 30.

- Short-Einstieg: EMA34 kreuzt unter EMA89 und RSI kleiner als 70.

-

Dynamischer Take-Profit und Stop-Loss:

- Wenn das Handelsvolumen größer als das Dreifache des durchschnittlichen Volumens der letzten 20 Kerzen ist, werden die Take-Profit- und Stop-Loss-Kurse aktualisiert.

- Die Take-Profit- und Stop-Loss-Kurse werden auf den Schlusskurs zum Zeitpunkt des hohen Volumens gesetzt.

-

Feste Haltedauer:

- Unabhängig von Gewinn oder Verlust wird die Position nach 15 Kerzen zwangsweise geschlossen.

-

EMA-Stop-Loss:

- Verwendung von EMA34 als dynamische Stop-Loss-Linie.

-

Volumenbestätigung:

- Die Bedingung hohen Handelsvolumens wird verwendet, um die Signalstärke zu bestätigen und die Take-Profit- und Stop-Loss-Kurse zu aktualisieren.

Strategievorteile

-

Koordination mehrerer Indikatoren: Kombination von EMA, RSI und Volumen für eine umfassende Marktanalyse und erhöhte Zuverlässigkeit der Signale.

-

Dynamisches Risikomanagement: Echtzeit-Anpassung von Take-Profit und Stop-Loss basierend auf der Marktvolatilität, Anpassung an unterschiedliche Marktumgebungen.

-

Feste Haltedauer: Vermeidung von Risiken durch langfristige Positionen, Begrenzung der Expositionszeit pro Trade.

-

Dynamischer EMA-Stop-Loss: Nutzung des gleitenden Durchschnitts als dynamische Unterstützung/Widerstand für flexibleren Stop-Loss-Schutz.

-

Volumenbestätigung: Nutzung von Volumenausbrüchen zur Bestätigung der Signalstärke, Erhöhung der Handelsgenauigkeit.

-

Visuelle Unterstützung: Markierung von Kauf-/Verkaufssignalen und wichtigen Preisniveaus im Chart zur Erleichterung von Analyse und Entscheidungsfindung.

Strategierisiken

-

Risiko in Seitwärtsmärkten: In einer bandbreitenorientierten Marktphase können EMA-Kreuze häufige Fehlsignale erzeugen.

-

Feste RSI-Schwellenwerte: Feste RSI-Schwellenwerte sind möglicherweise nicht für alle Marktumgebungen geeignet.

-

Volumenschwellen-Empfindlichkeit: Der Schwellenwert des Dreifachen des Durchschnittsvolumens kann zu hoch oder zu niedrig sein und muss je nach spezifischem Markt angepasst werden.

-

Feste Haltedauerbeschränkung: Die feste Schließzeit nach 15 Kerzen kann profitable Trades vorzeitig beenden.

-

Festlegung von Take-Profit/Stop-Loss-Kursen: Die Verwendung des Schlusskurses zum Zeitpunkt des hohen Volumens als Take-Profit/Stop-Loss ist möglicherweise nicht optimal.

Optimierungsmöglichkeiten

-

Dynamische RSI-Schwellenwerte: Automatische Anpassung der überkauften/überverkauften RSI-Schwellenwerte basierend auf der Marktvolatilität.

-

Optimierung des Volumenschwellenwerts: Einführung eines adaptiven Mechanismus zur dynamischen Anpassung des Volumenausbruch-Multiplikators basierend auf historischen Daten.

-

Verbessertes Haltedauermanagement: Dynamische Anpassung der maximalen Haltedauer unter Berücksichtigung von Trendstärke und Gewinnsituation.

-

Optimierung der Take-Profit/Stop-Loss-Einstellungen: Erwägung der Einführung des ATR-Indikators zur dynamischen Festlegung von Take-Profit/Stop-Loss basierend auf der Marktvolatilität.

-

Hinzufügen eines Trendfilters: Einführung eines langfristigen EMA oder Trendindikators, um Trades gegen den Haupttrend zu vermeiden.

-

Integration von Price Action-Analyse: Kombination von Candlestick-Mustern und Unterstützungs-/Widerstandsniveaus zur Verbesserung der Ein- und Ausstiegsgenauigkeit.

-

Berücksichtigung eines Drawdown-Controls: Festlegung eines maximalen Drawdown-Limits, das eine Zwangsschließung bei Erreichen eines bestimmten Drawdown-Levels auslöst.

Zusammenfassung

Diese mehrindikatorbasierte, dynamische Handelsstrategie schafft durch die Kombination von EMA, RSI und Volumen ein umfassendes Handelssystem. Sie kann nicht nur Markttrends erfassen, sondern auch Risiken durch dynamischen Take-Profit/Stop-Loss und eine feste Haltedauer managen. Der Vorteil der Strategie liegt in ihrer multidimensionalen Analyse und dem flexiblen Risikomanagement, gleichzeitig steht sie jedoch vor Herausforderungen durch sich ändernde Marktbedingungen. Durch weitere Optimierung der RSI-Schwellenwerte, der Volumenkriterien, des Haltedauermanagements sowie der Take-Profit/Stop-Loss-Einstellungen hat die Strategie das Potenzial, in verschiedenen Marktumgebungen eine verbesserte Performance zu erzielen. Letztlich bietet diese Strategie Händlern einen zuverlässigen Rahmen, der je nach individuellem Handelsstil und Marktbesonderheiten angepasst und verbessert werden kann.

- 1