Erweiterte Multi-Indikator Trendbestätigungs-Handelsstrategie

Überblick

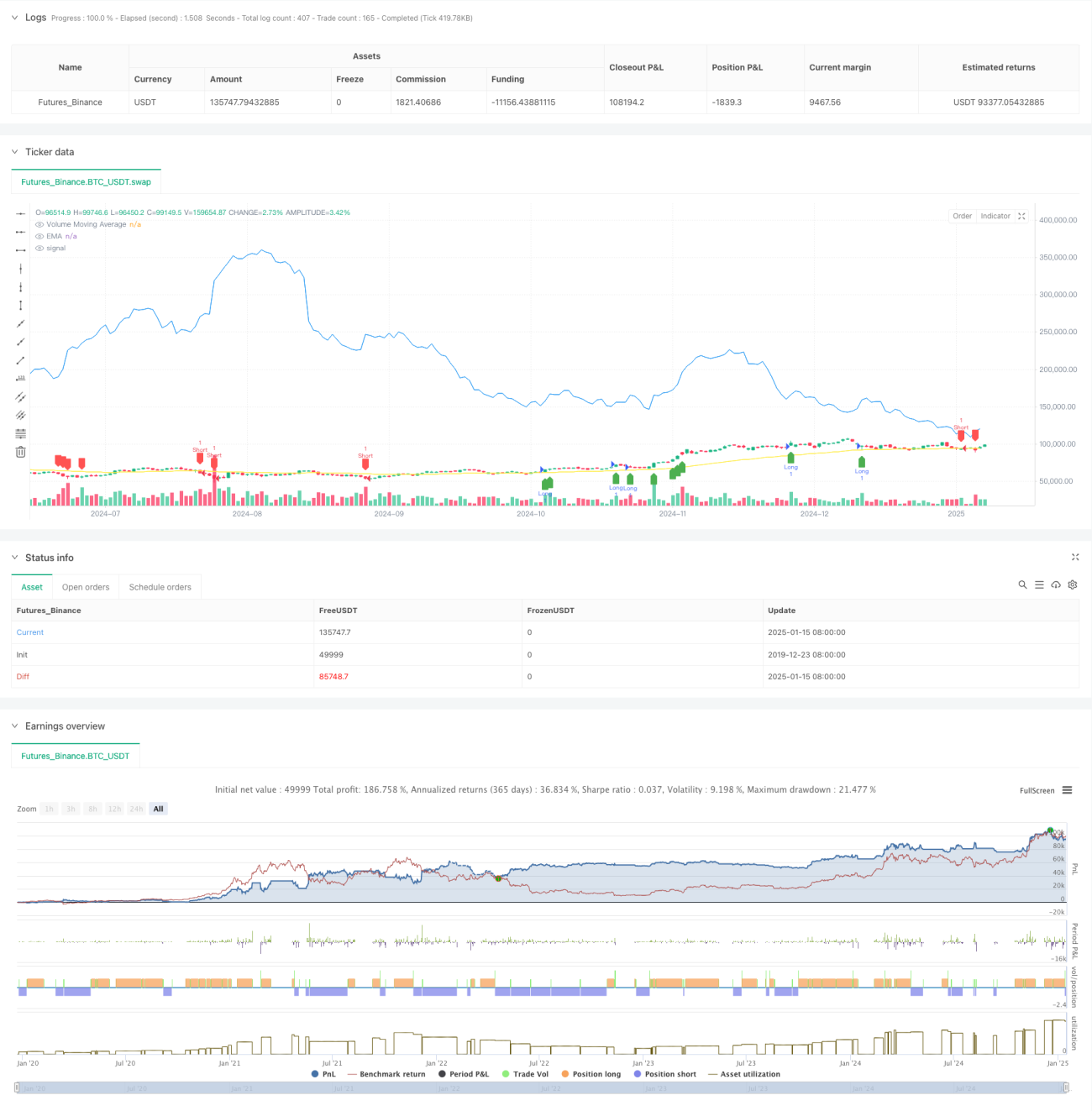

Diese Strategie ist eine fortschrittliche quantitative Handelsstrategie, die exponentielle gleitende Mittelwerte (EMA), Volumenbestätigung und Volatilitätsindikatoren (ATR) kombiniert. Durch die gleichzeitige Verwendung mehrerer technischer Indikatoren kann sie nicht nur Markttrends präzise erfassen, sondern auch die Zuverlässigkeit von Handelssignalen durch Volumenbestätigung erhöhen. Gleichzeitig nutzt sie den ATR zur dynamischen Anpassung von Stop-Loss und Take-Profit, um ein umfassendes Risikomanagementsystem zu schaffen.

Strategieprinzip

Die Kernlogik der Strategie besteht aus drei Hauptteilen:

- Trendbestimmung: Der EMA(50) dient als Hauptindikator für die Trendbestimmung. Liegt der Kurs oberhalb des EMA, wird ein Aufwärtstrend angenommen, andernfalls ein Abwärtstrend.

- Volumenbestätigung: Über die Berechnung des gleitenden Volumendurchschnitts (Volume MA) über 20 Perioden wird gefordert, dass das aktuelle Volumen nicht nur das 1,5-Fache des gleitenden Durchschnitts, sondern auch das Volumen der Vorperiode übersteigt, um eine ausreichende Marktbeteiligung sicherzustellen.

- Risikomanagement: Basierend auf dem 14-Perioden-ATR werden Stop-Loss und Take-Profit dynamisch festgelegt. Der Stop-Loss beträgt das 2-Fache des ATR, der Take-Profit das 3-Fache des ATR. Diese Einstellung schützt das Kapital und gibt dem Trend ausreichend Raum zur Entfaltung.

Vorteile der Strategie

- Mehrfachbestätigungsmechanismus: Durch die doppelte Bestätigung von Trend und Volumen wird die Zuverlässigkeit der Handelssignale erheblich erhöht.

- Dynamisches Risikomanagement: Die Verwendung des ATR für dynamische Stop-Loss- und Take-Profit-Einstellungen ermöglicht eine bessere Anpassung an Veränderungen der Marktvolatilität.

- Hohe Flexibilität: Die Strategieparameter können an verschiedene Marktbedingungen angepasst werden, was eine hohe Anpassungsfähigkeit gewährleistet.

- Klar visualisiert: Die Strategie bietet übersichtliche grafische Signalanzeigen, die dem Händler eine intuitive Beurteilung ermöglichen.

Risiken der Strategie

- Trendumkehrrisiko: Bei starken Marktschwankungen kann der EMA eine verzögerte Reaktion zeigen, was zu verspäteten Signalen führt.

- Falscher Volumenausbruch: Unter bestimmten Marktbedingungen kann ein hohes Volumen auf einen falschen Ausbruch hindeuten.

- Stop-Loss-Spanne: In manchen Fällen kann der Stop-Loss von 2 ATR zu groß sein und eine Anpassung erfordern.

Optimierungsmöglichkeiten

- Einführung eines Trendstärkeindikators: Die Hinzunahme von Indikatoren wie ADX könnte die Genauigkeit der Trendbestimmung weiter verbessern.

- Optimierung der Volumenfilterung: Komplexere Volumenanalysemethoden wie OBV oder volumengewichtete gleitende Mittelwerte könnten integriert werden.

- Verbesserung des Stop-Loss-Mechanismus: Nachlaufende Stop-Loss oder auf Unterstützungs-/Widerstandsniveaus basierende Stops könnten hinzugefügt werden.

- Zeitfilter hinzufügen: Die Einführung eines Handelszeitfilters könnte falsche Signale in Phasen geringer Marktaktivität vermeiden.

Zusammenfassung

Die Strategie baut durch die kombinierte Nutzung mehrerer technischer Indikatoren ein logisch strenges Handelssystem auf. Ihr Kernvorteil liegt im mehrfachen Bestätigungsmechanismus und im dynamischen Risikomanagement, jedoch sind Risiken wie Trendumkehr und falsche Volumenausbrüche zu beachten. Durch kontinuierliche Optimierung und Verbesserung kann die Strategie im realen Handel bessere Ergebnisse erzielen.

- 1