Mehrstufige volatilitätsadaptive dynamische SuperTrend-Strategie

Übersicht

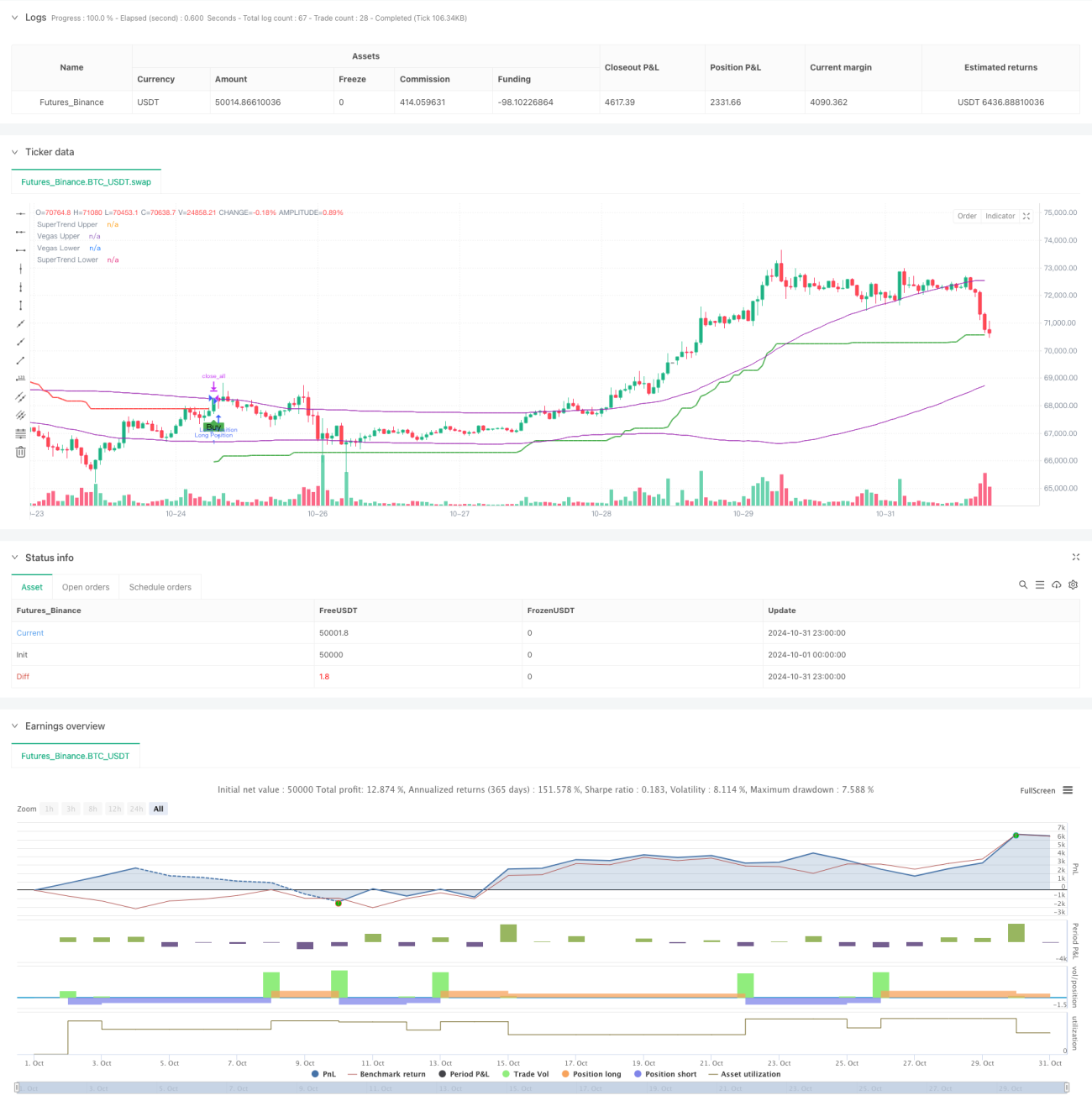

Die Mehrstufige Volatilitätsadaptive Dynamische SuperTrend-Strategie ist ein innovatives Handelssystem, das den Vegas-Kanal und den SuperTrend-Indikator kombiniert. Ihre Besonderheit liegt in der dynamischen Anpassungsfähigkeit an die Marktvolatilität sowie der Nutzung eines mehrstufigen Take-Profit-Mechanismus zur Optimierung des Risiko-Ertrags-Verhältnisses. Durch die Verbindung der Volatilitätsanalyse des Vegas-Kanals mit der Trendverfolgungsfunktion des SuperTrends passt die Strategie ihre Parameter automatisch an sich ändernde Marktbedingungen an und liefert so präzisere Handelssignale.

Strategieprinzip

Die Funktionsweise der Strategie basiert auf drei Kernkomponenten: der Berechnung des Vegas-Kanals, der Trenderkennung und dem mehrstufigen Take-Profit-Mechanismus. Der Vegas-Kanal verwendet den einfachen gleitenden Durchschnitt (SMA) und die Standardabweichung (STD), um die Preisschwankungsbreite zu definieren. Der SuperTrend-Indikator bestimmt die Trendrichtung auf Basis des angepassten ATR-Werts. Bei einer Trendänderung im Markt generiert das System Handelssignale. Der mehrstufige Take-Profit-Mechanismus ermöglicht das schrittweise Ausstieg zu unterschiedlichen Preisniveaus, was einerseits Gewinne sichert und andererseits einen Teil der Position weiterhin am potenziellen Gewinn teilhaben lässt. Die Einzigartigkeit der Strategie liegt im Volatilitätsanpassungsfaktor, der den SuperTrend-Multiplikator dynamisch an die Breite des Vegas-Kanals anpasst.

Strategievorteile

- Dynamische Anpassungsfähigkeit: Der Volatilitätsanpassungsfaktor ermöglicht eine automatische Reaktion auf unterschiedliche Marktbedingungen.

- Risikomanagement: Der mehrstufige Take-Profit-Mechanismus bietet eine systematische Lösung zur Gewinnmitnahme.

- Anpassbarkeit: Mehrere Parametereinstellungen stehen zur Verfügung, um unterschiedliche Handelsstile zu bedienen.

- Umfassende Marktabdeckung: Unterstützt sowohl Long- als auch Short-Handel.

- Visuelles Feedback: Klare grafische Oberfläche erleichtert Analyse und Entscheidungsfindung.

Strategierisiken

- Parameterempfindlichkeit: Unterschiedliche Parameterkombinationen können zu stark abweichenden Strategieleistungen führen.

- Verzögerung: Auf gleitenden Durchschnitten basierende Indikatoren weisen eine gewisse Verzögerung auf.

- Falsche Ausbrüche: In Seitwärtsmärkten können Fehlsignale auftreten.

- Abwägung bei Take-Profit-Einstellungen: Zu frühe Take-Profit-Level können große Trends verpassen, zu späte Take-Profit-Level können bereits erzielte Gewinne zunichtemachen.

Optimierungsrichtungen

- Einführung eines Marktumfeld-Filters zur Anpassung der Strategieparameter an unterschiedliche Marktbedingungen.

- Integration einer Volumenanalyse zur Erhöhung der Signalzuverlässigkeit.

- Entwicklung eines adaptiven Take-Profit-Mechanismus, der die Take-Profit-Niveaus dynamisch an die Marktvolatilität anpasst.

- Einbindung weiterer technischer Indikatoren zur Signalbestätigung.

- Implementierung eines dynamischen Positionsmanagements, das die Handelsgröße an das Marktrisiko anpasst.

Zusammenfassung

Die Mehrstufige Volatilitätsadaptive Dynamische SuperTrend-Strategie repräsentiert eine fortschrittliche quantitative Handelsmethode. Durch die Kombination mehrerer technischer Indikatoren und eines innovativen Take-Profit-Mechanismus bietet sie Tradern ein umfassendes Handelssystem. Ihre dynamische Anpassungsfähigkeit und das Risikomanagement machen sie besonders geeignet für den Einsatz in unterschiedlichen Marktumgebungen, mit guter Erweiterbarkeit und Optimierungspotenzial. Durch kontinuierliche Verbesserung und Optimierung verspricht die Strategie in Zukunft stabilere Handelsergebnisse.

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Multi-Step Vegas SuperTrend - strategy [presentTrading]", shorttitle="Multi-Step Vegas SuperTrend - strategy [presentTrading]", overlay=true, precision=3, commission_value=0.1, commission_type=strategy.commission.percent, slippage=1, currency=currency.USD)

// Input settings allow the user to customize the strategy's parameters.- 1