Erweiterte Fair-Value-Lücken-Erkennungsstrategie basierend auf dynamischem Risikomanagement und festem Gewinn

Übersicht

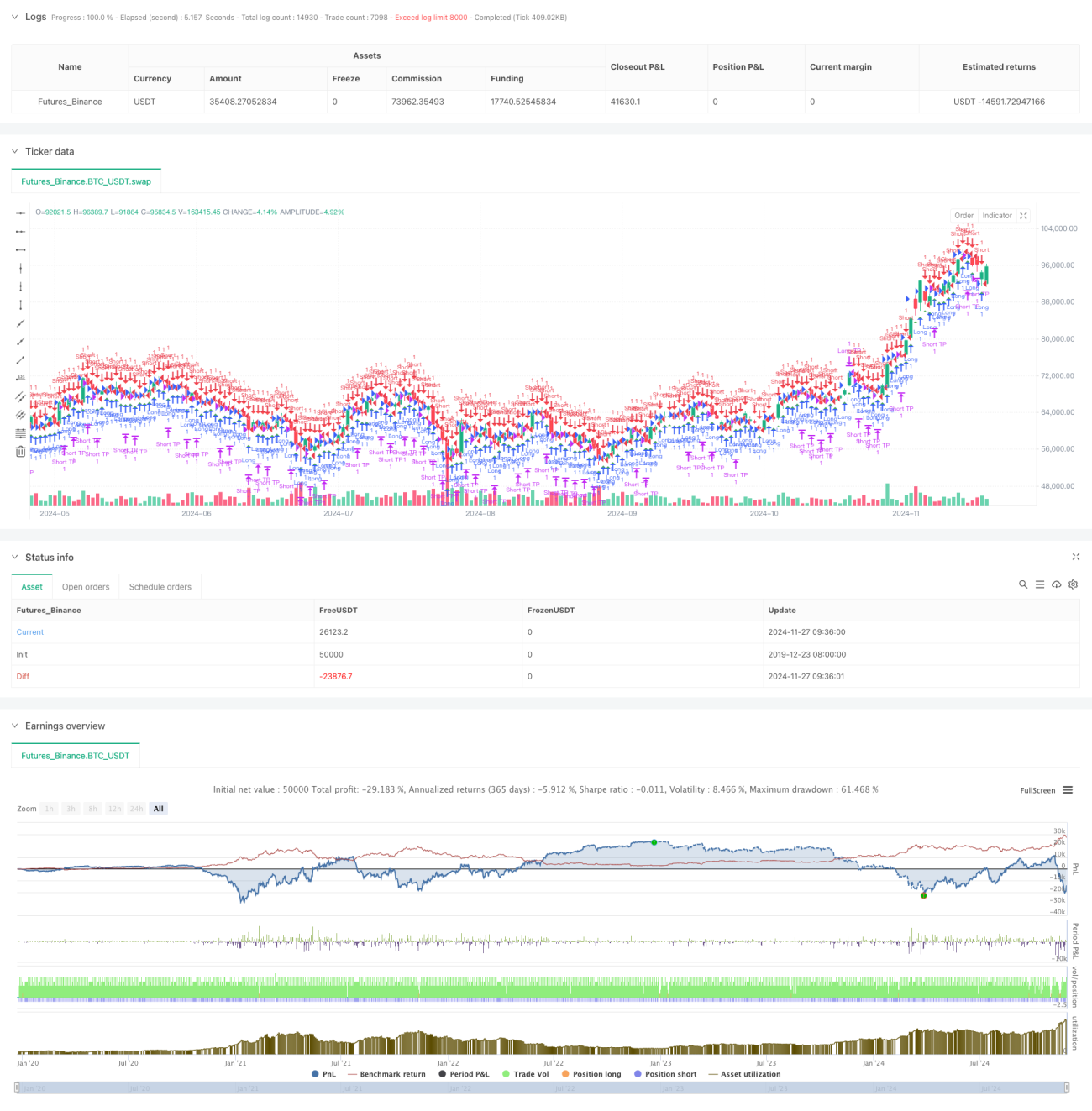

Diese Handelsstrategie basiert auf Fair-Value-Gaps (FVG) und kombiniert dynamisches Risikomanagement mit festen Gewinnzielen. Die Strategie läuft im 15-Minuten-Zeitraum und erkennt Preislücken im Markt, um potenzielle Handelsmöglichkeiten zu identifizieren. Laut Backtest-Daten erzielte die Strategie zwischen November 2023 und August 2024 eine Nettorendite von 284,40 % bei insgesamt 153 abgeschlossenen Trades, einer Gewinnrate von 71,24 % und einem Profitfaktor von 2,422.

Strategieprinzip

Der Kern der Strategie besteht darin, Fair-Value-Gaps durch die Überwachung der Preisbeziehungen zwischen drei aufeinanderfolgenden Kerzen zu identifizieren. Im Einzelnen:

- Bedingung für eine Long-FVG: Das Hoch der vorherigen Kerze liegt unter dem Tief der vorletzten Kerze.

- Bedingung für eine Short-FVG: Das Tief der vorherigen Kerze liegt über dem Hoch der vorletzten Kerze.

- Das Einstiegssignal wird durch den FVG-Schwellenwertparameter gesteuert; ein Trade wird nur ausgelöst, wenn die Lücke einen bestimmten Prozentsatz des Preises überschreitet.

- Das Risikomanagement verwendet einen festen Prozentsatz des Eigenkapitals (1 %) als Stop-Loss.

- Das Gewinnziel wird als feste Punktzahl (50 Punkte) festgelegt.

Strategievorteile

- Wissenschaftliches Risikomanagement: Der Stop-Loss auf Basis des Eigenkapitalanteils ermöglicht eine dynamische Risikosteuerung.

- Klare Handelsregeln: Ein festes Gewinnziel vermeidet subjektive Entscheidungen.

- Hervorragende Leistung: Die hohe Gewinnrate und der Profitfaktor weisen auf eine gute Stabilität der Strategie hin.

- Einfache Umsetzung: Der Code ist klar strukturiert, leicht verständlich und wartbar.

- Anpassungsfähigkeit: Parameter können an unterschiedliche Marktbedingungen angepasst werden.

Strategierisiken

- Marktvolatilitätsrisiko: In hochvolatilen Märkten kann das feste Gewinnziel zu unflexibel sein.

- Slippage-Risiko: Häufiger Handel kann zu hohen Slippage-Kosten führen.

- Parameterabhängigkeit: Die Performance hängt stark von der Einstellung des FVG-Schwellenwerts ab.

- Risiko falscher Ausbrüche: Einige FVG-Signale könnten falsche Ausbrüche sein, die zusätzliche Bestätigungsindikatoren erfordern.

- Kapitalmanagement-Risiko: Ein fester Stop-Loss-Prozentsatz kann bei Verlustserien zu einem schnellen Kapitalabbau führen.

Optimierungsansätze

- Einführung von Marktvolatilitätsindikatoren zur dynamischen Anpassung des Gewinnziels.

- Hinzufügen eines Trendfilters, um Trades in Seitwärtsmärkten zu vermeiden.

- Entwicklung eines Mehrfach-Zeitrahmen-Bestätigungsmechanismus.

- Optimierung des Positionsgrößen-Algorithmus, Einführung eines gleitenden Positionssystems.

- Hinzufügen von Handelszeitfiltern, um volatile Handelszeiten zu vermeiden.

- Entwicklung eines Signalstärke-Bewertungssystems zur Auswahl qualitativ hochwertiger Handelsmöglichkeiten.

Fazit

Die Strategie kombiniert die Fair-Value-Gap-Theorie mit wissenschaftlichem Risikomanagement und zeigt gute Handelsergebnisse. Die hohe Gewinnrate und der stabile Profitfaktor weisen auf ihren praktischen Wert hin. Mit den vorgeschlagenen Optimierungen gibt es noch Raum für Verbesserungen. Es wird empfohlen, vor dem Live-Einsatz ausreichende Parameteroptimierungen und Backtests durchzuführen.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1