Doppelte MACD-Preisaktions-Durchbruchsverfolgungsstrategie

Übersicht

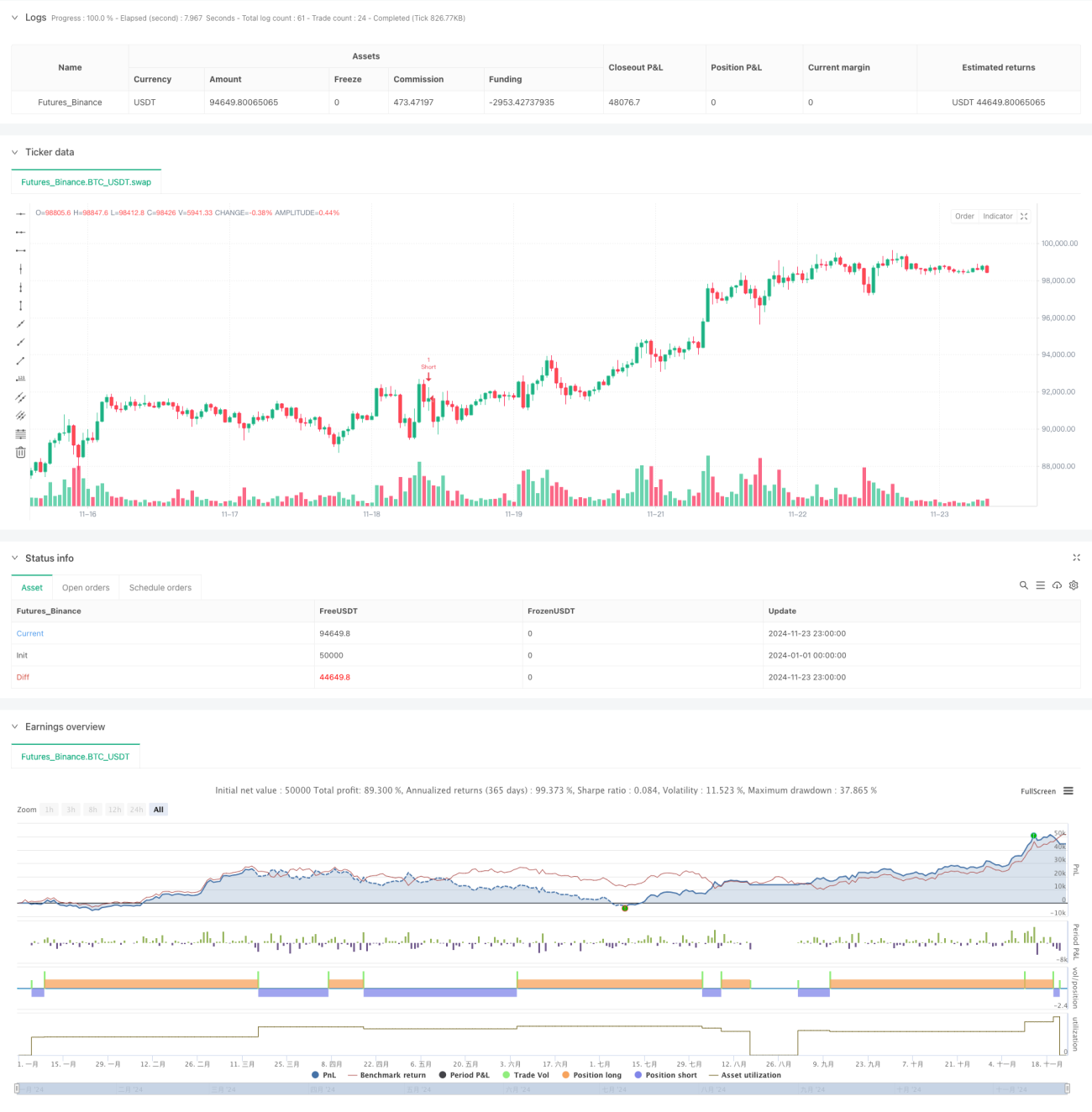

Dies ist eine Handelsstrategie, die doppelte MACD-Indikatoren mit der Analyse des Preisverhaltens kombiniert. Die Strategie bestimmt den Markttrend, indem sie die Farbveränderungen des doppelten MACD-Histogramms im 15-Minuten-Zeitraum beobachtet, sucht gleichzeitig im 5-Minuten-Zeitraum nach starken Kerzenmustern und bestätigt Ausbruchssignale im 1-Minuten-Zeitraum. Die Strategie verwendet einen dynamischen Stop-Loss basierend auf dem ATR und einen Trailing-Profit-Mechanismus, um das Risiko effektiv zu managen und gleichzeitig den Gewinnspielraum zu maximieren.

Strategieprinzip

Die Strategie verwendet zwei MACD-Indikatoren mit unterschiedlichen Parametern (34/144/9 und 100/200/50), um den Markttrend zu bestätigen. Wenn beide MACD-Histogramme den gleichen Farbtrend anzeigen, sucht das System im 5-Minuten-Chart nach starken Kerzenmustern, die dadurch gekennzeichnet sind, dass der Körper mehr als das 1,5-fache des Schattens beträgt. Sobald eine starke Kerze gefunden wurde, überwacht das System im 1-Minuten-Chart, ob ein Ausbruch erfolgt. Bei einem Ausbruch über das Hoch im Aufwärtstrend oder unter das Tief im Abwärtstrend wird eine Position eröffnet. Der Stop-Loss wird basierend auf dem ATR-Indikator festgelegt, während das 1,5-fache des ATR als dynamischer Trailing-Profit verwendet wird.

Strategievorteile

- Multi-Zeitraum-Analyse: Kombination der drei Zeiträume 15 Minuten, 5 Minuten und 1 Minute zur Erhöhung der Signalzuverlässigkeit

- Trendbestätigung: Kreuzvalidierung durch doppelte MACD-Indikatoren reduziert Fehlsignale

- Preisverhaltensanalyse: Identifizierung wichtiger Preisniveaus durch starke Kerzenmuster

- Dynamisches Risikomanagement: Adaptiver Stop-Loss und Trailing-Profit-Mechanismus basierend auf ATR

- Signalfilterung: Strenge Einstiegsbedingungen reduzieren Fehlentscheidungen

- Hoher Automatisierungsgrad: Vollautomatischer Handel reduziert menschliche Eingriffe

Strategierisiken

- Trendumkehrrisiko: In stark volatilen Märkten können falsche Ausbrüche auftreten

- Slippage-Risiko: Hochfrequenter Handel im 1-Minuten-Zeitraum kann unter Slippage leiden

- Überhandlungsrisiko: Häufige Signale können zu übermäßigem Handel führen

- Marktabhängigkeit: In Seitwärtsmärkten kann die Performance schlecht sein

Gegenmaßnahmen:

- Hinzufügen eines Trendfilters

- Festlegen einer minimalen Volatilitätsschwelle

- Begrenzung der Handelsanzahl

- Einführung eines Markterkennungsmechanismus

Optimierungsrichtungen

- MACD-Parameteroptimierung: Anpassung der MACD-Parameter je nach Marktcharakteristik

- Stop-Loss-Optimierung: Hinzufügen eines dynamischen Stop-Loss basierend auf Volatilität

- Handelszeitfilter: Einführung von Handelszeitfenster-Beschränkungen

- Positionsmanagement: Umsetzung von schrittweisem Aufbau und Ausstieg

- Marktumgebungsfilter: Hinzufügen von Trendstärke-Indikatoren

- Drawdown-Kontrolle: Einführung eines risikobasierten Kontrollmechanismus auf Basis der Eigenkapitalkurve

Zusammenfassung

Dies ist ein Strategie-System, das technische Analyse und Risikomanagement kombiniert. Durch Multi-Zeitraum-Analyse und strenge Signalfilterung wird die Handelsqualität sichergestellt, während dynamische Stop-Loss- und Trailing-Profit-Mechanismen das Risiko effektiv managen. Die Strategie ist anpassungsfähig, erfordert jedoch eine kontinuierliche Optimierung je nach Marktumgebung. Vor dem Echtzeiteinsatz wird empfohlen, gründliche Backtests und Parameteroptimierungen durchzuführen und die Strategie an die Marktcharakteristiken anzupassen.

- 1