Dynamischer Volumen-gleitender Durchschnitt Trendfolge und HLCC4-Ausbruch-Handelsstrategie

Überblick

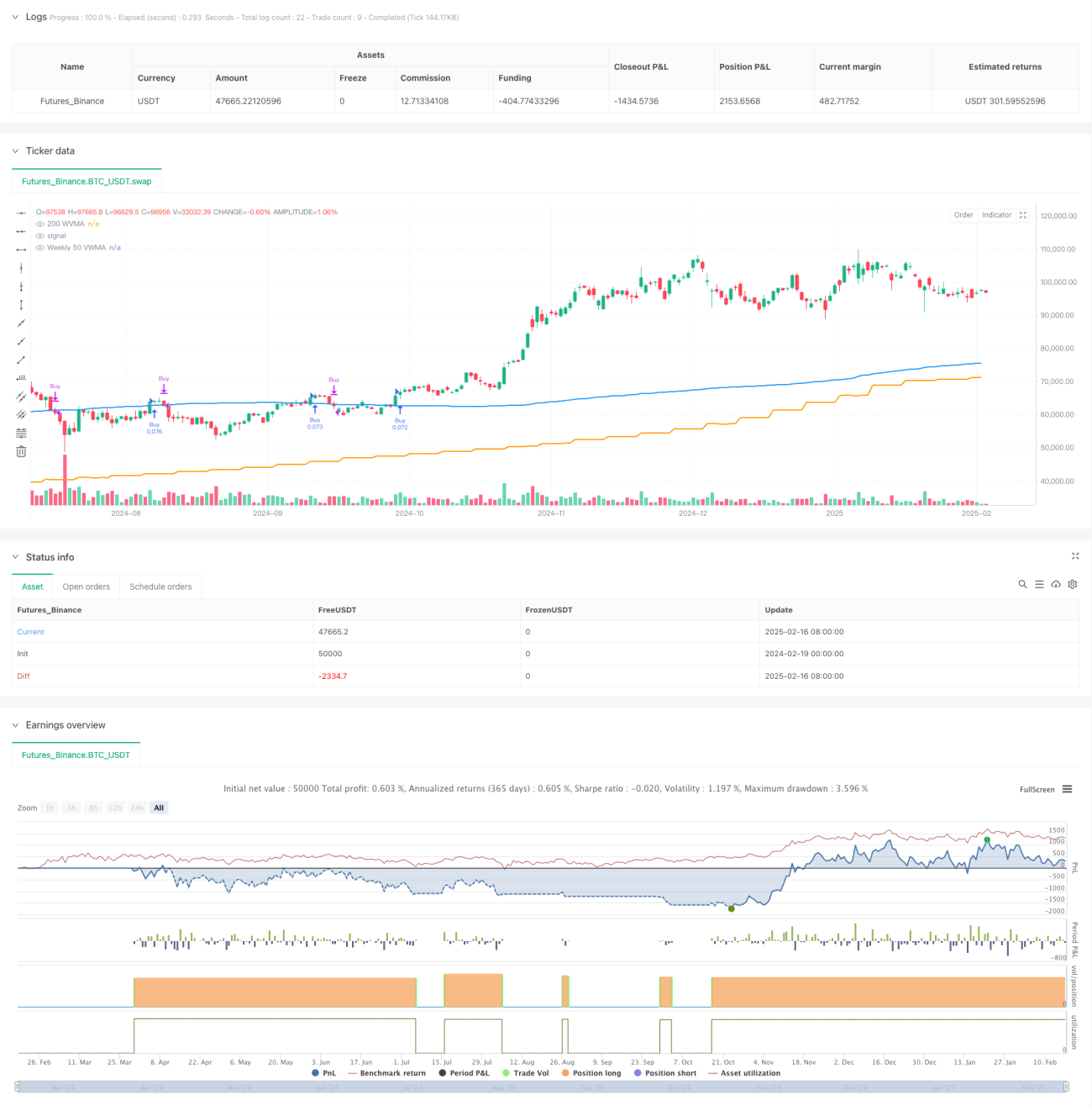

Die Strategie ist ein auf multiplen Zeiträumen basierendes Trendfolgesystem. Sie nutzt den 50-Perioden Volume-Weighted Moving Average (VWMA) im Wochenchart als groben Trendfilter und verwendet den 200-Perioden VWMA des aktuellen Zeitrahmens sowie den HLCC4-Kursdurchbruch als konkrete Handelssignale. Es handelt sich um eine reine Long-Strategie, die durch strenge Trendbestätigung und Überprüfung über mehrere Zeiträume die Zuverlässigkeit der Trades erhöht.

Strategieprinzip

Die Kernlogik der Strategie umfasst die folgenden Schlüsselelemente:

- Der 50-Perioden VWMA im Wochenchart dient als Maßstab für den übergeordneten Trend: Eine Position wird nur eröffnet, wenn der Kurs über diesem gleitenden Durchschnitt liegt.

- Die Einstiegsbedingung erfordert, dass die Schlusskurse von zwei aufeinanderfolgenden Kerzen über dem 200-Perioden VWMA liegen und der Schlusskurs der zweiten Kerze höher ist als der HLCC4-Durchschnittskurs der ersten Kerze.

- Das Ausstiegssignal basiert auf dem Tageschart: Eine Position wird geschlossen, wenn der Tagesschlusskurs unter den 200-Perioden VWMA des Tagescharts fällt.

- Die Strategie verwendet ein festes Positionsgrößenmanagement: Pro Trade werden 10 % des Kontokapitals eingesetzt.

- Der Backtest-Zeitraum ist auf die letzten 5 Jahre begrenzt, um die Wirksamkeit der Strategie unter aktuellen Marktbedingungen sicherzustellen.

Strategievorteile

- Überprüfung über mehrere Zeiträume: Durch die Kombination von Wochen- und Tageschart werden sowohl der große Trend erfasst als auch zeitnah auf Marktveränderungen reagiert.

- Umfassendes Risikomanagement: Die Verwendung des VWMA anstelle eines einfachen gleitenden Durchschnitts spiegelt die tatsächliche Marktentwicklung besser wider.

- Strenge Trendbestätigung: Mehrere Bedingungen müssen gleichzeitig erfüllt sein, bevor ein Einstieg erfolgt, wodurch das Risiko von Fehlausbrüchen reduziert wird.

- Angemessenes Positionsgrößenmanagement: Die feste Positionsgröße kontrolliert das Risiko und erhält gleichzeitig Ertragspotenzial.

- Hoher Automatisierungsgrad: Die Strategielogik ist klar und kann vollständig automatisiert gehandelt werden.

Strategierisiken

- Trendumkehrrisiko: Bei starken Marktschwankungen können größere Verluste auftreten.

- Slippage-Einfluss: Bei geringer Marktliquidität kann der tatsächliche Handelskurs vom theoretischen Kurs abweichen.

- Signalverzögerung: Aufgrund der Verwendung längerer Durchschnittsperioden kann die Reaktion der Strategie auf Trendwenden relativ verzögert sein.

- Fehlausbruchsrisiko: Trotz mehrfacher Bestätigung können dennoch Verluste durch Fehlausbrüche auftreten.

- Beschränkung auf Long-Trades: Die Strategie handelt nur Long und verpasst in Abwärtstrends potenzielle Short-Gelegenheiten.

Optimierungsmöglichkeiten der Strategie

- Dynamische Parameteroptimierung: Die Periodenparameter des VWMA könnten automatisch an die Marktvolatilität angepasst werden.

- Optimierung des Positionsgrößenmanagements: Einführung eines dynamischen Positionsgrößenmanagements auf Basis der Volatilität.

- Verbesserung des Ausstiegsmechanismus: Hinzufügen eines Trailing-Stops oder eines dynamischen Stops basierend auf technischen Indikatoren.

- Einbindung von Marktstimmungsindikatoren: Kombination mit Indikatoren wie RSI oder MACD zur Erhöhung der Signalzuverlässigkeit.

- Einführung der Volumenanalyse: Vertiefung der Volumenanalyse und Optimierung der Berechnungsmethode des VWMA.

Zusammenfassung

Es handelt sich um eine sorgfältig konzipierte Trendfolgestrategie, die durch die Kombination mehrerer Zeiträume und strenge Handelsbedingungen eine gute Risikokontrolle erreicht. Der Hauptvorteil der Strategie liegt in ihrem soliden Trendbestätigungsmechanismus und ihrer klaren Handelslogik, die sich eignet, um in starken Märkten mittel- bis langfristige Trendchancen zu nutzen. Durch die vorgeschlagenen Optimierungsrichtungen besteht weiteres Verbesserungspotenzial.

/*backtest

start: 2024-02-19 00:00:00

end: 2025-02-17 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Long-Only 200 WVMA + HLCC4 Strategy (Weekly 50 VWMA Filter, Daily Exit, Last 5 Years)", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Parameters- 1