Mehrfach-Gleitender-Durchschnitt-Goldenes-Kreuz-Teilweise-Gewinnmitnahme-Strategie

Überblick

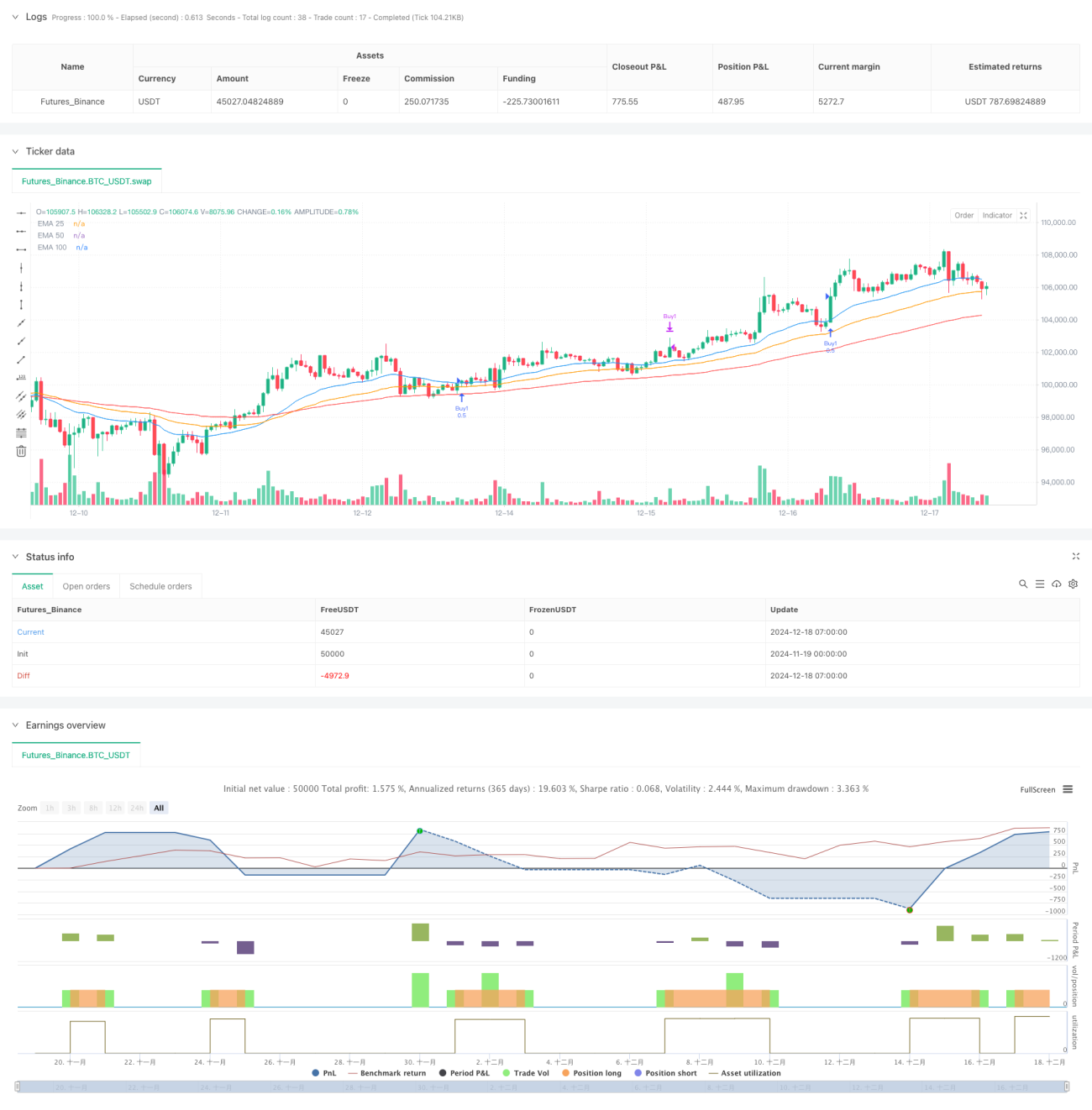

Diese Strategie ist ein Trendfolge-Handelssystem, das auf mehreren exponentiell gleitenden Durchschnitten (EMA) basiert. Sie verwendet den Golden Cross der drei EMAs (EMA25, EMA50 und EMA100), um einen starken Aufwärtstrend zu bestätigen, und steigt bei einem Durchbruch des Preises über den EMA25 in zwei Tranchen ein. Die Strategie setzt dynamische Stopp-Loss- und teilweise Take-Profit-Regeln ein, um Risiken zu managen und Gewinne zu sichern.

Funktionsweise der Strategie

Der Kern der Strategie umfasst folgende Schlüsselelemente:

- Trendbestätigung: Verwendung von drei EMAs mit unterschiedlichen Perioden (25, 50, 100). Wenn der kurzfristige über dem mittelfristigen und der mittelfristige über dem langfristigen EMA liegt, entsteht ein Golden Cross, der einen Aufwärtstrend bestätigt.

- Einstiegssignal: Sobald der Schlusskurs den EMA25 nach oben durchbricht, wird in zwei Tranchen zu je 50 % der Positionsgröße long eingestiegen.

- Stopp-Loss: Dynamischer Stopp-Loss basierend auf dem niedrigsten Kurs der letzten 20 Perioden, mit einem zusätzlichen Puffer (0,0003), um falsche Ausbrüche zu vermeiden.

- Teilweiser Take-Profit: Zwei Take-Profit-Ziele mit unterschiedlichen Multiplikatoren (1,0- und 1,5-fach). Die erste Tranche wird beim niedrigeren Ziel geschlossen, die zweite beim höheren Ziel.

- Trendende-Schutz: Wenn der Preis unter den EMA100 fällt, wird zur Vermeidung von Verlusten durch eine Trendumkehr ein Schließsignal für alle Positionen ausgelöst.

Vorteile der Strategie

- Mehrfachbestätigungsmechanismus: Durch die Kombination mehrerer gleitender Durchschnitte werden Fehlsignale effektiv herausgefiltert und die Zuverlässigkeit der Trades erhöht.

- Dynamisches Risikomanagement: Der Stopp-Loss wird basierend auf der Echtzeit-Marktvolatilität dynamisch angepasst, was die Anpassungsfähigkeit verbessert.

- Gestaffelter Aufbau und Teil-Gewinnmitnahme: Durch die gestaffelte Vorgehensweise können sowohl Gewinne teilweise gesichert als auch laufende Gewinne maximiert werden.

- Trendschutzmechanismus: Der langfristige EMA dient als Frühwarnlinie für Trendumkehrungen, sodass Verluste rechtzeitig begrenzt und große Rücksetzer vermieden werden.

Risiken der Strategie

- Verzögerungsrisiko: Gleitende Durchschnitte sind inhärent verzögert, was zu späten Einstiegen und verpassten optimalen Kaufpunkten führen kann.

- Seitwärtsmarkt-Risiko: In einer Seitwärtsbewegung können häufige Fehlausbrüche zu aufeinanderfolgenden Stopp-Loss-Verlusten führen.

- Risiko des festen Stopp-Loss-Puffers: Ein fester Puffer ist möglicherweise nicht für alle Marktbedingungen geeignet.

- Risiko des Kapitalmanagements: Die feste 50 %-Aufteilung der Positionen kann unflexibel sein.

Optimierungsmöglichkeiten

- Dynamische Parameteroptimierung: Anpassung der EMA-Perioden und des Stopp-Loss-Puffers basierend auf der Marktvolatilität.

- Filterung nach Marktumfeld: Hinzufügen von Trendstärke- und Volatilitätsindikatoren, um Parameter je nach Marktphase anzupassen.

- Optimierung des Positionsmanagements: Dynamische Anpassung der Positionsgröße basierend auf Volatilität und Kontowert.

- Optimierung des Einstiegszeitpunkts: Kombination mit anderen Indikatoren wie RSI oder MACD zur Verbesserung des Einstiegszeitpunkts.

- Optimierung der Gewinnmitnahme: Einführung eines gleitenden Take-Profit-Mechanismus, um bereits erzielte Gewinne besser zu schützen.

Zusammenfassung

Diese Strategie bildet durch die Kombination mehrerer gleitender Durchschnitte und gestaffelter Vorgehensweise ein relativ vollständiges Trendfolge-Handelssystem. Der Vorteil liegt in der Verknüpfung von Trendfolge und Risikomanagement, jedoch müssen Parameter und Regeln je nach tatsächlicher Marktsituation optimiert werden. Mit den vorgeschlagenen Optimierungsrichtungen kann die Strategie auch unter verschiedenen Marktbedingungen stabile Ergebnisse erzielen.

- 1