动态趋势动量优化策略结合G通道指标

Überblick

Diese Strategie ist ein fortschrittliches Trendfolge-Handelssystem, das die G-Channel-, RSI- und MACD-Indikatoren integriert. Es berechnet dynamisch Unterstützungs- und Widerstandszonen und kombiniert diese mit Momentum-Indikatoren, um Handelsmöglichkeiten mit hoher Wahrscheinlichkeit zu identifizieren. Der Kern der Strategie liegt darin, die Markttrends mit dem benutzerdefinierten G-Channel-Indikator zu bestimmen, während RSI und MACD genutzt werden, um Momentumänderungen zu bestätigen und so präzisere Handelssignale zu generieren.

Strategieprinzip

Die Strategie verwendet einen dreifachen Filtermechanismus, um die Zuverlässigkeit der Handelssignale sicherzustellen. Zunächst baut der G-Channel dynamisch Unterstützungs- und Widerstandszonen auf, indem er die höchsten und tiefsten Kurse innerhalb eines bestimmten Zeitraums berechnet. Wenn der Preis den Kanal durchbricht, identifiziert das System potenzielle Trendwenden. Zweitens wird der RSI-Indikator verwendet, um zu bestätigen, ob der Markt überkauft oder überverkauft ist, und so wertvollere Handelsmöglichkeiten herauszufiltern. Schließlich bestätigt der MACD-Indikator durch die positiven und negativen Werte des Histogramms die Richtung und Stärke des Momentums. Nur wenn alle drei Bedingungen erfüllt sind, gibt das System ein Handelssignal aus.

Strategievorteile

- Mehrdimensionale Signalbestätigungsmechanismen verbessern die Handelsgenauigkeit erheblich

- Dynamische Stop-Loss- und Take-Profit-Einstellungen kontrollieren das Risiko effektiv

- Die adaptive Natur des G-Channels ermöglicht der Strategie, sich an verschiedene Marktumgebungen anzupassen

- Vollständiges Risikomanagementsystem, einschließlich Positions- und Geldmanagement

- Visuelles Labelsystem zeigt Handelssignale intuitiv an, was die Analyse und Optimierung erleichtert

Strategierisiken

- In Seitwärtsmärkten können falsche Signale auftreten; eine Identifizierung des Marktumfelds ist erforderlich

- Übermäßige Parameteroptimierung kann zu Überanpassungsrisiken führen

- Mehrere Indikatoren können in Phasen hoher Volatilität zu Verzögerungseffekten führen

- Ungünstig eingestellte Stop-Loss-Niveaus können zu übermäßigen Drawdowns führen

Optimierungsrichtungen der Strategie

- Einführung eines Marktumfeld-Identifikationsmoduls, das je nach Marktzustand unterschiedliche Parametereinstellungen verwendet

- Entwicklung eines adaptiven Stop-Loss-Mechanismus, der die Stop-Loss-Niveaus dynamisch an die Marktvolatilität anpasst

- Hinzufügung von Volumenanalyse-Indikatoren zur Verbesserung der Signalzuverlässigkeit

- Optimierung der Berechnungsmethode des G-Channels zur Reduzierung von Verzögerungseffekten

Zusammenfassung

Die Strategie baut durch die umfassende Nutzung mehrerer technischer Indikatoren ein vollständiges Handelssystem auf. Ihr Kernvorteil liegt im mehrdimensionalen Signalbestätigungsmechanismus und dem vollständigen Risikomanagementsystem. Durch kontinuierliche Optimierung und Verbesserung kann die Strategie voraussichtlich in verschiedenen Marktumgebungen stabile Ergebnisse erzielen. Es wird empfohlen, vor dem Live-Handel verschiedene Parameterkombinationen ausgiebig zu testen und je nach den spezifischen Marktmerkmalen entsprechende Anpassungen vorzunehmen.

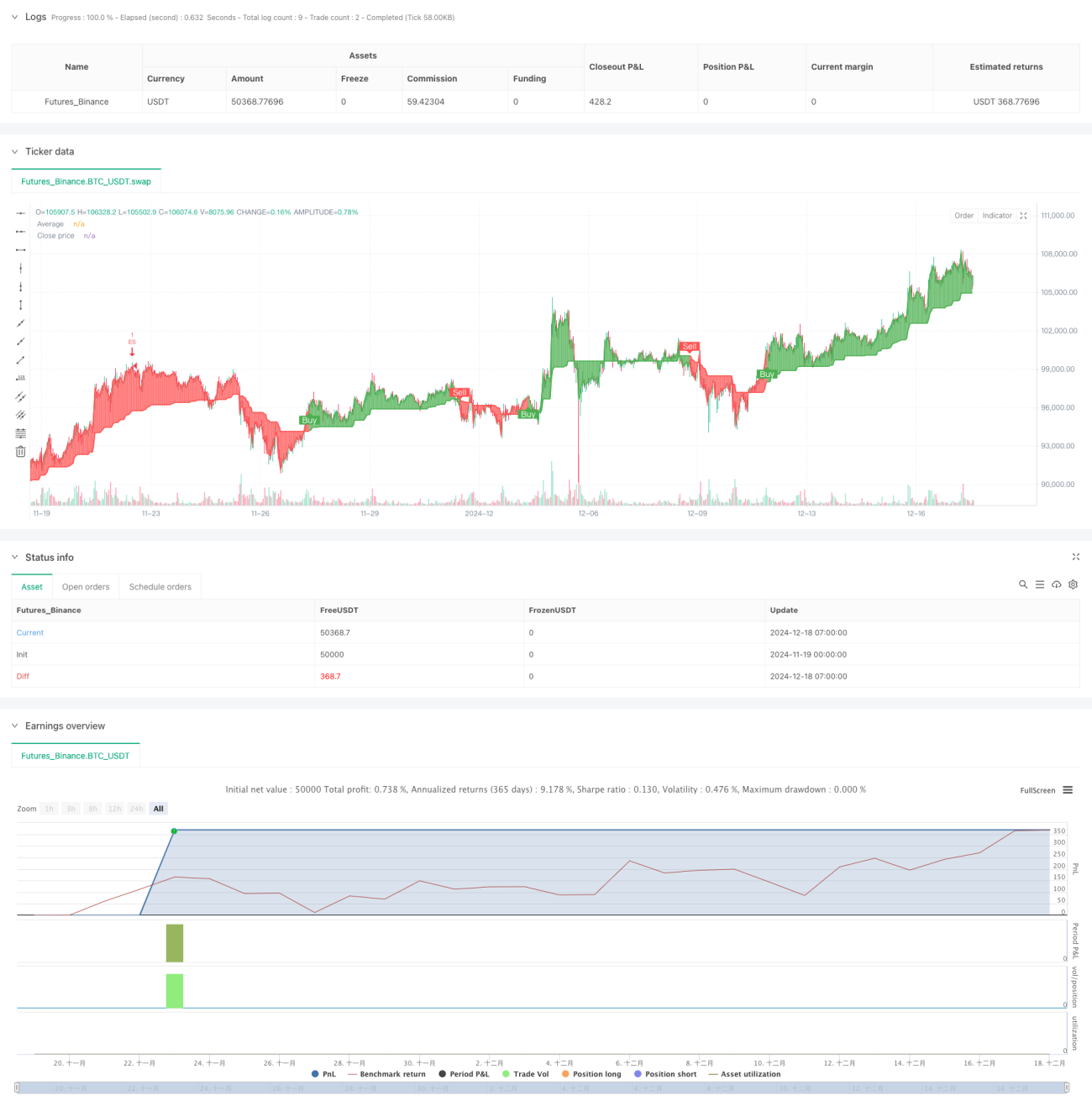

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("VinSpace Optimized Strategy", shorttitle="VinSpace Magic", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input Parameters- 1