Übersicht

Dies ist eine mehrstufige Handelsstrategie, die eine adaptive Berechnung des Average True Range (ATR) mit einer momentum-basierten Trenddetektion kombiniert. Das markanteste Merkmal dieser Strategie ist ihr einzigartiger 7-stufiger Gewinnmechanismus, der vier ATR-basierte Ausstiegsniveaus mit drei festen prozentualen Niveaus kombiniert. Dieser hybride Ansatz ermöglicht es Händlern, dynamisch auf die Marktvolatilität zu reagieren und gleichzeitig systematisch Gewinne in Long- und Short-Märkten zu erzielen. Die Strategie bietet Händlern eine umfassende Handelslösung durch die Kombination von dynamischer ATR-Anpassung, Trendstärkeerkennung und mehreren Gewinnmechanismen.

Strategieprinzip

Der Kern der Strategie funktioniert durch folgende Schlüsselkomponenten:

- Erweiterte True-Range-Berechnung: Misst die Marktvolatilität, indem die signifikantesten Kursbewegungen berücksichtigt werden.

- Integration des Momentum-Faktors: Passt den ATR basierend auf den jüngsten Kursbewegungen an, um ihn anpassungsfähiger zu machen.

- Adaptiver ATR: Passt den traditionellen ATR in Abhängigkeit vom Momentum-Faktor an, sodass er in volatilen Phasen sensibler reagiert.

- Quantifizierung der Trendstärke: Bewertet die Stärke des Trends durch einen komplexen Algorithmus.

- Siebenstufiger Gewinnmechanismus: Umfasst vier ATR-basierte Ausstiegsniveaus und drei feste prozentuale Niveaus.

Strategievorteile

- Hohe Anpassungsfähigkeit: Passt sich durch dynamische ATR-Berechnung an verschiedene Marktbedingungen an.

- Umfassendes Risikomanagement: Der mehrstufige Gewinnmechanismus bietet eine systematische Risikosteuerung.

- Hohe Flexibilität: Kann gleichermaßen effektiv in Long- und Short-Märkten operieren.

- Einstellbare Parameter: Bietet mehrere anpassbare Parameter, um unterschiedlichen Handelsstilen gerecht zu werden.

- Systematische Umsetzung: Klare Einstiegs- und Ausstiegsregeln reduzieren emotionales Trading.

Strategierisiken

- Parameterempfindlichkeit: Falsche Parametereinstellungen können zu Überhandel oder verpassten Chancen führen.

- Abhängigkeit von Marktbedingungen: In stark volatilen oder seitwärts tendierenden Märkten kann die Performance nachlassen.

- Komplexitätsrisiko: Der mehrstufige Gewinnmechanismus kann die Ausführung erschweren.

- Slippage-Einfluss: Mehrere Gewinnpunkte können erheblich von Slippage betroffen sein.

- Kapitalanforderungen: Erfordert ausreichend Kapital zur Umsetzung der mehrstufigen Gewinnstrategie.

Optimierungsrichtungen

- Dynamische Parameteranpassung: Automatische Anpassung der Parameter je nach Marktsituation.

- Marktumfeld-Filter: Hinzufügen eines Mechanismus zur Erkennung des Marktumfelds.

- Verbessertes Risikomanagement: Einführung eines dynamischen Stop-Loss-Mechanismus.

- Ausführungsoptimierung: Vereinfachung des Gewinnmechanismus zur Reduzierung von Slippage-Effekten.

- Verbesserung des Backtesting-Rahmens: Einbeziehung weiterer realer Handelsfaktoren.

Zusammenfassung

Diese Strategie bietet Händlern durch die Kombination von adaptivem ATR und einem mehrstufigen Gewinnmechanismus ein umfassendes Handelssystem. Ihr Vorteil liegt in der Fähigkeit, sich an verschiedene Marktbedingungen anzupassen und gleichzeitig Risiken auf systematische Weise zu managen. Obwohl einige potenzielle Risiken bestehen, kann die Strategie durch geeignete Optimierung und Risikomanagement zu einem effektiven Handelswerkzeug werden. Ihr innovativer mehrstufiger Gewinnmechanismus eignet sich besonders für Händler, die bei gleichzeitiger Risikokontrolle Gewinne maximieren möchten.

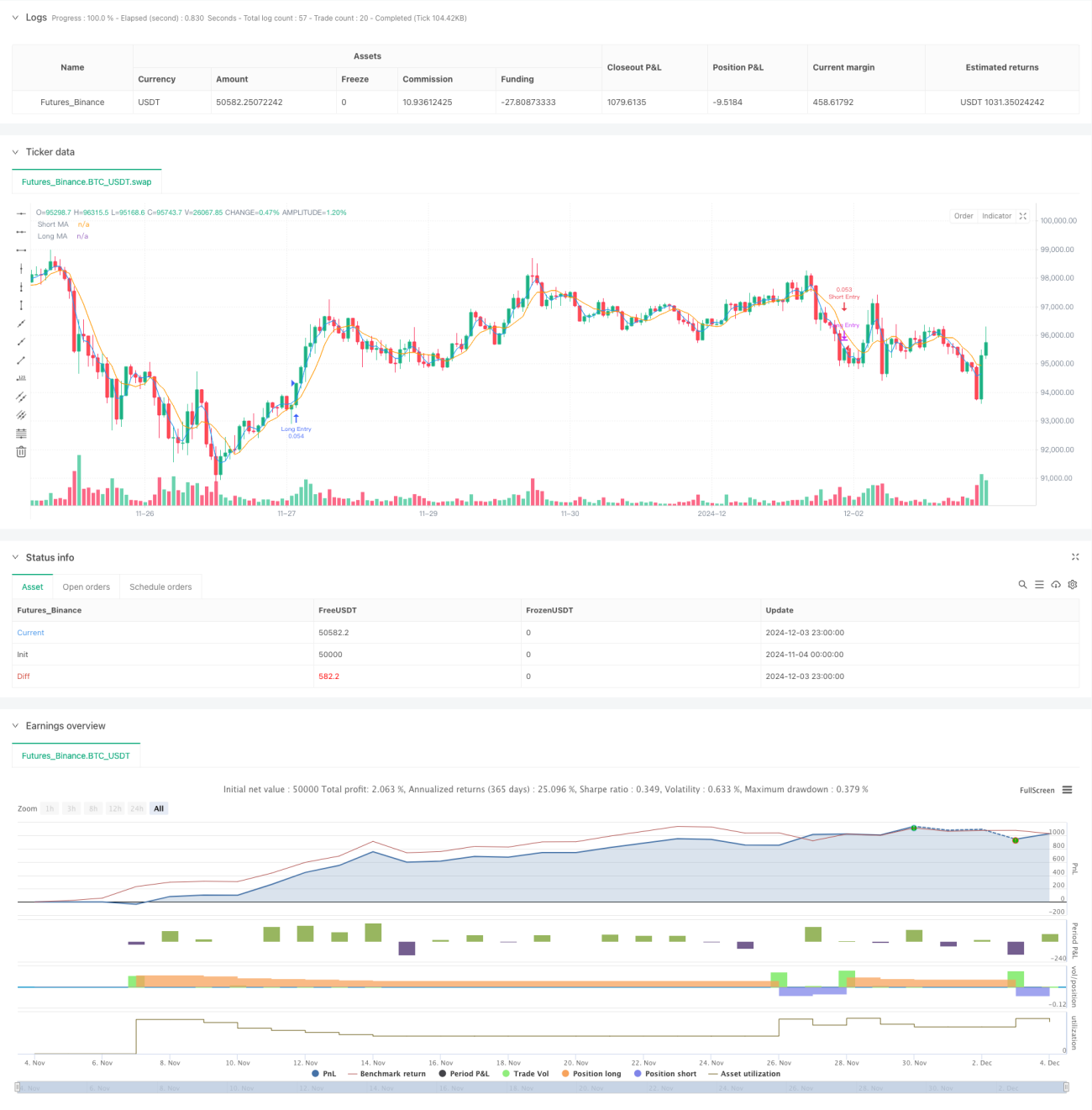

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The SuperATR 7-Step Profit Strategy is a multi-layered trading strategy that combines adaptive ATR and momentum-based trend detection - 1