Kollaborative Trendfluktuations-Handelsstrategie mit mehreren gleitenden Durchschnitten basierend auf dynamischer ATR-Risikokontrolle

Überblick

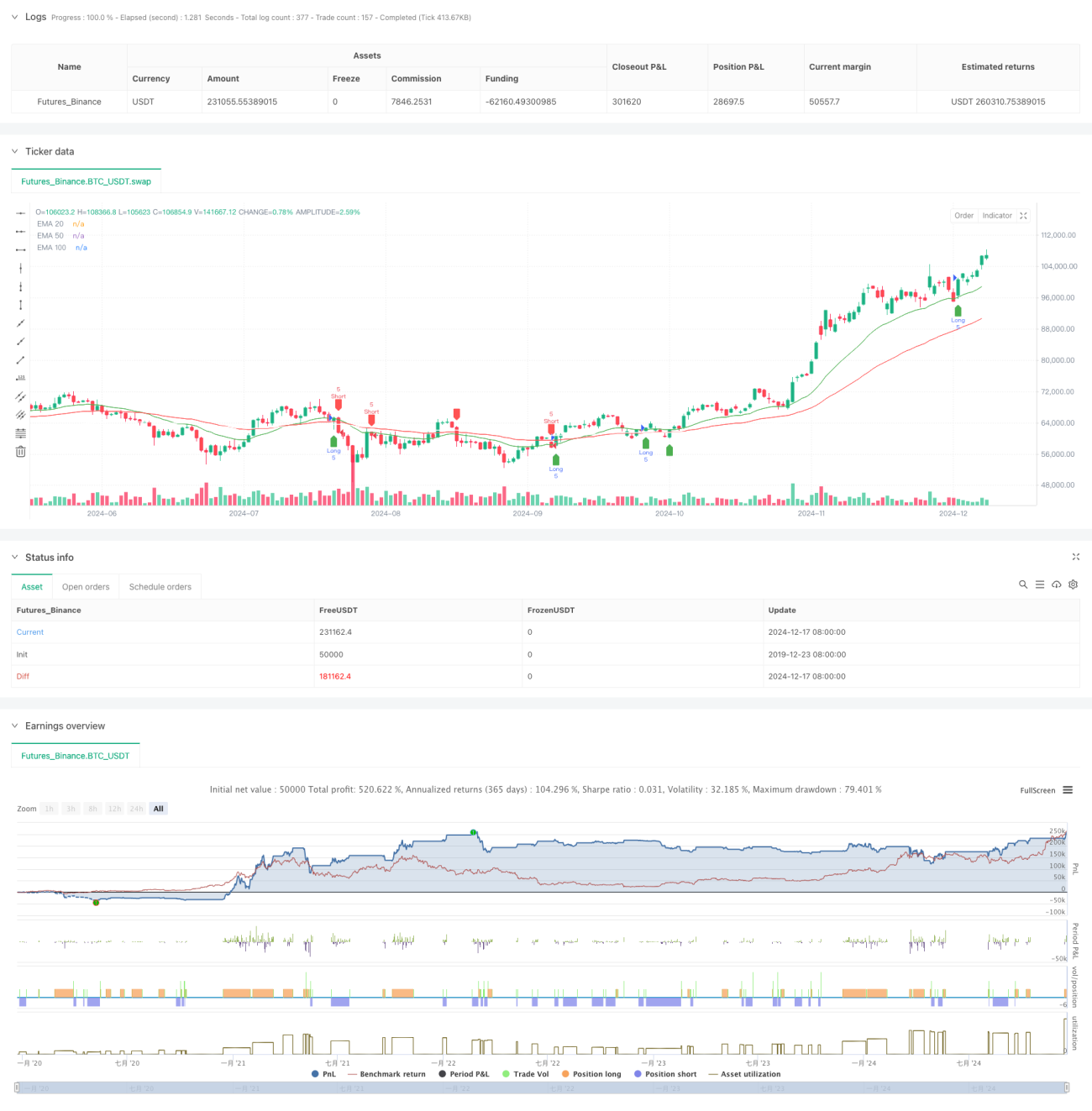

Die Strategie ist ein Trend-Tracking-Trading-System, basierend auf einem Multi-Index-Moving Average (EMA) und einer realen Bandbreite (ATR). Die Strategie erfasst die Markttrends durch die synchronisierte Kombination von drei EMAs mit 20-, 50- und 100-Zyklen und nutzt ATR für die dynamische Risikomanagement und die Ertragszielstellung. Diese Methode gewährleistet sowohl die Systematik des Handels als auch die dynamische Kontrolle des Risikos.

Strategieprinzip

Die Kernlogik der Strategie basiert auf der Wechselbeziehung zwischen dem Preis und mehreren EMAs.

- Eintrittssignale basieren auf der Kreuzung des Preises mit einem 20-Zyklus-EMA, wobei ein 50-Zyklus-EMA als Trendfilter verwendet wird

- Mehrfache Einstiegsvoraussetzungen: Der Preis trägt eine 20-Zyklus-EMA und liegt über einer 50-Zyklus-EMA

- Eintrittsvoraussetzungen: Preis unterhalb der 20-Zyklus-EMA und unterhalb der 50-Zyklus-EMA

- Stop-Loss-Einstellungen: basierend auf der dynamischen Berechnung des 14-Zyklus-ATR, um sicherzustellen, dass die Stop-Loss-Punkte an Marktschwankungen angepasst werden können

- Gewinnziel: mit einem Risiko-Gewinn-Verhältnis von 1,5x, d.h. mit einem Gewinnziel, das 1,5x die Stop-Loss-Distanz beträgt

Strategische Vorteile

- Mehrfache Zeitzyklus-Verifizierung: Effektive Verringerung von Falschsignalen durch Kombination von 20/50/100 Triple EMAs

- Dynamisches Risikomanagement: ATR-basierte Stop-Loss-Einstellungen, die Risikokontrollen marktgerechter gestalten

- Definitive RPV: Fixed RPV von 1,5 Mal, was zu langfristigen, stabilen Erträgen führt

- Trend-Tracking kombiniert mit Schwingungskontrolle: Beide können große Trends erfassen, ohne kurzfristige Chancen zu verpassen

- Visualisierte Handelssignale: Strategien bieten eine klare grafische Oberfläche, die von Händlern leicht verstanden und ausgeführt werden kann

Strategisches Risiko

- Risiken von Marktschocks: Häufige Falschbrüche während der Quer-Strecken-Phase

- Gleitrisiko: Bei schnellen Marktschwankungen kann der tatsächliche Kaufpreis von dem Signalpreis abweichen

- Trendwechselrisiko: Ein plötzlicher Trendwechsel in einem starken Trend kann zu größeren Verlusten führen

- Risiko der Parameteroptimierung: Eine Überoptimierung kann dazu führen, dass die Strategie im realen Handel schlechte Ergebnisse erzielt.

Richtung der Strategieoptimierung

- Einführung von Umsatzindikatoren: Effektivität von Preisbrüchen durch Umsatz

- Hinzufügen von Trendstärkefiltern: Erwägen Sie die Einführung von Trendstärkeindikatoren wie ADX, um die Einstiegsqualität zu verbessern

- Optimierung der Stop-Loss-Methode: Ein Tracking-Stop kann in Betracht gezogen werden, um die Gewinne besser zu sichern

- Klassifizierung der Marktumgebung: Anpassung der Strategieparameter an die unterschiedlichen Marktumgebungen

- Einführung von Volatilitätsfiltern: Aussetzung des Handels bei übermäßig schwankenden Marktumständen

Zusammenfassen

Durch die Kombination von Multiple Equilibrium-System und ATR Dynamic Wind Control erstellt die Strategie ein Trading-System mit Trend-Tracking und Bandbreiten-Betrieb. Die Strategie hat den Vorteil, dass sie systematisch und risikokontrollierbar ist. In der praktischen Anwendung muss jedoch auf die Anpassung an die Marktumgebung geachtet und entsprechend den tatsächlichen Umständen gezielt optimiert werden. Mit vernünftigen Parametersätzen und strenger Risikokontrolle wird die Strategie in den meisten Marktumgebungen zu stabilen Handelsergebnissen führen.

- 1