Multi-Zeitrahmen-Trendfolge mit ATR-Take-Profit-und-Stop-Loss-Strategie

Überblick

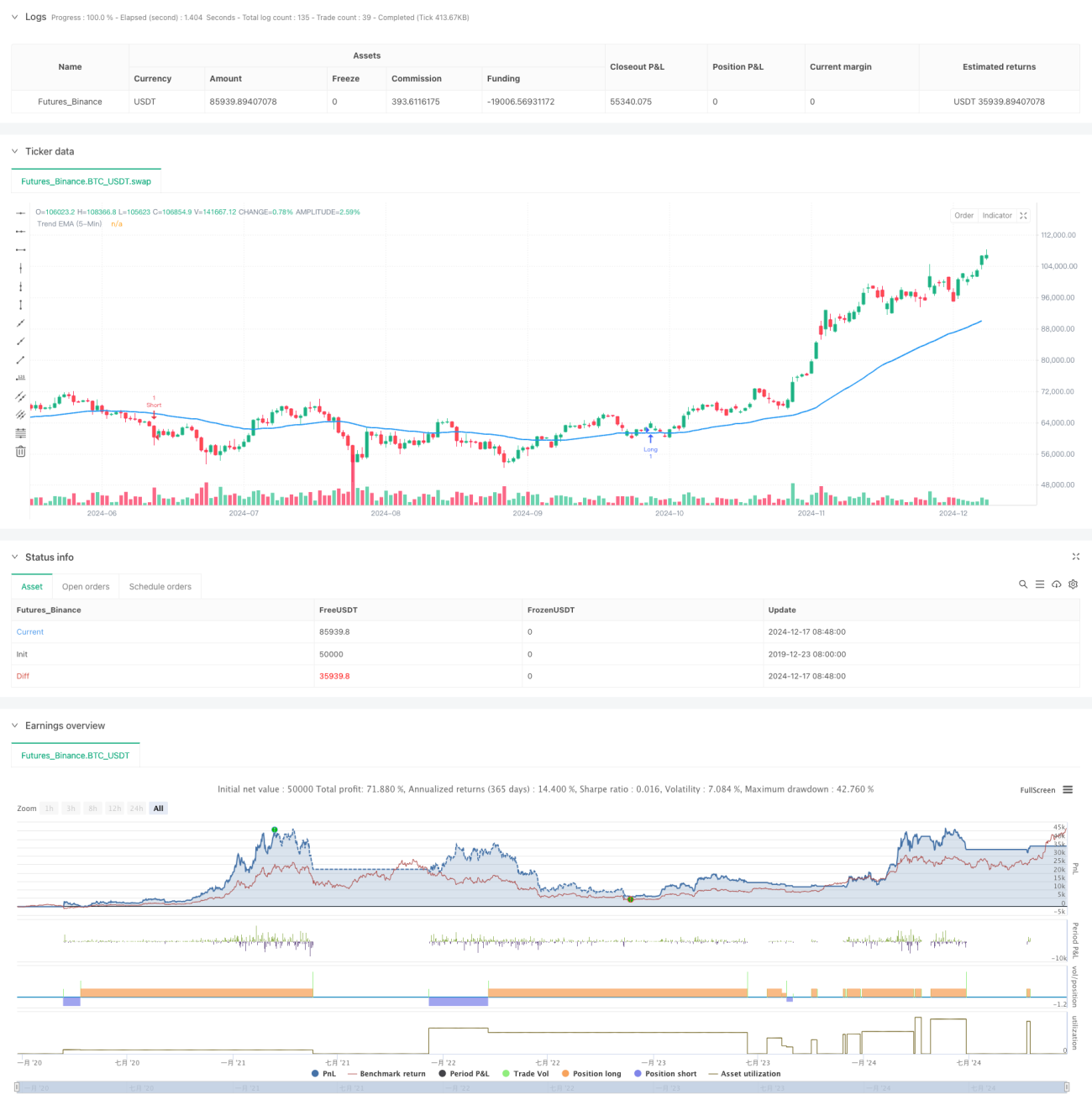

Dies ist eine Trendfolge-Handelsstrategie, die den UT Bot mit einem 50-Perioden exponentiellen gleitenden Durchschnitt (EMA) kombiniert. Die Strategie wird hauptsächlich im 1-Minuten-Zeitrahmen für kurzfristige Trades eingesetzt, während der Trend im 5-Minuten-Zeitrahmen als Richtungsfilter dient. Sie verwendet den ATR-Indikator zur dynamischen Berechnung von Stop-Loss-Positionen und setzt zwei Take-Profit-Ziele zur Optimierung der Erträge ein.

Strategieprinzip

Die Kernlogik der Strategie basiert auf folgenden Schlüsselkomponenten:

- Verwendung des UT Bot zur Berechnung dynamischer Unterstützungs- und Widerstandsniveaus

- Nutzung des 50-Perioden-EMA im 5-Minuten-Zeitrahmen zur Bestimmung des übergeordneten Trends

- Kombination des 21-Perioden-EMA mit UT Bot-Signalen zur Bestimmung konkreter Einstiegspunkte

- Dynamisches Trailing-Stop-Loss mittels ATR-Multiplikator

- Setzen von zwei Take-Profit-Zielen (0,5 % und 1 %), um jeweils 50 % der Position zu schließen

Wenn der Preis die vom UT Bot berechneten Unterstützungs-/Widerstandsniveaus durchbricht und der 21-Perioden-EMA mit dem UT Bot kreuzt, wird ein Handelssignal ausgelöst, sofern der Preis in die richtige Richtung des 5-Minuten-50-Perioden-EMA liegt.

Vorteile der Strategie

- Die Kombination mehrerer Zeitrahmen erhöht die Zuverlässigkeit der Trades

- Dynamischer ATR-Stopp passt sich automatisch an die Marktvolatilität an

- Zwei Take-Profit-Ziele balancieren Gewinn und Gewinnrate aus

- Verwendung von Heikin-Ashi-Kerzenkerzen filtert einige Fehldurchbrüche heraus

- Flexible Handelsrichtung (nur Long, nur Short oder beide Richtungen möglich)

Strategierisiken

- Kurzfristiger Handel kann höhere Spread- und Transaktionskosten verursachen

- In seitwärts tendierenden Märkten können häufige Fehlsignale auftreten

- Mehrere Bedingungen können dazu führen, dass potenzielle Handelsmöglichkeiten verpasst werden

- Die ATR-Parameter müssen an unterschiedliche Märkte angepasst werden

Optimierungsrichtungen

- Hinzufügen eines Volumenindikators als zusätzliche Bestätigung

- Einbeziehung weiterer Marktstimmungsindikatoren

- Entwicklung adaptiver Parameter für unterschiedliche Marktvolatilitätsmuster

- Einführung von Handelszeitfenster-Filtern

- Entwicklung eines intelligenteren Positionsmanagementsystems

Zusammenfassung

Die Strategie erstellt ein vollständiges Handelssystem durch die Kombination mehrerer technischer Indikatoren und Zeitrahmen. Sie umfasst nicht nur klare Ein- und Ausstiegsbedingungen, sondern auch ein umfassendes Risikomanagement. Obwohl die Parameter je nach Marktsituation optimiert werden müssen, bietet das Gesamtgerüst eine gute Praktikabilität und Erweiterbarkeit.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

- 1