Überblick

Diese Strategie ist ein marktoffenes Handelssystem, das auf mehreren technischen Indikatoren basiert und sich hauptsächlich auf die Eröffnungsphasen des deutschen und US-amerikanischen Marktes konzentriert. Die Strategie identifiziert Konsolidierungsphasen mithilfe von Bollinger-Bändern, bestätigt die Trendrichtung mit kurzfristigen und langfristigen exponentiellen gleitenden Durchschnitten, filtert Handelssignale mit dem Relative-Stärke-Index und dem Trendstärkeindikator und verwendet schließlich den Average True Range (ATR) zur dynamischen Positionsverwaltung.

Strategieprinzip

Die Strategie verwendet ein 14-Perioden-Bollinger-Band (1,5-fache Standardabweichung), um Phasen geringer Volatilität zu identifizieren. Wenn sich der Preis der Mittellinie des Bollinger-Bands nähert, wird dies als Konsolidierung betrachtet. Gleichzeitig werden ein 10-Perioden- und ein 200-Perioden-exponentieller gleitender Durchschnitt verwendet, um einen Aufwärtstrend zu bestätigen. Dabei muss der Preis über beiden gleitenden Durchschnitten liegen. Ein 7-Perioden-RSI stellt sicher, dass der Markt nicht überverkauft ist (>30), und ein 7-Perioden-ADX bestätigt die Trendstärke (>10). Die Strategie analysiert auch die Höchstkurse der letzten 20 Kerzen, um Widerstandsniveaus zu finden, die mindestens zweimal berührt wurden. Wenn der Preis dieses Widerstandsniveau durchbricht und die anderen Bedingungen erfüllt sind, erfolgt der Einstieg. Ein Stop-Loss wird mit dem 2-fachen ATR und ein Take-Profit mit dem 4-fachen ATR gesetzt.

Strategievorteile

- Mehrere technische Indikatoren kreuzvalidieren sich, wodurch Fehlsignale effektiv reduziert werden.

- Dynamischer Stop-Loss und Take-Profit basierend auf ATR passen sich der Marktvolatilität an.

- Konzentration auf Chancen mit hoher Volatilität während der Markteröffnung.

- Erfassung starker Trends durch das Konsolidierungs-Durchbruchsmuster.

- Vollständiger Risikomanagementmechanismus.

Strategierisiken

- Mehrere Indikatoren können dazu führen, dass einige Handelsmöglichkeiten verpasst werden.

- Starke Kursschwankungen während der Eröffnungsphase können den Stop-Loss auslösen.

- Schnelle Marktumkehrungen können zu erheblichen Verlusten führen.

Es wird empfohlen, eine angemessene Positionsgröße zu verwenden, die Stop-Loss-Strategie strikt einzuhalten und übermäßigen Handel zu vermeiden.

Optimierungsmöglichkeiten

- Anpassung der Indikatorparameter je nach Markteigenschaften.

- Hinzufügen von Volumenindikatoren zur Validierung der Durchbruchseffektivität.

- Einführung weiterer technischer Indikatoren zur Erhöhung der Signalezuverlässigkeit.

- Optimierung des Einstiegszeitpunkts zur Verringerung von Slippage-Einflüssen.

- Verbesserung des Take-Profit- und Stop-Loss-Mechanismus zur Steigerung des Gewinn-Verlust-Verhältnisses.

Zusammenfassung

Diese Strategie erfasst Handelsmöglichkeiten während der Markteröffnung durch eine mehrdimensionale technische Analyse und verwaltet das Risiko mit dynamischen Stop-Loss- und Take-Profit-Einstellungen. Die Strategie ist logisch aufgebaut, verfügt über ein robustes Risikomanagement und ist gut praktisch anwendbar. Durch kontinuierliche Optimierung und Anpassung kann die Strategieleistung voraussichtlich weiter verbessert werden.

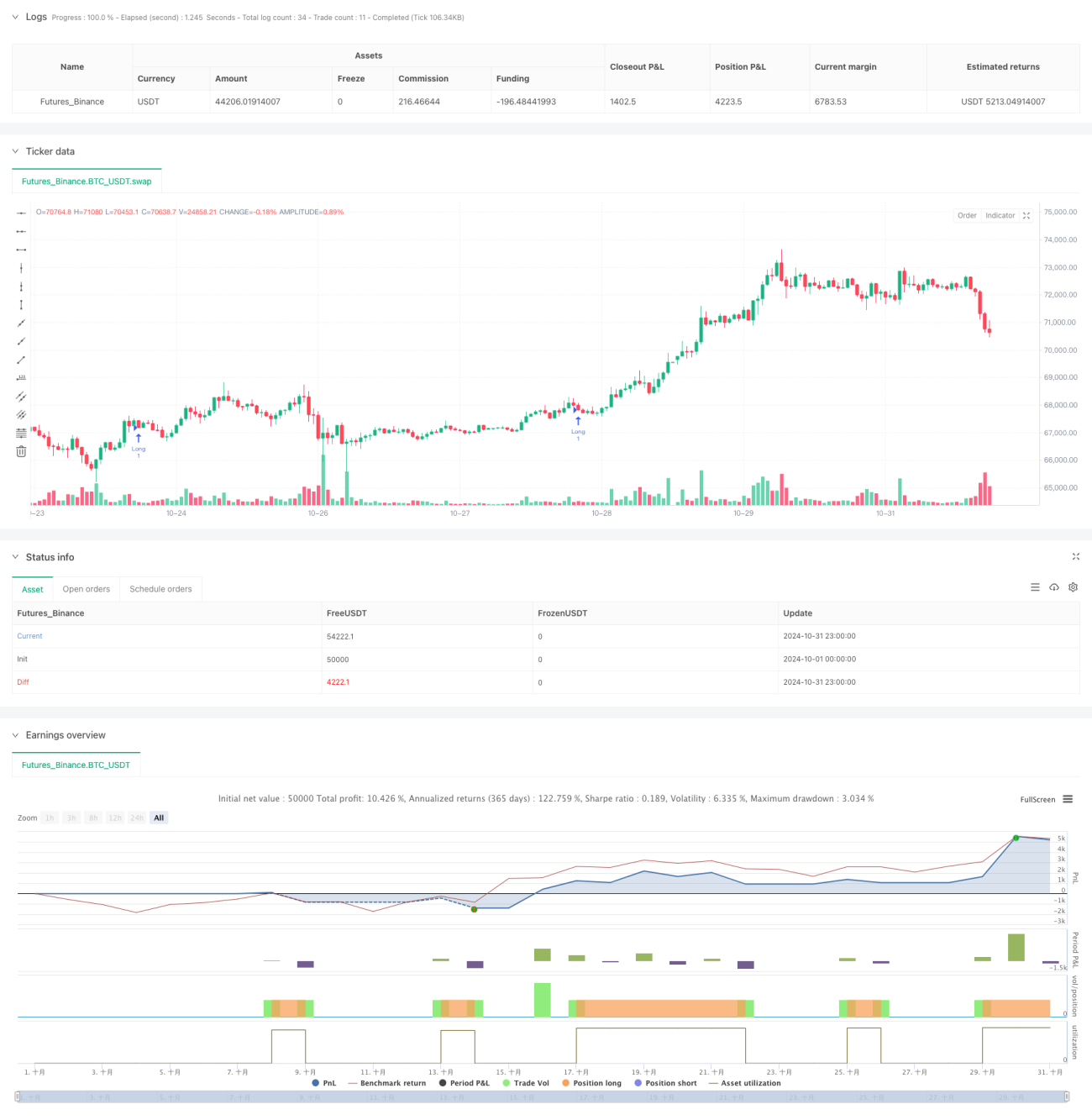

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Post-Open Long Strategy with ATR-based Stop Loss and Take Profit (Separate Alerts)", overlay=true)

// Parametri per Bande di Bollinger ed EMA- 1