Adaptive dynamische Handelsstrategie basierend auf standardisierten logarithmischen Renditen

Überblick

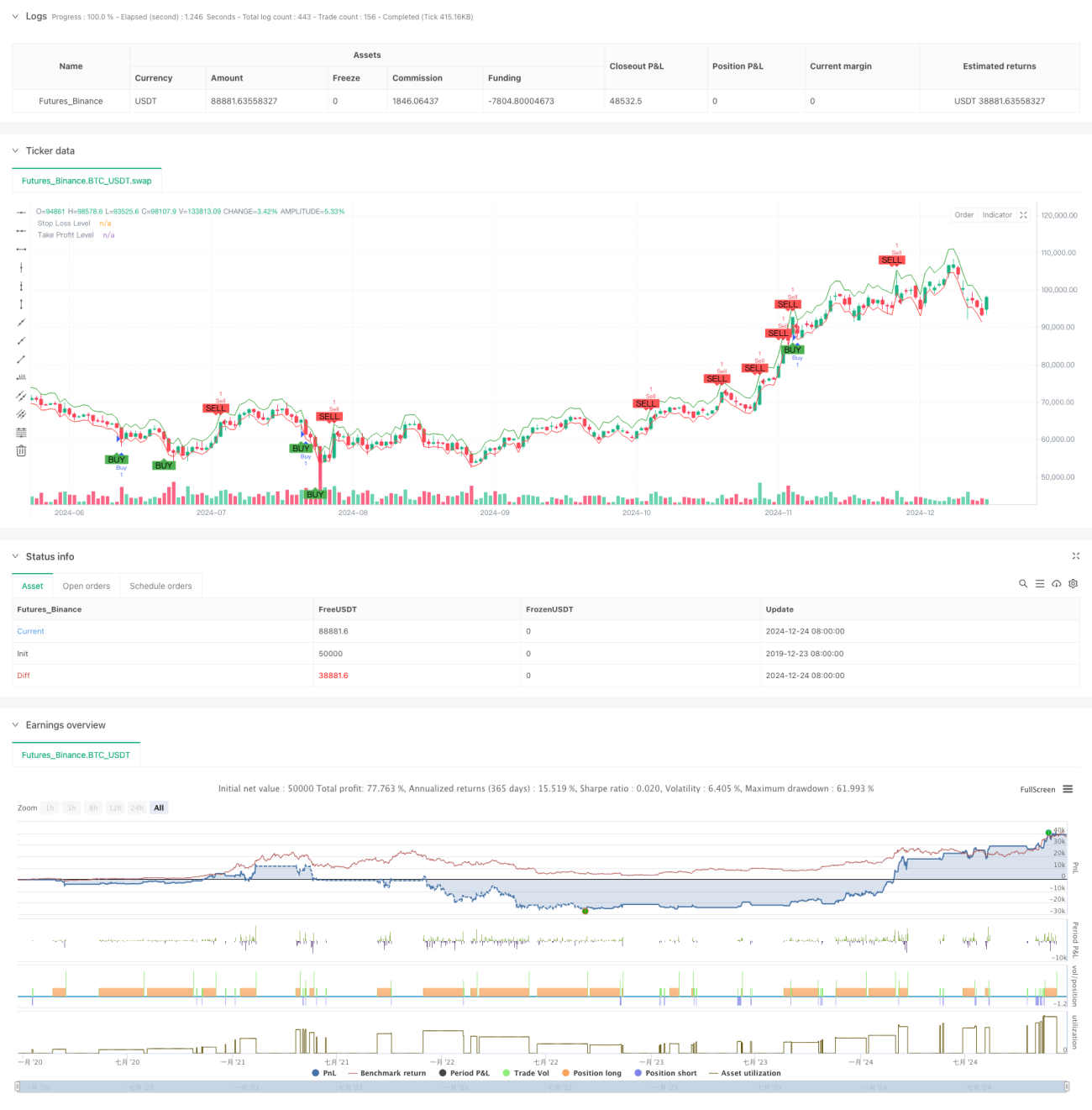

Diese Strategie ist ein adaptives Handelssystem, das auf dem Shiryaev-Zhou-Index (SZI) basiert. Es identifiziert überkaufte und überverkaufte Marktzustände, indem es den standardisierten Score der logarithmischen Renditen berechnet, und nutzt so Mean-Reversion-Chancen bei den Preisen. Die Strategie kombiniert dynamische Stop-Loss- und Take-Profit-Ziele für eine präzise Risikosteuerung.

Strategieprinzip

Der Kern der Strategie besteht darin, mit rollierenden statistischen Kennzahlen der logarithmischen Renditen einen standardisierten Indikator zu konstruieren. Die genauen Schritte sind:

- Berechnung der logarithmischen Renditen zur Normalisierung der Renditen.

- Verwendung eines 50-Perioden-Fensters zur Berechnung des rollierenden Mittelwerts und der Standardabweichung.

- Aufbau des SZI-Indikators: (logarithmische Rendite – rollierender Mittelwert) / rollierende Standardabweichung.

- Erzeugung eines Long-Signals, wenn SZI unter -2,0 fällt, und eines Short-Signals, wenn SZI über 2,0 steigt.

- Festlegung eines Stop-Loss von 2 % und eines Take-Profit von 4 %, basierend auf dem Einstiegspreis.

Strategievorteile

- Solide theoretische Basis: Beruht auf der Annahme einer logarithmischen Normalverteilung und bietet eine gute statistische Unterstützung.

- Hohe Anpassungsfähigkeit: Durch die Verwendung rollierender Fenster kann sich die Strategie an sich ändernde Marktvolatilitätsbedingungen anpassen.

- Umfassendes Risikomanagement: Verwendung eines prozentualen Stop-Loss, der eine präzise Risikokontrolle für jeden Trade ermöglicht.

- Benutzerfreundliche Visualisierung: Klare Markierung von Handelssignalen und Risikosteuerungsniveaus auf dem Chart.

Strategierisiken

- Parameterempfindlichkeit: Die Wahl der Fensterlänge und des Schwellenwerts hat erheblichen Einfluss auf die Strategieleistung.

- Abhängigkeit vom Marktumfeld: In Trendmärkten können häufige Fehlsignale auftreten.

- Slippage-Effekt: In Zeiten starker Marktbewegungen können die tatsächlichen Ausführungspreise erheblich vom Idealniveau abweichen.

- Rechenverzögerung: Die Echtzeitberechnung statistischer Indikatoren kann zu einer gewissen Signalverzögerung führen.

Optimierungsrichtungen

- Dynamische Schwellenwerte: Anpassung der Signalschwellenwerte basierend auf der Marktvolatilität.

- Multi-Timeframe: Einführung eines Signalbestätigungsmechanismus über mehrere Zeitrahmen.

- Volatilitätsfilter: Aussetzen des Handels oder Anpassung der Positionen bei extremen Volatilitäten.

- Signalbestätigung: Hinzufügen von Hilfsindikatoren wie Volumen und Momentum zur Signalbestätigung.

- Positionsmanagement: Implementierung eines dynamischen Positionsmanagements basierend auf der Volatilität.

Zusammenfassung

Dies ist eine quantitative Handelsstrategie mit einer soliden statistischen Grundlage, die über standardisierte logarithmische Renditen Preisbewegungschancen erfasst. Die Hauptvorteile der Strategie liegen in ihrer Anpassungsfähigkeit und der umfassenden Risikokontrolle, jedoch gibt es noch Optimierungspotenzial bei der Parameterauswahl und der Anpassung an das Marktumfeld. Durch die Einführung dynamischer Schwellenwerte und eines mehrdimensionalen Signalbestätigungsmechanismus lässt sich die Stabilität und Zuverlässigkeit der Strategie voraussichtlich weiter verbessern.

- 1