Übersicht

Dies ist eine flexible Handelsstrategie, die auf dem Keltner-Kanal basiert. Die Strategie unterstützt sowohl Long- als auch Short-Positionen und handelt, indem sie Ausbrüche des Preises über die obere oder untere Kanallinie überwacht. Der Kern der Strategie besteht darin, einen Preiskurskanal mithilfe eines gleitenden Durchschnitts (MA) zu konstruieren und die Kanalbreite dynamisch anhand der wahren Schwankungsbreite (ATR) anzupassen, um die Anpassungsfähigkeit der Strategie in verschiedenen Marktumgebungen zu gewährleisten.

Strategieprinzip

Die Strategie basiert hauptsächlich auf den folgenden Kernprinzipien:

- Berechnung des zentralen Trends des Kurses mittels EMA oder SMA zur Bildung der Mittellinie des Kanals.

- Verwendung von ATR, TR oder Range zur Berechnung der Volatilität und Konstruktion der oberen und unteren Kanallinien.

- Auslösen eines Long-Signals bei einem Ausbruch über die obere Linie und eines Short-Signals bei einem Ausbruch unter die untere Linie.

- Verwendung von Stop-Loss-Aufträgen für den Ein- und Ausstieg, um die Ausführungszuverlässigkeit zu erhöhen.

- Flexible Auswahl der Handelsmodi: nur Long, nur Short oder beide Richtungen.

Strategievorteile

- Hohe Anpassungsfähigkeit – Dynamische Anpassung der Kanalbreite durch ATR, sodass die Strategie an unterschiedliche Marktvolatilitätsumgebungen angepasst werden kann.

- Umfassendes Risikomanagement – Verwendung von Stop-Loss-Aufträgen zur effektiven Risikokontrolle.

- Flexible Bedienung – Unterstützt mehrere Handelsmodi, die je nach Markteigenschaften und Handelspräferenzen angepasst werden können.

- Validierte Wirksamkeit – Gute Performance in Kryptowährungs- und Aktienmärkten, insbesondere in volatileren Märkten.

- Klare Visualisierung – Anschauliche Darstellung von Handelssignalen und Positionsstatus.

Strategierisiken

- Seitwärtsmarktrisiko – In seitwärts tendierenden Märkten können häufige falsche Ausbruchssignale auftreten.

- Slippage-Risiko – In illiquiden Märkten können Stop-Loss-Aufträge mit erheblichen Slippagen verbunden sein.

- Trendumkehrrisiko – Bei plötzlichen Trendumkehrungen können größere Verluste entstehen.

- Parametersensitivität – Die Wahl der Kanalparameter hat einen erheblichen Einfluss auf die Performance der Strategie.

Optimierungsmöglichkeiten

- Einführung eines Trendfilters – Reduzierung falscher Ausbruchssignale durch Hinzufügen eines Trendindikators.

- Dynamische Parameteroptimierung – Dynamische Anpassung der Kanalparameter an die Marktvolatilität.

- Verbesserung des Stop-Loss-Mechanismus – Hinzufügen eines nachlaufenden Stopps zum besseren Schutz von Gewinnen.

- Volumenbestätigung – Kombination mit Volumenindikatoren zur Erhöhung der Signalkonfidenz.

- Optimierung des Positionsmanagements – Einführung eines dynamischen Positionsmanagements zur besseren Risikokontrolle.

Zusammenfassung

Diese Strategie ist ein gut durchdachtes und logisch klares Handelssystem. Durch den flexiblen Einsatz des Keltner-Kanals und verschiedener technischer Indikatoren werden Marktchancen effektiv erfasst. Die hohe Anpassbarkeit der Strategie macht sie für Händler mit unterschiedlichen Risikoprofilen geeignet. Durch kontinuierliche Optimierung und Verbesserung kann die Strategie voraussichtlich in verschiedenen Marktumgebungen stabile Ergebnisse erzielen.

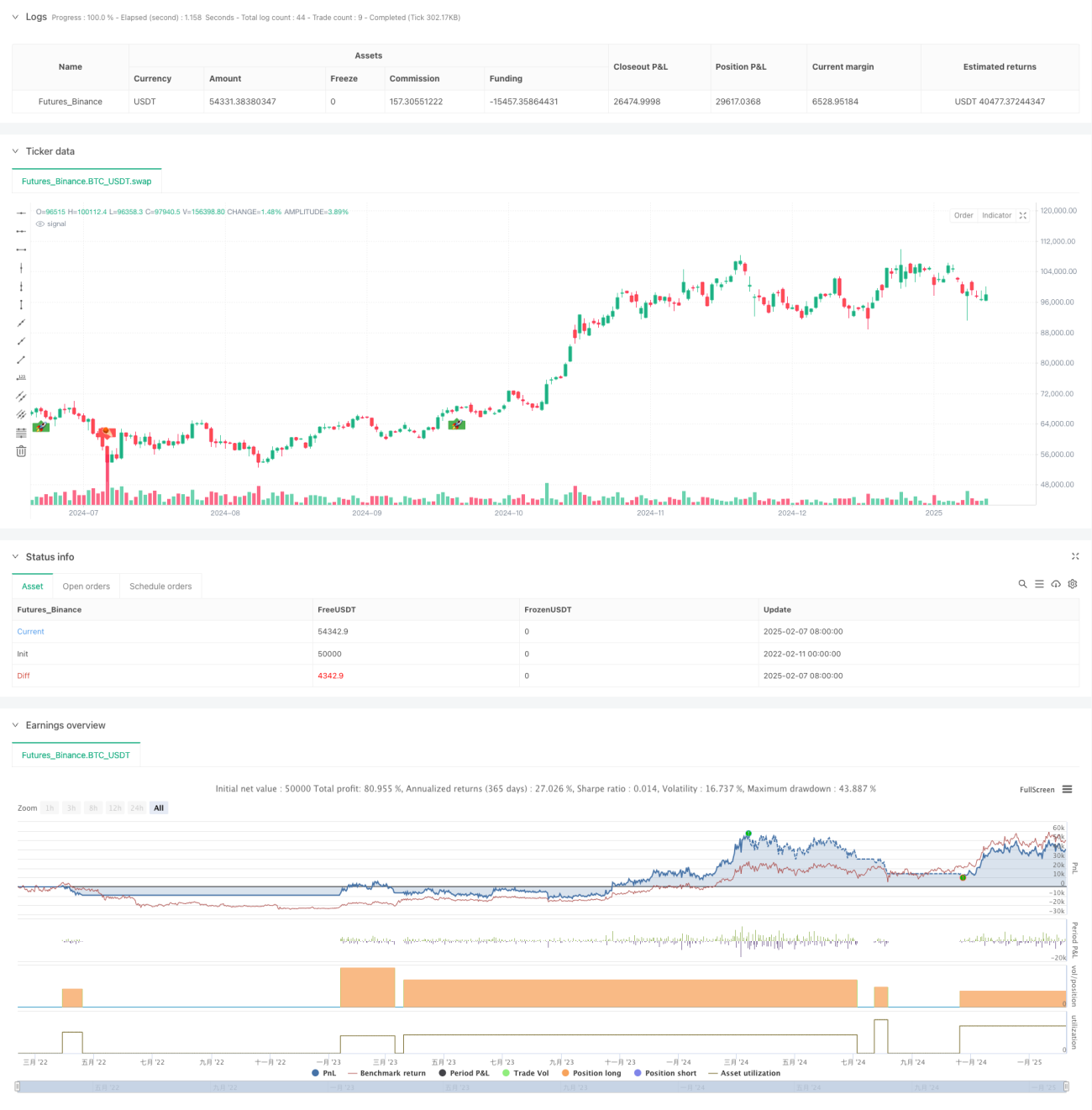

/*backtest

start: 2022-02-11 00:00:00

end: 2025-02-08 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy(title = "Jaakko's Keltner Strategy", overlay = true, initial_capital = 10000, default_qty_type = strategy.percent_of_equity, default_qty_value = 100)

// ──────────────────────────────────────────────────────────────────────────────- 1