Erweiterte dynamische Trailing-Stop- und Zielgewinnstrategie

Überblick

Diese Strategie ist ein fortschrittliches Handelssystem, das dynamisches Trailing-Stop-Loss, Risiko-Ertrags-Verhältnis und RSI-Extremausstiege kombiniert. Die Strategie identifiziert spezifische Marktformationen (parallele Kerzenformationen und Nadelkerzenformationen) für den Einstieg, nutzt gleichzeitig ATR und das jüngste Tief zur dynamischen Stop-Loss-Platzierung und legt das Gewinnziel auf Basis eines vorgegebenen Risiko-Ertrags-Verhältnisses fest. Das System integriert zudem einen auf dem RSI-Indikator basierenden Mechanismus zur Erkennung überhitzter/überkühlter Märkte, der bei Erreichen von Extremwerten eine rechtzeitige Positionsschließung auslöst.

Strategieprinzip

Die Kernlogik der Strategie umfasst die folgenden Hauptbestandteile:

- Einstiegssignale basieren auf zwei Formationen: Parallele Kerzenformation (großer bullish Kerze gefolgt von großer bearish Kerze) und Doppelnadelkerzenformation.

- Das dynamische Trailing-Stop-Loss verwendet einen ATR-Multiplikator für den Tiefstpreis der letzten N Kerzen, um sicherzustellen, dass der Stop-Loss sich dynamisch an die Marktvolatilität anpassen kann.

- Das Gewinnziel wird auf Basis eines festen Risiko-Ertrags-Verhältnisses festgelegt, indem der Risikowert (R) jeder Transaktion berechnet wird.

- Die Positionsgröße wird dynamisch auf Basis eines festen Risikobetrags und des Risikowerts jeder Transaktion berechnet.

- Der RSI-Extremausstiegsmechanismus löst bei Überhitzung oder Überkühlung des Marktes ein Schlusssignal aus.

Strategievorteile

- Dynamisches Risikomanagement: Durch die Kombination von ATR und dem jüngsten Tief kann der Stop-Loss dynamisch an die Marktvolatilität angepasst werden.

- Präzise Positionskontrolle: Die auf einem festen Risikobetrag basierende Positionsberechnungsmethode gewährleistet ein konsistentes Risiko pro Transaktion.

- Mehrdimensionale Ausstiegsmechanismen: Kombination aus Trailing-Stop, festem Gewinnziel und RSI-Extremausstieg als Dreifach-Ausstiegsmechanismus.

- Flexible Handelsrichtungsauswahl: Möglichkeit, nur Long, nur Short oder beide Richtungen zu handeln.

- Klares Risiko-Ertrags-Setup: Festlegung des Gewinnziels jeder Transaktion durch ein vorgegebenes Risiko-Ertrags-Verhältnis.

Strategierisiken

- Risiko der Formationserkennungsgenauigkeit: Die Identifizierung paralleler Kerzen und Nadelkerzen kann fehlerhaft sein.

- Slippage-Risiko bei Stop-Loss: In stark volatilen Märkten kann es zu erheblichen Slippage kommen.

- RSI-Extremausstieg kann zu früh erfolgen: In starken Trendmärkten kann dies zu vorzeitigem Ausstieg und verpassten Gewinnen führen.

- Einschränkungen des festen Risiko-Ertrags-Verhältnisses: Das optimale Risiko-Ertrags-Verhältnis kann je nach Marktumfeld variieren.

- Risiko der Überoptimierung von Parametern: Die Kombination mehrerer Parameter kann zu einer Überoptimierung führen.

Optimierungsrichtungen der Strategie

- Optimierung der Einstiegssignale: Hinzufügen weiterer Bestätigungsindikatoren wie Volumen, Trendindikatoren usw.

- Dynamisches Risiko-Ertrags-Verhältnis: Anpassung des Risiko-Ertrags-Verhältnisses basierend auf der Marktvolatilität.

- Intelligente Parameteradaptivität: Einführung von maschinellen Lernalgorithmen zur dynamischen Optimierung der Parameter.

- Mehrfachzeitrahmen-Bestätigung: Hinzufügen von Signalbestätigungen aus mehreren Zeitrahmen.

- Marktumfeldklassifizierung: Verwendung unterschiedlicher Parametersätze je nach Marktumfeld.

Zusammenfassung

Diese Strategie ist ein durchdachtes Handelssystem, das durch die Kombination mehrerer etablierter technischer Analysekonzepte ein vollständiges Handelssystem aufbaut. Der Vorteil der Strategie liegt in ihrem umfassenden Risikomanagement-Rahmenwerk und den flexiblen Handelsregeln. Allerdings sind auch die Parameteroptimierung und die Marktanpassungsfähigkeit zu beachten. Durch die vorgeschlagenen Optimierungsrichtungen besteht noch weiteres Verbesserungspotenzial für die Strategie.

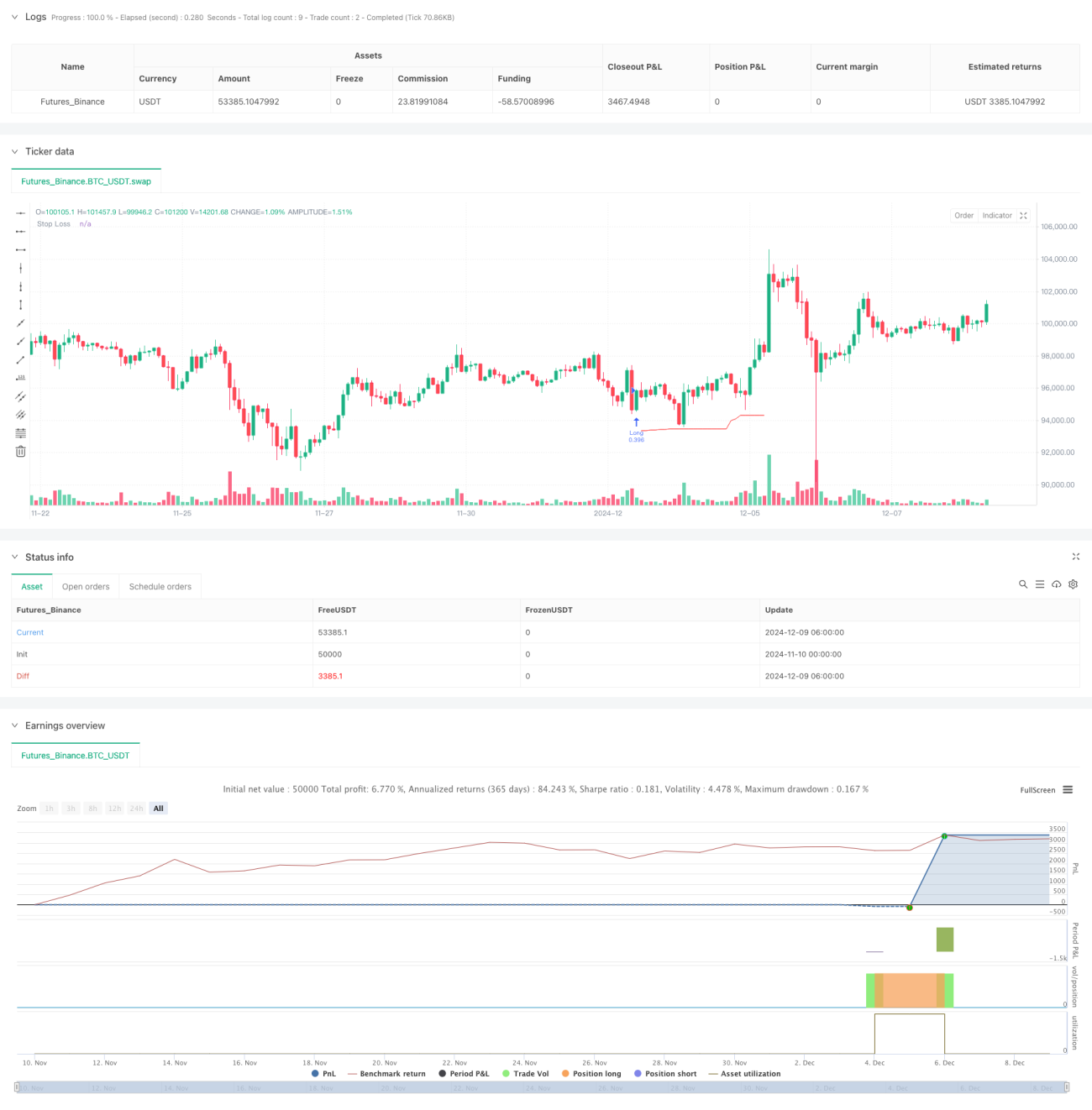

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 2h

basePeriod: 2h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading | www.TheArtOfTrading.com

// @version=5

strategy("Trailing stop 1", overlay=true)- 1