SMA-RSI-MACD Multi-Indikator-Kombination Dynamische Limit-Order-Trading-Strategie

Überblick

Diese Strategie ist ein Handelssystem, das mehrere technische Indikatoren kombiniert. Es basiert hauptsächlich auf der Bestätigung durch ein dreifaches Signal: EMA-Kreuzung, RSI-Überverkauft und MACD-Golden Cross, um Positionen zu eröffnen, und nutzt dynamische Limit-Orders sowie mehrere Ausstiegsmechanismen zur Risikosteuerung. Die Strategie verwendet den exponentiellen gleitenden Durchschnitt (EMA) der Perioden 9 und 21 als primären Trendindikator, kombiniert mit dem Relative-Stärke-Index (RSI) und dem Moving Average Convergence Divergence (MACD) zur Filterung von Handelssignalen. Das Risiko wird durch die Festlegung des Limit-Order-Abstands sowie fester Take-Profit- und Stop-Loss-Punkte kontrolliert.

Prinzip der Strategie

Der Kern der Handelslogik umfasst folgende Schlüsselkomponenten:

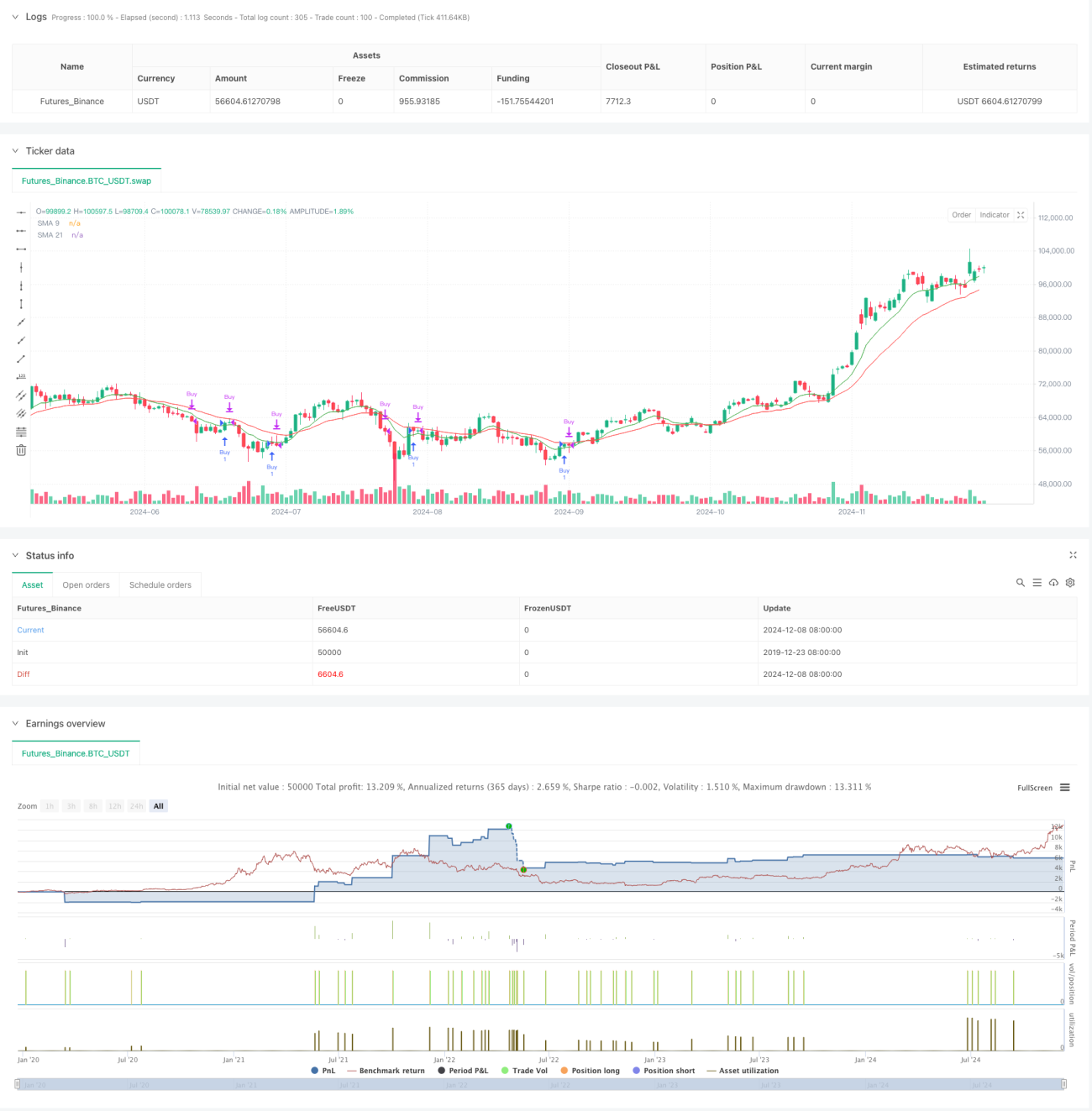

- Das Einstiegssignal wird ausgelöst, wenn der 9-Perioden-EMA den 21-Perioden-EMA von unten nach oben kreuzt.

- Der Einstiegspreis wird als Limit-Order unterhalb des 9-Perioden-EMA mit einer festgelegten Punktedistanz gesetzt.

- Die Handelsbestätigung erfordert gleichzeitig, dass der RSI unter dem festgelegten Schwellenwert liegt und der MACD ein Golden Cross aufweist.

- Zu den Ausstiegssignalen gehören das MACD-Death Cross, festgelegte Take-Profit- und Stop-Loss-Punkte sowie die Zwangsglattstellung bei Börsenschluss.

- Die Handelszeit ist auf den Zeitraum nach 9:30 Uhr bis vor 15:10 Uhr beschränkt.

Die Strategie verwendet die Einstiegsmethode über Limit-Orders, um Positionen zu besseren Preisen eröffnen zu können, und erhöht durch die Kombination mehrerer technischer Indikatoren die Genauigkeit der Trades.

Vorteile der Strategie

- Die mehrfache Signalbestätigung erhöht die Zuverlässigkeit der Trades.

- Die Einstiegsmethode über Limit-Orders ermöglicht günstigere Ausführungskurse.

- Feste Take-Profit- und Stop-Loss-Punkte erleichtern die Risikosteuerung.

- Die Zwangsglattstellung bei Börsenschluss vermeidet Übernachtrisiken.

- Die zeitliche Beschränkung vermeidet die Volatilität zum Handelsstart.

- Der EMA reagiert schneller auf Trends.

- Die Kombination von RSI und MACD kann falsche Signale herausfiltern.

Risiken der Strategie

- Die mehrfache Signalbestätigung kann dazu führen, dass einige Handelsmöglichkeiten verpasst werden.

- Limit-Orders können aufgrund schneller Kursbewegungen nicht ausgeführt werden.

- Feste Stop-Loss-Punkte können in Zeiten hoher Volatilität zu größeren Verlusten führen.

- MACD-Signale können zeitlich verzögert sein.

- Die Strategie berücksichtigt keine Änderungen der Marktvolatilität.

- Die Parameteroptimierung birgt das Risiko einer Überanpassung.

Optimierungsmöglichkeiten

- Einführung adaptiver Take-Profit- und Stop-Loss-Punkte, die dynamisch an die Marktvolatilität angepasst werden.

- Hinzufügen von Volumenindikatoren als zusätzliches Bestätigungssignal.

- Integration eines Trendstärkefilters.

- Optimierung der Berechnungsmethode für den Limit-Order-Abstand, z.B. dynamische Anpassung mittels ATR.

- Einbeziehung von Marktstimmungsindikatoren, um ungünstige Marktbedingungen herauszufiltern.

- Integration eines Positionsmanagement-Systems, das die Positionsgröße basierend auf der Signalstärke anpasst.

Zusammenfassung

Es handelt sich um eine vollständig strukturierte, logisch klare Multi-Indikator-Handelsstrategie. Sie identifiziert Trends über das gleitende Durchschnittssystem, filtert Signale über RSI und MACD und kontrolliert Risiken durch Limit-Orders und mehrere Stop-Mechanismen. Die Stärke der Strategie liegt in der hohen Signalzuverlässigkeit und der umfassenden Risikosteuerung. Allerdings gibt es auch Probleme wie Signalverzögerungen und Parameteroptimierung. Durch die Einführung dynamischer Parameteranpassungen und zusätzlicher Indikatoren bietet die Strategie noch erhebliches Optimierungspotenzial. Sie eignet sich für konservative Anleger in klar trendbestimmten Marktumgebungen.

- 1