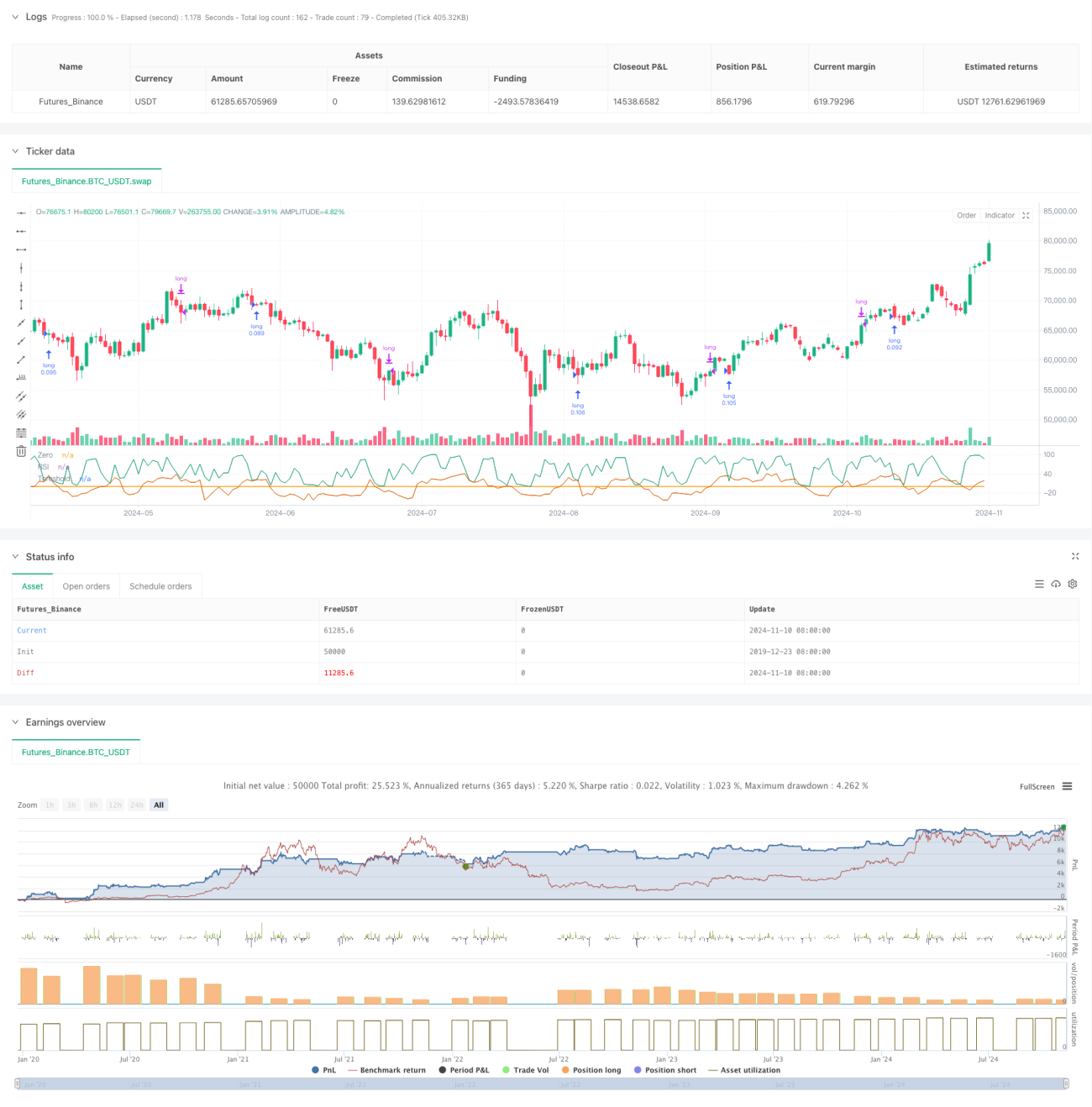

Überblick

Diese Strategie ist ein adaptives Handelssystem, das auf dem RSI (Relative Strength Index) basiert und die Handelssignale durch dynamische Anpassung der überkauften/überverkauften Schwellenwerte optimiert. Die Kerninnovation der Strategie liegt in der Einführung der Bufi Adaptive Threshold (BAT)-Methode, die die RSI-Trigger-Schwellenwerte dynamisch an Markttrends und Preisvolatilität anpasst und so die Effektivität der traditionellen RSI-Strategie verbessert.

Strategieprinzip

Der Kern der Strategie besteht darin, das traditionelle System mit festen RSI-Schwellenwerten auf ein System mit dynamischen Schwellenwerten zu aktualisieren. Die konkrete Umsetzung erfolgt wie folgt:

- Verwendung eines kurzfristigen RSI zur Berechnung des überkauften/überverkauften Marktzustands

- Berechnung der Preistrendsteigung durch lineare Regression

- Messung der Preisvolatilität mithilfe der Standardabweichung

- Integration von Trend- und Volatilitätsinformationen zur dynamischen Anpassung der RSI-Schwellenwerte

- Erhöhung der Schwellenwerte in Aufwärtstrends, Senkung in Abwärtstrends

- Verringerung der Schwellenempfindlichkeit, wenn der Preis stark vom Mittelwert abweicht

Die Strategie enthält auch zwei Risikokontrollmechanismen:

- Festzyklus-Schließungsmechanismus

- Maximalverlust-Stoppmechanismus

Strategievorteile

-

Hohe dynamische Anpassungsfähigkeit:

- Automatische Anpassung der Handelsschwellen an den Marktzustand

- Vermeidung der Nachteile fester Parameter in verschiedenen Marktumgebungen

-

Umfassende Risikokontrolle:

- Begrenzung der maximalen Haltedauer

- Kapital-Stopp-Verlust-Schutzmechanismus

- Prozentuales Positionsmanagement

-

Verbesserte Signalqualität:

- Reduzierung falscher Signale in Seitwärtsmärkten

- Erhöhte Erfassungsfähigkeit in Trendmärkten

- Balance zwischen Sensitivität und Stabilität

Strategierisiken

-

Parameterempfindlichkeit:

- Wahl des BAT-Koeffizienten beeinflusst die Strategieleistung

- RSI-Zykluseinstellungen erfordern gründliche Tests

- Parameter für adaptive Längen müssen optimiert werden

-

Abhängigkeit vom Marktumfeld:

- Mögliches Verpassen von Chancen in hochvolatilen Märkten

- Große Slippage bei Stopp-Loss in starken Schwankungen

- Parameter müssen je nach Markt angepasst werden

-

Technische Einschränkungen:

- Abhängigkeit von historischen Daten zur Schwellenberechnung

- Mögliche Verzögerung (Lag)

- Berücksichtigung der Transaktionskosten erforderlich

Optimierungsrichtungen

-

Parameteroptimierung:

- Einführung eines adaptiven Parameterauswahlmechanismus

- Dynamische Anpassung der Parameter je nach Marktzyklus

- Hinzufügen einer automatischen Parameteroptimierungsfunktion

-

Signaloptimierung:

- Kombination mit anderen technischen Indikatoren zur Bestätigung

- Hinzufügen einer Marktzykluserkennungsfunktion

- Optimierung des Einstiegszeitpunkts

-

Risikokontrolloptimierung:

- Einführung eines dynamischen Stopp-Loss-Mechanismus

- Optimierung der Positionsmanagementstrategie

- Hinzufügen eines Drawdown-Kontrollmechanismus

Zusammenfassung

Dies ist eine innovative adaptive Handelsstrategie, die die Einschränkungen der traditionellen RSI-Strategie durch dynamische Schwellenwerte überwindet. Die Strategie berücksichtigt sowohl Markttrends als auch Volatilität und bietet eine hohe Anpassungsfähigkeit sowie Risikokontrollfähigkeiten. Trotz Herausforderungen wie der Parameteroptimierung kann die Strategie durch kontinuierliche Verbesserung und Optimierung im realen Handel stabile Ergebnisse erzielen. Es wird empfohlen, vor dem Live-Einsatz ausreichende Backtests und Parameteroptimierungen durchzuführen sowie Anpassungen an die spezifischen Marktgegebenheiten vorzunehmen.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PineCodersTASC

// TASC Issue: October 2024- 1