Quantitative Handelsstrategie mit dynamischem Trailing-Stop-Loss basierend auf einem Drittel der Kerzenlinie

Übersicht

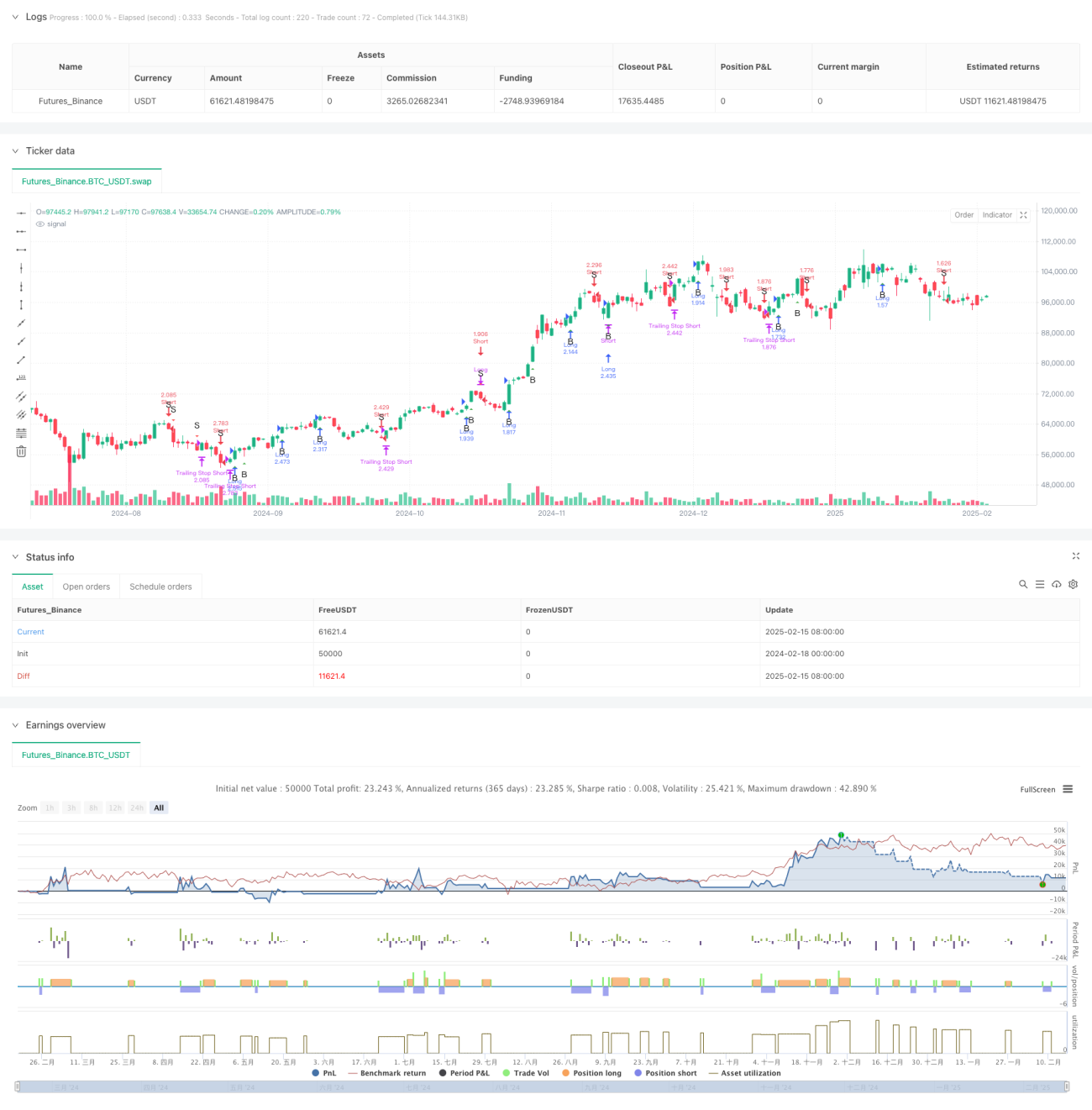

Dies ist eine quantitative Handelsstrategie, die die Drittel-Kerzenanalyse von Bill Williams mit einer dynamischen Trailing-Stop-Funktion kombiniert. Die Strategie analysiert die strukturellen Merkmale der aktuellen und der vorherigen Kerze, um klare Long-/Short-Signale zu generieren, und nutzt einen konfigurierbaren Trailing-Stop-Mechanismus, um Positionen zu schützen. Dies ermöglicht präzise Ein- und Ausstiege sowie ein effektives Risikomanagement.

Strategieprinzip

Die Kernlogik der Strategie basiert auf den folgenden Schlüsselkomponenten:

- Drittelung der Kerze: Die Spanne jeder Kerze (Hoch – Tief) wird in drei gleiche Teile geteilt, um die Grenzwerte der oberen und unteren Zone zu erhalten.

- Klassifizierung der Kerzenformen: Basierend auf der Position von Eröffnungs- und Schlusskurs innerhalb der drei Zonen werden die Kerzen in verschiedene Typen eingeteilt. Liegt der Eröffnungskurs in der unteren Zone und der Schlusskurs in der oberen Zone, gilt dies beispielsweise als starke Aufwärtsformation.

- Signalgenerierungsregeln: Durch die kombinierte Analyse der Formen der aktuellen und der vorherigen Kerze werden gültige Handelssignale ermittelt. Zeigen beispielsweise zwei aufeinanderfolgende Kerzen starke Merkmale, wird ein Long-Signal ausgelöst.

- Dynamischer Trailing-Stop: Innerhalb eines bestimmten Zeitraums wird der niedrigste Kurs der vorherigen N Kerzen (bei Long) bzw. der höchste Kurs (bei Short) als gleitender Stop-Level verwendet.

Strategievorteile

- Klare Logik: Die Strategie verwendet eine intuitive Methode zur Analyse der Kerzenstruktur, mit eindeutigen und leicht verständlichen Handelsregeln.

- Umfassendes Risikomanagement: Durch den dynamischen Trailing-Stop-Mechanismus kann das Verlustrisiko effektiv kontrolliert werden, während ausreichend Gewinnpotenzial erhalten bleibt.

- Hohe Anpassungsfähigkeit: Die Strategie kann die Trailing-Stop-Parameter an unterschiedliche Marktbedingungen anpassen und ist daher gut anpassbar.

- Hoher Automatisierungsgrad: Von der Signalerzeugung bis zum Positionsmanagement ist alles vollautomatisiert, wodurch menschliche Eingriffe reduziert werden.

Strategierisiken

- Risiko seitwärts tendierender Märkte: In Seitwärtsbewegungen können häufige Fehlsignale (Fakeouts) auftreten, die zu überhöhtem Handel führen.

- Gap-Risiko: Bei großen Kurslücken (Gaps) kann der Trailing-Stop möglicherweise nicht rechtzeitig ausgelöst werden, was zu unerwarteten Verlusten führt.

- Parameterempfindlichkeit: Die Wahl der Trailing-Stop-Parameter hat großen Einfluss auf die Strategieleistung. Ungünstige Einstellungen können zu vorzeitigem Ausstieg oder unzureichendem Schutz führen.

Optimierungsmöglichkeiten

- Hinzufügen eines Marktumgebungsfilters: Trendindikatoren oder Volatilitätsindikatoren können eingeführt werden, um die Strategieparameter dynamisch an verschiedene Marktbedingungen anzupassen.

- Optimierung des Stopp-Mechanismus: Die Kombination mit dem ATR-Indikator ermöglicht flexiblere Stop-Abstände und verbessert die Anpassungsfähigkeit des Stopps.

- Einführung eines Positionsmanagements: Die Positionsgröße kann dynamisch an die Signalstärke und die Marktvolatilität angepasst werden, um eine feinere Risikokontrolle zu erreichen.

- Verbesserung des Ausstiegs: Gewinnziele oder zusätzliche technische Indikatoren können hinzugefügt werden, um den Ausstiegszeitpunkt zu optimieren.

Zusammenfassung

Dies ist eine strukturell vollständige und logisch klare quantitative Handelsstrategie, die klassische technische Analysemethoden mit modernen Risikomanagementtechniken kombiniert und eine hohe Praxistauglichkeit aufweist. Das Design der Strategie berücksichtigt die Anforderungen des Live-Handels, einschließlich Signalgenerierung, Positionsmanagement und Risikokontrolle. Durch weitere Optimierung und Verfeinerung kann diese Strategie im praktischen Handel bessere Ergebnisse erzielen.

/*backtest

start: 2024-02-18 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("TrinityBar with Trailing Stop", overlay=true, initial_capital=100000,

default_qty_type=strategy.percent_of_equity, default_qty_value=250)

- 1