Überblick

Diese Strategie ist ein fortschrittliches Handelssystem, das auf der Analyse von Pivot-Punkten basiert. Es identifiziert potenzielle Trendumkehrungen durch das Erkennen wichtiger Wendepunkte im Markt. Die Strategie verwendet eine innovative "Pivot der Pivots"-Methode und kombiniert diese mit dem Volatilitätsindikator ATR für das Positionsmanagement, um ein vollständiges Handelssystem zu bilden. Sie ist auf mehrere Märkte anwendbar und kann je nach den Eigenschaften des jeweiligen Marktes durch Parameteroptimierung angepasst werden.

Strategieprinzip

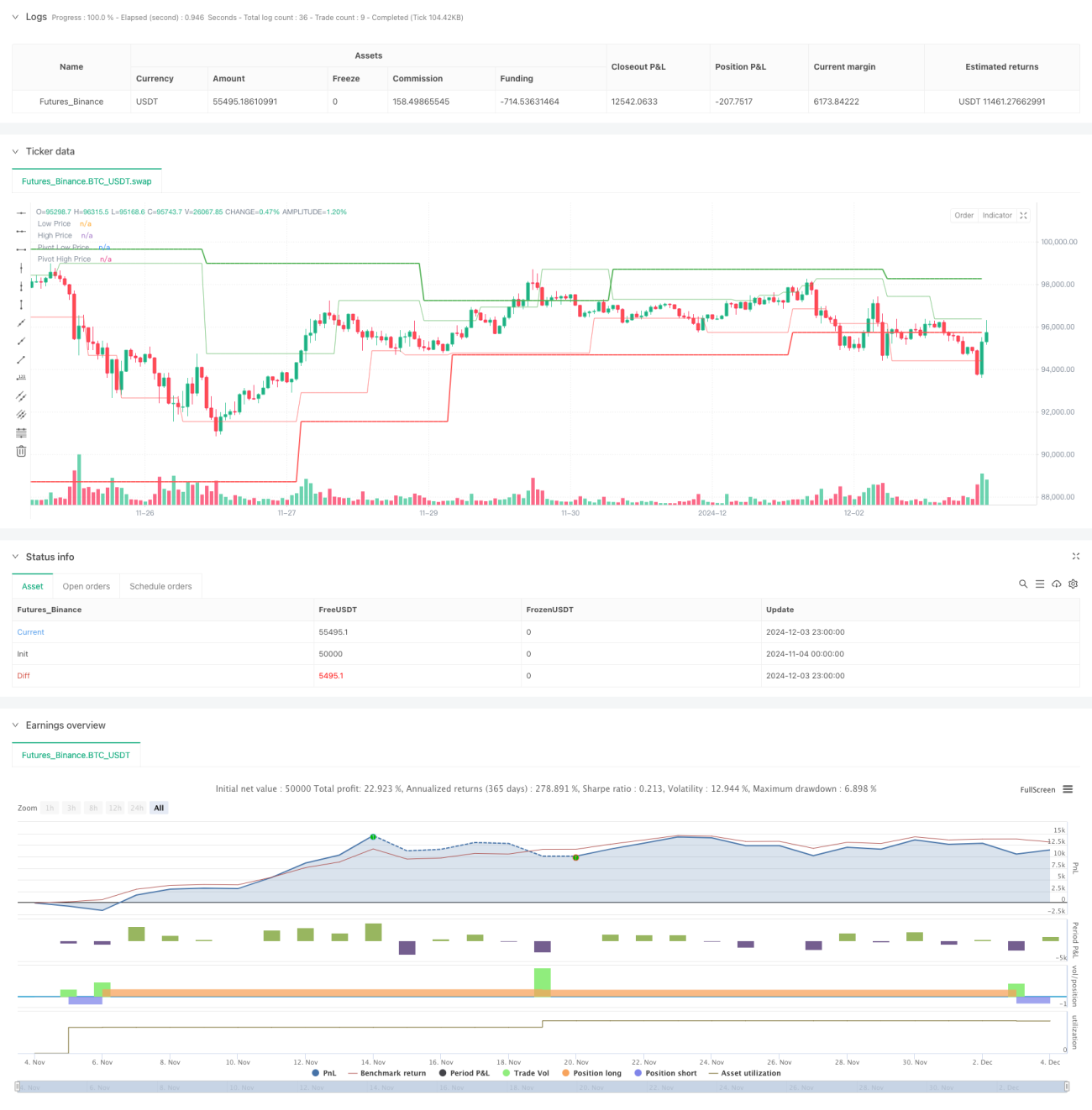

Der Kern der Strategie besteht darin, Marktumkehrchancen durch eine zweistufige Analyse von Pivot-Punkten zu identifizieren. Die erste Stufe umfasst grundlegende Hoch- und Tiefpunkte, die zweite Stufe filtert signifikante Wendepunkte innerhalb dieser ersten Pivot-Punkte heraus. Wenn der Preis diese entscheidenden Niveaus durchbricht, generiert das System Handelssignale. Gleichzeitig wird der ATR-Indikator verwendet, um die Marktvolatilität zu messen, die zur Bestimmung von Stop-Loss- und Take-Profit-Niveaus sowie der Positionsgröße dient.

Strategievorteile

- Hohe Anpassungsfähigkeit: Die Strategie kann sich an unterschiedliche Marktumgebungen anpassen, indem Parameter an verschiedene Volatilitätsniveaus angepasst werden.

- Umfassendes Risikomanagement: Durch die dynamische Stop-Loss-Setzung mittels ATR werden Schutzmaßnahmen automatisch an die Marktvolatilität angepasst.

- Mehrstufige Bestätigung: Die zweistufige Pivot-Punkt-Analyse reduziert das Risiko von Fehlausbrüchen.

- Flexibles Positionsmanagement: Die Positionsgröße wird dynamisch an das Kontovolumen und die Marktvolatilität angepasst.

- Klare Einstiegsregeln: Ein eindeutiger Signalbestätigungsmechanismus minimiert subjektive Entscheidungen.

Strategierisiken

- Slippage-Risiko: In Märkten mit hoher Volatilität kann es zu erheblichen Slippage kommen.

- Risiko von Fehlausbrüchen: Bei seitwärts gerichteten Märkten können falsche Signale entstehen.

- Übermäßiges Hebelrisiko: Unsachgemäße Nutzung von Hebeln kann zu schweren Verlusten führen.

- Risiko der Parameteroptimierung: Übermäßige Optimierung kann zu Overfitting führen.

Optimierungsmöglichkeiten der Strategie

- Signalfilterung: Hinzufügen eines Trendfilters, um nur in Richtung des Haupttrends zu handeln.

- Dynamische Parameter: Automatische Anpassung der Pivot-Punkt-Parameter basierend auf dem Marktzustand.

- Mehrere Zeitrahmen: Erhöhung der Genauigkeit durch Bestätigung über mehrere Zeitrahmen.

- Intelligente Stop-Loss: Entwicklung intelligenterer Stop-Loss-Strategien, wie z. B. Trailing-Stop-Loss.

- Risikokontrolle: Hinzufügen weiterer Risikokontrollmaßnahmen, wie z. B. Korrelationsanalysen.

Zusammenfassung

Dies ist eine gut konzipierte Trendumkehr-Handelsstrategie, die durch zweistufige Pivot-Punkt-Analyse und ATR-Volatilitätsmanagement ein robustes Handelssystem aufbaut. Ihre Stärken liegen in der hohen Anpassungsfähigkeit und dem umfassenden Risikomanagement. Dennoch müssen Händler Hebelwirkungen vorsichtig einsetzen und die Parameter kontinuierlich optimieren. Durch die vorgeschlagenen Optimierungsmöglichkeiten bietet die Strategie weiteres Verbesserungspotenzial. Sie eignet sich für konservative Händler und stellt ein Handelssystem dar, das eine eingehende Untersuchung und praktische Anwendung verdient.

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Pivot of Pivot Reversal Strategy [MAD]", shorttitle="PoP Reversal Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

// Inputs with Tooltips- 1