Gemischte adaptive Strategie aus doppeltem gleitendem Durchschnitt und relativer Stärke

Überblick

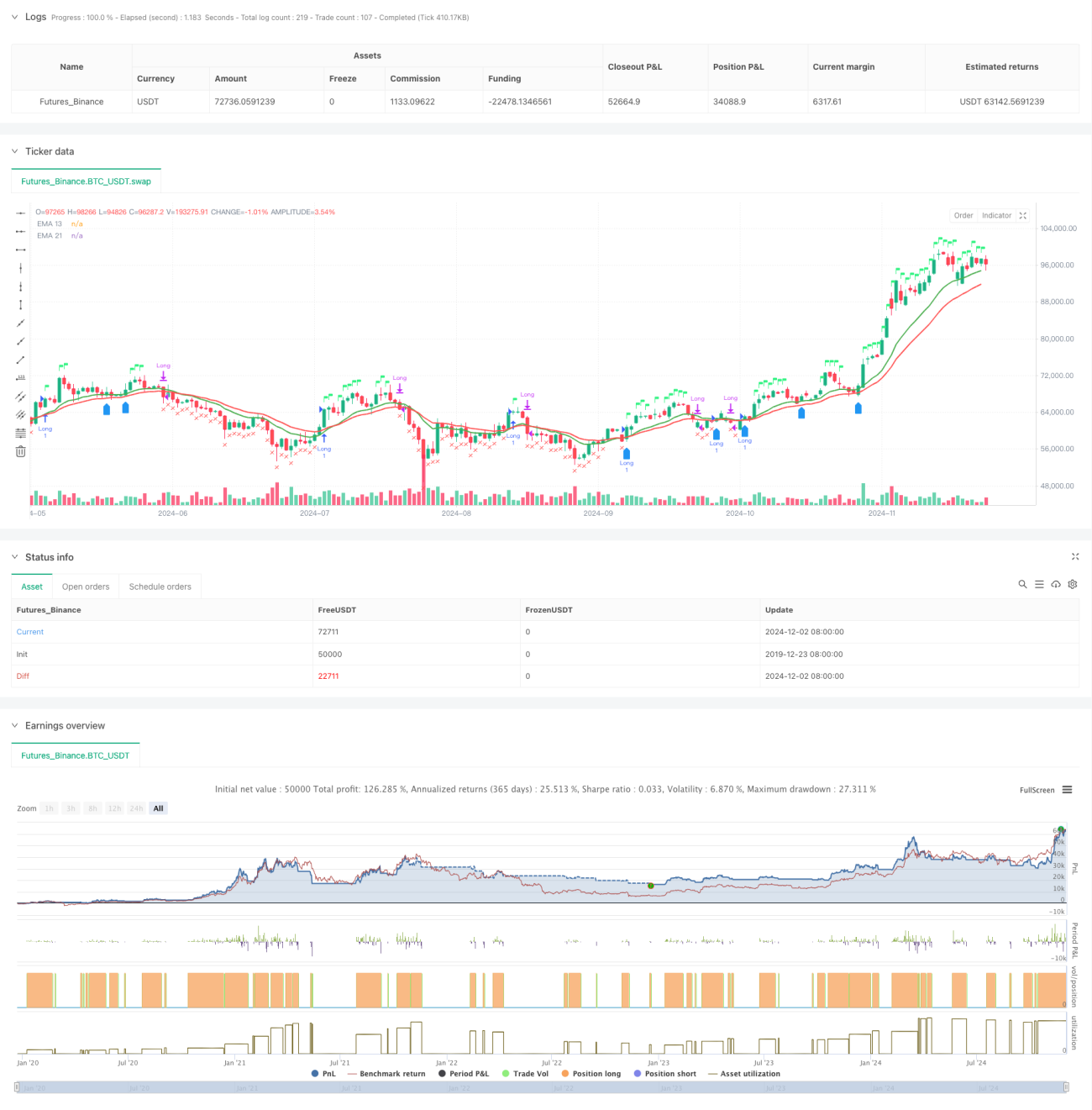

Diese Strategie ist ein umfassendes Handelssystem, das eine Kombination aus zwei gleitenden Durchschnitten, dem Relative-Stärke-Index (RSI) und der relativen Stärke (RS) verwendet. Die Strategie bestätigt Trends durch den Schnittpunkt der exponentiell gleitenden Durchschnitte (EMA) für 13 und 21 Tage, während sie gleichzeitig den RSI und den RS-Wert im Vergleich zum Referenzindex zur Bestätigung von Handelssignalen nutzt, und realisiert so einen mehrdimensionalen Entscheidungsmechanismus. Die Strategie enthält außerdem eine Risikokontrollmechanismus basierend auf dem 52-Wochen-Hoch sowie eine Bewertung der Wiedereinstiegsbedingungen.

Strategieprinzip

Die Strategie verwendet einen mehrfachen Signalbestätigungsmechanismus:

- Eingangssignale müssen gleichzeitig die folgenden Bedingungen erfüllen:

- EMA13 kreuzt über EMA21 oder der Preis liegt über EMA13

- RSI größer als 60

- Relative Stärke (RS) positiv

- Ausstiegsbedingungen umfassen:

- Preis fällt unter EMA21

- RSI unter 50

- RS wird negativ

- Wiedereinstiegsbedingungen:

- Preis kreuzt über EMA13 und EMA13 größer als EMA21

- RS bleibt positiv

- Oder Preis durchbricht das Hoch der Vorwoche

Strategievorteile

- Der mehrfache Signalbestätigungsmechanismus reduziert das Risiko von Fehlausbrüchen

- Kombination mit relativer Stärke-Analyse filtert effektiv starke Instrumente

- Verwendung eines adaptiven Zeitperioden-Anpassungsmechanismus

- Umfassendes Risikokontrollsystem

- Intelligenter Wiedereinstiegsmechanismus

- Echtzeit-Visualisierung des Handelsstatus

Strategierisiken

- Seitwärtsmärkte können zu häufigen Trades führen

- Abhängigkeit von mehreren Indikatoren kann zu Signalverzögerungen führen

- Feste RSI-Schwellenwerte sind möglicherweise nicht an alle Marktbedingungen angepasst

- Die Berechnung der relativen Stärke hängt von der Genauigkeit des Referenzindex ab

- Der 52-Wochen-Hoch-Stopp könnte zu locker sein

Optimierungsmöglichkeiten

- Einführung adaptiver RSI-Schwellenwerte

- Optimierung der Logik zur Bewertung von Wiedereinstiegsbedingungen

- Hinzufügen einer Handelsvolumen-Analyse-Dimension

- Verbesserung des Gewinnmitnahme- und Stop-Loss-Mechanismus

- Integration eines Volatilitätsfilters

- Optimierung des Berechnungszeitraums der relativen Stärke

Zusammenfassung

Die Strategie baut durch die Kombination von technischer Analyse und relativer Stärke-Analyse ein umfassendes Handelssystem auf. Ihr mehrfacher Signalbestätigungsmechanismus und ihr Risikokontrollsystem verleihen ihr eine hohe Praktikabilität. Durch die vorgeschlagenen Optimierungsrichtungen gibt es noch Raum für Verbesserungen. Die erfolgreiche Umsetzung der Strategie erfordert ein tiefes Verständnis des Marktes seitens des Händlers sowie eine angemessene Parametereinstellung entsprechend den Eigenschaften des jeweiligen Handelsinstruments.

- 1