RSI Mean-Reversion-Breakout-Strategie

Strategieübersicht

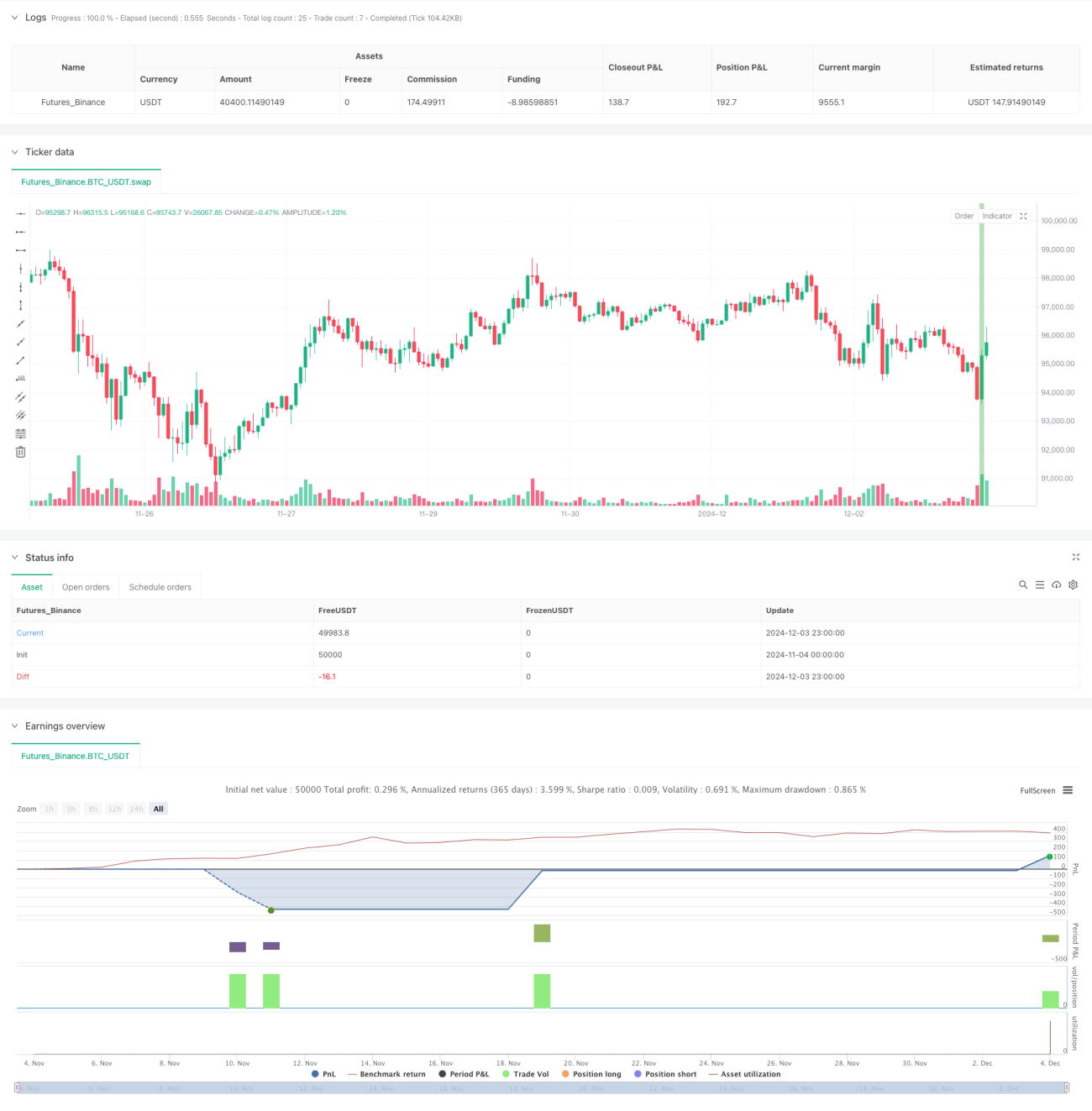

Diese Strategie ist ein quantitatives Handelssystem, das auf dem RSI-Indikator und dem Prinzip der Mean Reversion basiert. Es erkennt überkaufte und überverkaufte Marktzustände und nutzt die Preisspanne sowie die Position des Schlusskurses, um Marktwende-Chancen zu erfassen. Der Kerngedanke der Strategie besteht darin, nach extremen Marktzuständen nach Umkehrungen zu suchen und das Risiko durch strenge Einstiegsbedingungen und dynamische Stop-Losses zu managen.

Strategieprinzip

Die Strategie verwendet einen mehrstufigen Filtermechanismus, um Handelssignale zu bestimmen: Zunächst muss der Preis ein 10-Perioden-Tief erreichen, was auf einen überverkauften Markt hindeutet. Zweitens muss die Preisspanne des aktuellen Tages die größte der letzten 10 Handelstage sein, was auf erhöhte Volatilität hinweist. Schließlich wird durch die Prüfung, ob der Schlusskurs im oberen Quartil der täglichen Preisspanne liegt, ein mögliches Umkehrsignal bestätigt. Der Einstieg erfolgt als Ausbruch: Innerhalb von 2 Handelstagen nach Erfüllung der Bedingungen wird eine Long-Position eröffnet, wenn der Preis das vorherige Hoch durchbricht. Der Stop-Loss wird als nachlaufender Stop (Trailing Stop) ausgeführt, um Gewinne zu schützen.

Strategievorteile

- Mehrere Filterbedingungen erhöhen die Signalqualität und reduzieren Fehlsignale.

- Kombiniert mehrere Dimensionen der technischen Analyse wie Preisformation, Volatilität und Momentum.

- Der nachlaufende Stop-Loss schützt Gewinne effektiv.

- Der Einstiegsmechanismus nutzt eine Ausbruchsbestätigung, um vorzeitige Positionierungen zu vermeiden.

- Die Handelslogik ist klar, leicht verständlich und umsetzbar.

Strategierisiken

- In starken Trendmärkten kann es zu häufigen Stop-Loss-Auslösungen kommen.

- Die strengen Einstiegsbedingungen können dazu führen, dass einige Handelsmöglichkeiten verpasst werden.

- Eine hohe Handelsfrequenz kann höhere Transaktionskosten verursachen.

- In einem Umfeld geringer Volatilität können nur schwer gültige Handelssignale gefunden werden.

- Der Stop-Loss könnte zu konservativ sein und die Gesamtrendite beeinträchtigen.

Optimierungsmöglichkeiten

- Ein Trendfilter könnte eingeführt werden, der in starken Trendphasen den Handel pausiert.

- Die Einbeziehung von Volumenindikatoren als zusätzliche Bestätigung wäre denkbar.

- Die Stop-Loss-Einstellungen könnten optimiert werden, indem sie dynamisch an die Marktvolatilität angepasst werden.

- Eine Begrenzung der Haltedauer könnte zu lange Seitwärtsbewegungen vermeiden.

- Mehrperiodenanalyse könnte die Signalzuverlässigkeit verbessern.

Zusammenfassung

Es handelt sich um eine strukturell vollständige und logisch klare Mean-Reversion-Strategie. Durch mehrstufige Bedingungsfilter und dynamisches Stop-Loss-Management kann die Strategie unter Risikokontrolle effektiv Markt-Abprall-Chancen nach Übertreibungen nutzen. Obwohl es einige Einschränkungen gibt, kann die Gesamtleistung der Strategie durch sinnvolle Optimierungen und Verbesserungen gesteigert werden. Anleger wird empfohlen, bei der praktischen Anwendung Parameter an die spezifischen Marktgegebenheiten und die eigene Risikotoleranz anzupassen.

- 1