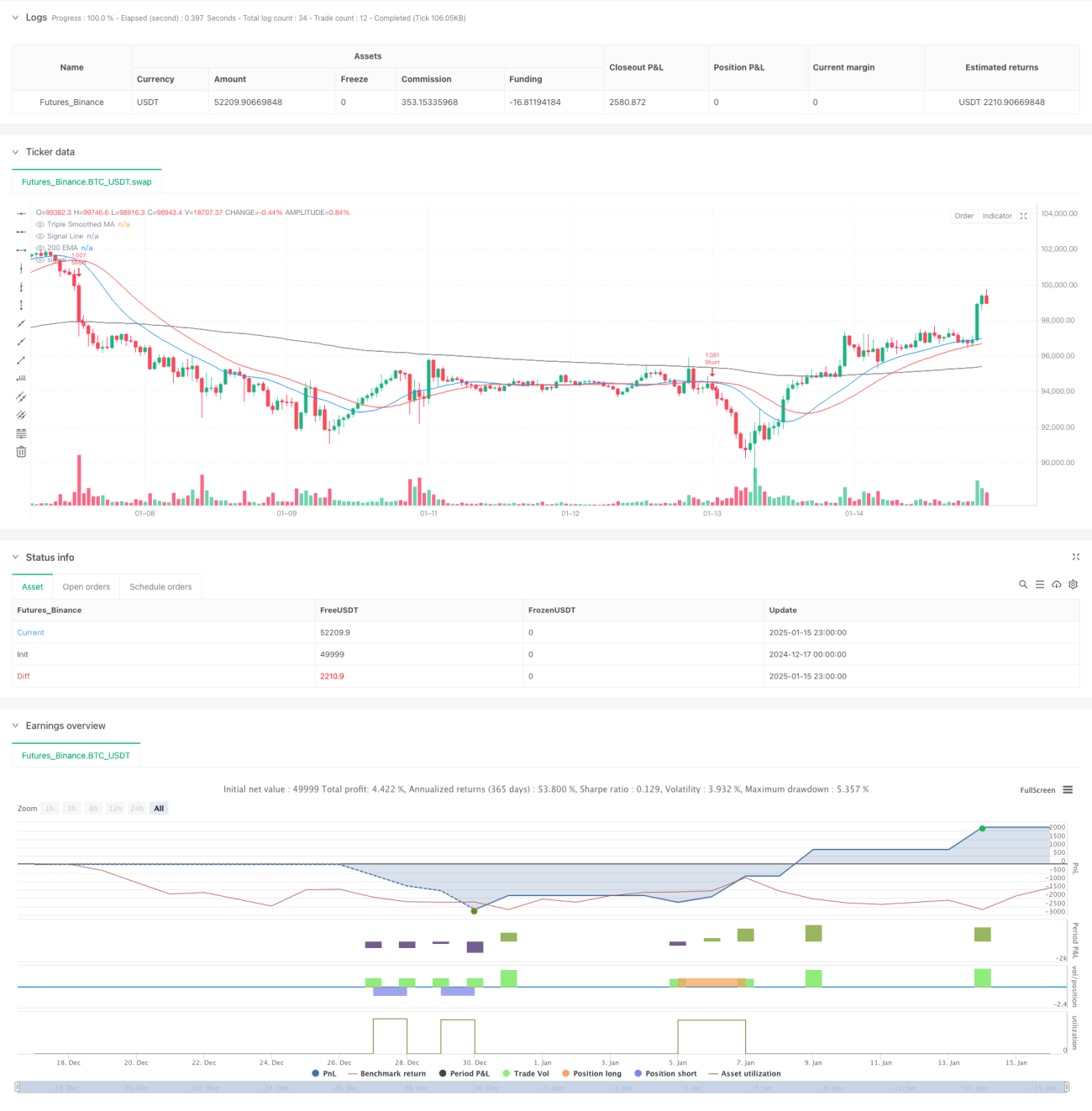

Übersicht

Diese Strategie ist ein Trendfolgesystem, das auf mehrfach geglätteten gleitenden Durchschnitten basiert. Durch eine dreifache Glättung wird Marktrauschen gefiltert, während gleichzeitig der RSI-Momentum-Indikator, der ATR-Volatilitätsindikator und der 200-Perioden-EMA-Trendfilter zur Bestätigung von Handelssignalen eingesetzt werden. Die Strategie verwendet einen 1-Stunden-Zeitraum, der ein gutes Gleichgewicht zwischen Handelsfrequenz und Trendzuverlässigkeit bietet und mit dem institutionellen Handelsverhalten übereinstimmt.

Strategieprinzip

Der Kern der Strategie besteht darin, durch dreifache Glättung der Kurse eine Haupttrendlinie zu konstruieren und mit einer Signallinie kürzerer Periode zu kreuzen, um Handelssignale zu erzeugen. Ein Handelssignal wird nur dann ausgeführt, wenn die folgenden Bedingungen gleichzeitig erfüllt sind:

- Die Beziehung der Kursposition zum 200-EMA bestätigt die Haupttrendrichtung.

- Die Position des RSI-Indikators bestätigt den Impuls.

- Der ATR-Indikator bestätigt ausreichende Volatilität.

- Der Kreuzungspunkt der Signallinie mit der dreifach geglätteten Durchschnittslinie bestätigt den konkreten Einstiegspunkt.

Der Stop-Loss basiert auf einem dynamischen ATR, der Take-Profit wird auf das 2-fache des ATR gesetzt, um ein gutes Risiko-Ertrags-Verhältnis zu gewährleisten.

Strategievorteile

- Die dreifache Glättung reduziert Fehlsignale erheblich und erhöht die Zuverlässigkeit der Trendbestimmung.

- Mehrere Bestätigungsmechanismen stellen sicher, dass die Handelsrichtung mit dem Haupttrend übereinstimmt.

- Dynamische Stop-Loss- und Take-Profit-Einstellungen passen sich unterschiedlichen Marktvolatilitätsumgebungen an.

- Die Strategie läuft im 1-Stunden-Zeitraum und vermeidet effektiv Seitwärtsbewegungen in niedrigeren Zeiträumen.

- Die Eigenschaft des Nicht-Nachzeichnens gewährleistet die Zuverlässigkeit der Backtest-Ergebnisse.

Strategierisiken

- In Seitwärtsmärkten können aufeinanderfolgende kleine Verluste auftreten.

- Mehrere Bestätigungsmechanismen können dazu führen, dass einige Handelsmöglichkeiten verpasst werden.

- Die Signalverzögerung kann die Optimierung des Einstiegspunkts beeinträchtigen.

- Es ist ausreichende Volatilität erforderlich, um gültige Signale zu erzeugen.

- In extremen Marktumgebungen kann der dynamische Stop-Loss möglicherweise nicht rechtzeitig sein.

Optimierungsrichtungen

- Die Einbeziehung des Volumenindikators als zusätzliche Bestätigung ist möglich.

- Die Einführung eines adaptiven Parameteroptimierungsmechanismus kann in Betracht gezogen werden.

- Eine quantitative Bewertung der Trendstärke kann hinzugefügt werden.

- Die Multiplikatoreinstellungen für Stop-Loss und Take-Profit können optimiert werden.

- Die Aufnahme eines Oszillatorindikators zur Verbesserung der Leistung in Seitwärtsmärkten kann erwogen werden.

Zusammenfassung

Dies ist eine strukturell vollständige und logisch rigorose Trendfolgestrategie. Durch die mehrfache Glättung und mehrere Bestätigungsmechanismen wird die Zuverlässigkeit der Handelssignale effektiv verbessert. Das dynamische Risikomanagement verleiht ihr eine gute Anpassungsfähigkeit. Obwohl eine gewisse Verzögerung besteht, bietet die Strategie durch Parameteroptimierung und Hinzufügung ergänzender Indikatoren noch erhebliches Verbesserungspotenzial.

/*backtest

start: 2024-12-17 00:00:00

end: 2025-01-16 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=6

strategy("Optimized Triple Smoothed MA Crossover Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=200)

// === Input Settings ===- 1