Multitechnische-Indikatoren-Trendfolgestrategie in Kombination mit Ichimoku-Cloud-Durchbruch und Stop-Loss-System

Übersicht

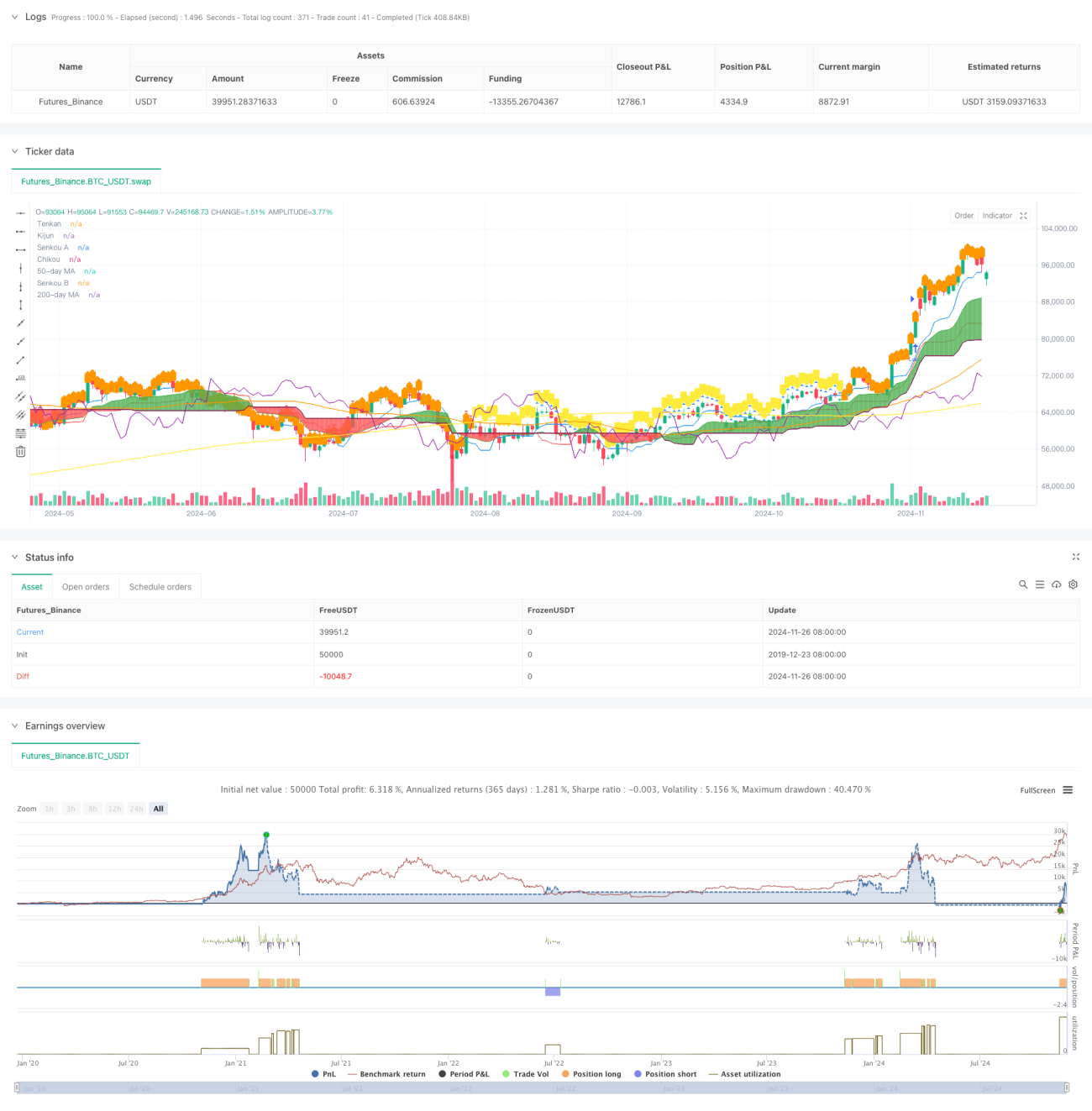

Diese Strategie ist ein vollständiges Handelssystem, das eine Reihe technischer Indikatoren kombiniert. Die Handelsentscheidungen basieren hauptsächlich auf dem Ichimoku-Wolken-Indikator. Das System nutzt die Kreuzung von Tenkan-sen und Kijun-sen als Einstiegssignal, ergänzt durch den Relative Stärke Index (RSI) und gleitende Durchschnitte (MA) als zusätzliche Filterbedingungen. Die Strategie verwendet die Wolkenkomponenten als dynamische Stop-Loss-Level und bildet so ein umfassendes Risikomanagementsystem.

Strategieprinzip

Die Kernlogik der Strategie basiert auf folgenden Schlüsselelementen:

- Das Einstiegssignal wird durch die Kreuzung von Tenkan-sen und Kijun-sen erzeugt: Ein Aufwärtskreuzen signalisiert Long, ein Abwärtskreuzen signalisiert Short.

- Die Position des Preises relativ zur Wolke (Kumo) dient als Trendbestätigung: Bei Kursen über der Wolke wird long gegangen, bei Kursen unter der Wolke short.

- Die relative Position von 50-Tage- und 200-Tage-gleitendem Durchschnitt dient als Trendfilter.

- Der wöchentliche RSI dient als Bestätigung der Marktstärke und filtert Fehlsignale.

- Die oberen und unteren Grenzen der Wolke dienen als dynamische Stop-Loss-Level und ermöglichen ein dynamisches Risikomanagement.

Strategievorteile

- Die Kombination mehrerer technischer Indikatoren liefert zuverlässigere Handelssignale und reduziert Fehlsignale deutlich.

- Die Verwendung der Wolke als dynamischer Stop-Loss passt sich automatisch an die Marktvolatilität an, schützt Gewinne und lässt ausreichend Spielraum für Kursbewegungen.

- Durch den wöchentlichen RSI-Filter werden ungünstige Trades in überkauften/überverkauften Bereichen effektiv vermieden.

- Der gleitende Durchschnittskreuzung bietet eine zusätzliche Trendbestätigung und erhöht die Erfolgsrate der Trades.

- Ein vollständiges Risikokontrollsystem, das Einstieg, Haltedauer und Ausstieg umfasst.

Strategierisiken

- Die mehrstufigen Filter könnten dazu führen, dass einige potenziell gute Gelegenheiten verpasst werden.

- In Seitwärtsmärkten können häufige Fehlausbruchssignale auftreten.

- Der Ichimoku-Indikator weist eine gewisse Verzögerung auf, die den Einstiegszeitpunkt beeinflussen kann.

- In schnell bewegten Märkten können die dynamischen Stop-Loss-Level zu weit gefasst sein.

- Zu viele Filterbedingungen können die Anzahl der Handelsmöglichkeiten verringern und die Gesamtrendite der Strategie beeinträchtigen.

Optimierungsmöglichkeiten

- Einführung eines Volatilitätsindikators, um Strategieparameter an die Marktvolatilität anzupassen.

- Optimierung der Ichimoku-Parameter für verschiedene Marktumgebungen.

- Hinzufügen einer Volumenanalyse zur Verbesserung der Signalzuverlässigkeit.

- Einführung eines Zeitfilters, um Phasen hoher Volatilität zu vermeiden.

- Entwicklung eines adaptiven Parameteroptimierungssystems für eine dynamische Anpassung der Strategie.

Zusammenfassung

Die Strategie kombiniert mehrere technische Indikatoren zu einem vollständigen Handelssystem. Sie legt nicht nur Wert auf die Signalerzeugung, sondern beinhaltet auch ein umfassendes Risikomanagement. Durch die mehrstufigen Filter wird die Erfolgsrate der Trades effektiv erhöht. Gleichzeitig sorgt das dynamische Stop-Loss-Design für ein gutes Risiko-Ertrags-Verhältnis. Obwohl es Optimierungspotenzial gibt, handelt es sich insgesamt um ein strukturell vollständiges und logisch klares Strategiesystem.

- 1