Multi-Perioden-Trend-Dynamische-Volatilitäts-Tracking-Strategie

Übersicht

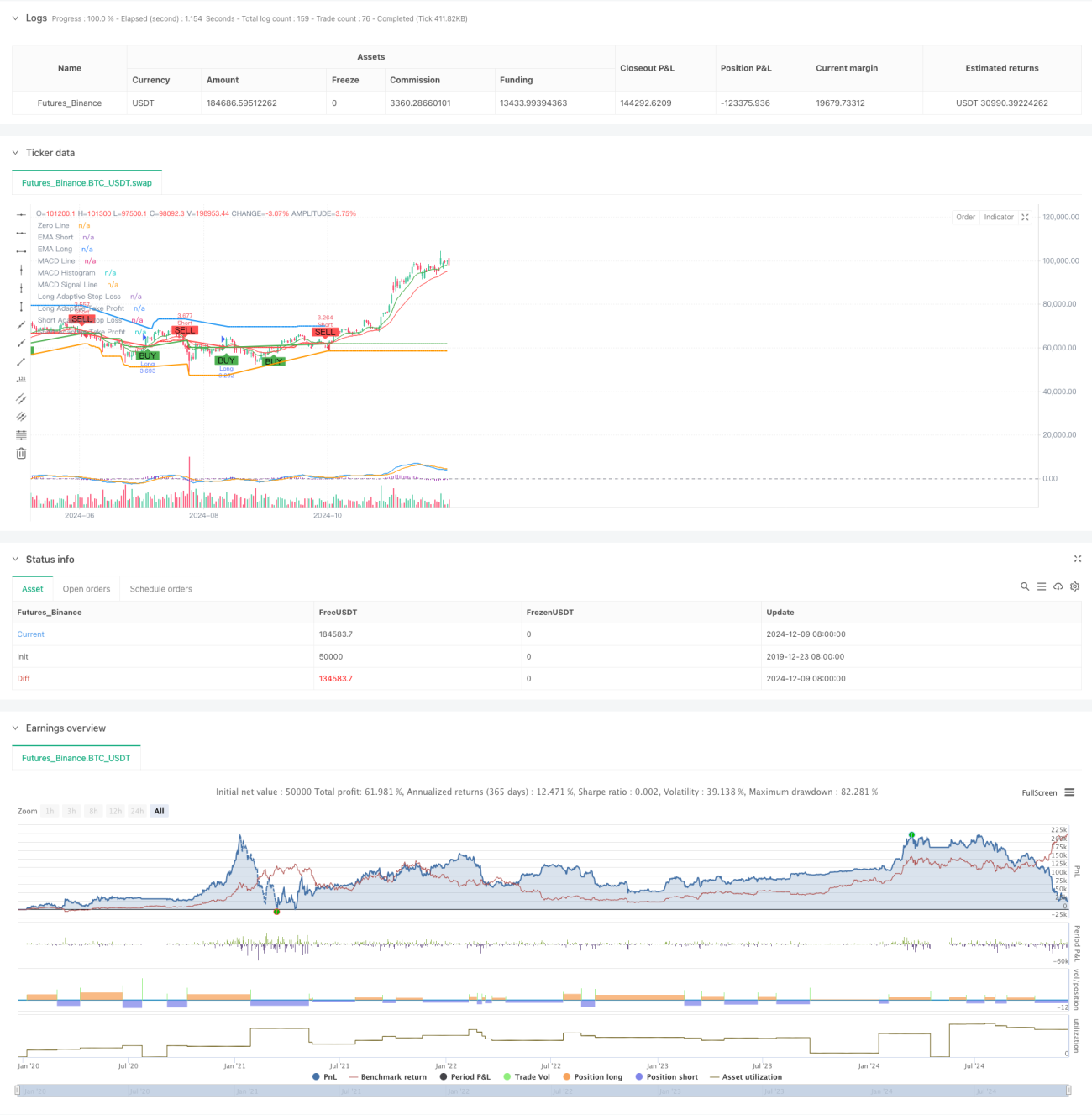

Diese Strategie ist ein adaptives Trendfolgesystem, das mehrere technische Indikatoren kombiniert. Durch Mehrperiodenanalyse und dynamische Anpassung von Stop-Loss und Take-Profit wird die Handelsleistung optimiert. Kern der Strategie ist die Identifizierung von Trends mithilfe von gleitenden Durchschnitten, die Bestätigung der Trendstärke durch RSI und MACD sowie die dynamische Anpassung der Risikomanagementparameter basierend auf dem ATR.

Funktionsweise der Strategie

Die Strategie verwendet einen dreifachen Bestätigungsmechanismus für Trades: 1) Bestimmung der Trendrichtung durch den Crossover von schnellem und langsamen EMA; 2) Filterung von Handelssignalen durch überkaufte/überverkaufte RSI-Niveaus und MACD-Trendbestätigung; 3) Einbeziehung eines EMA eines höheren Zeitrahmens zur Trendbestätigung. Im Risikomanagement werden Stop-Loss und Gewinnziele dynamisch auf Basis des ATR angepasst, was eine adaptive Positionsverwaltung ermöglicht. Bei steigender Marktvolatilität werden die Stop-Loss- und Gewinnzonen automatisch erweitert; bei ruhigeren Märkten werden sie enger gesetzt, um die Erfolgsquote zu erhöhen.

Vorteile der Strategie

- Die mehrdimensionale Signalbestätigung verbessert die Handelsgenauigkeit erheblich.

- Die adaptive Einstellung von Stop-Loss und Take-Profit passt sich besser an unterschiedliche Marktbedingungen an.

- Die Trendbestätigung über einen höheren Zeitrahmen reduziert effektiv das Risiko von Fehlausbrüchen.

- Ein umfassendes Benachrichtigungssystem hilft, Handelsmöglichkeiten rechtzeitig zu erkennen und Risiken zu kontrollieren.

- Die flexible Ausrichtung der Trades ermöglicht eine Anpassung an verschiedene Handelspräferenzen.

Risiken der Strategie

- Der mehrfache Bestätigungsmechanismus kann dazu führen, dass schnelle Marktbewegungen verpasst werden.

- In stark volatilen Märkten kann der dynamische Stop-Loss zu früh ausgelöst werden.

- In Seitwärtsmärkten können häufige Fehlsignale auftreten.

- Bei der Parameteroptimierung besteht das Risiko einer Überanpassung (Overfitting).

- Mehrperiodenanalysen können zu widersprüchlichen Signalen auf verschiedenen Zeitrahmen führen.

Optimierungsmöglichkeiten

- Einführung eines Volumenindikators als zusätzliche Bestätigung zur Steigerung der Signalzuverlässigkeit.

- Entwicklung eines quantitativen Bewertungssystems für die Trendstärke zur Verbesserung des Einstiegszeitpunkts.

- Entwicklung eines adaptiven Optimierungsmechanismus für Parameter zur Erhöhung der Strategiestabilität.

- Integration eines Systems zur Klassifizierung des Marktumfelds, um je nach Marktlage unterschiedliche Parameter zu verwenden.

- Entwicklung eines dynamischen Positionsmanagementsystems, das die Positionsgröße an die Signalstärke anpasst.

Zusammenfassung

Diese Strategie ist ein sorgfältig konzipiertes Trendfolgesystem, das durch mehrstufige Bestätigungsmechanismen und dynamisches Risikomanagement eine umfassende Handelslösung bietet. Die Kernvorteile liegen in der Anpassungsfähigkeit und der Risikokontrolle. Bei der Anwendung ist jedoch auf die Abstimmung von Parameteroptimierung und Marktumfeld zu achten. Durch kontinuierliche Optimierung und Verbesserung kann die Strategie voraussichtlich unter verschiedenen Marktbedingungen eine stabile Performance erzielen.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("TrenGuard Adaptive ATR Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Parameters- 1