Handelsstrategie zur Trend-Erfassung basierend auf historischen Delta-SMA-Hochs und -Tiefs

Übersicht

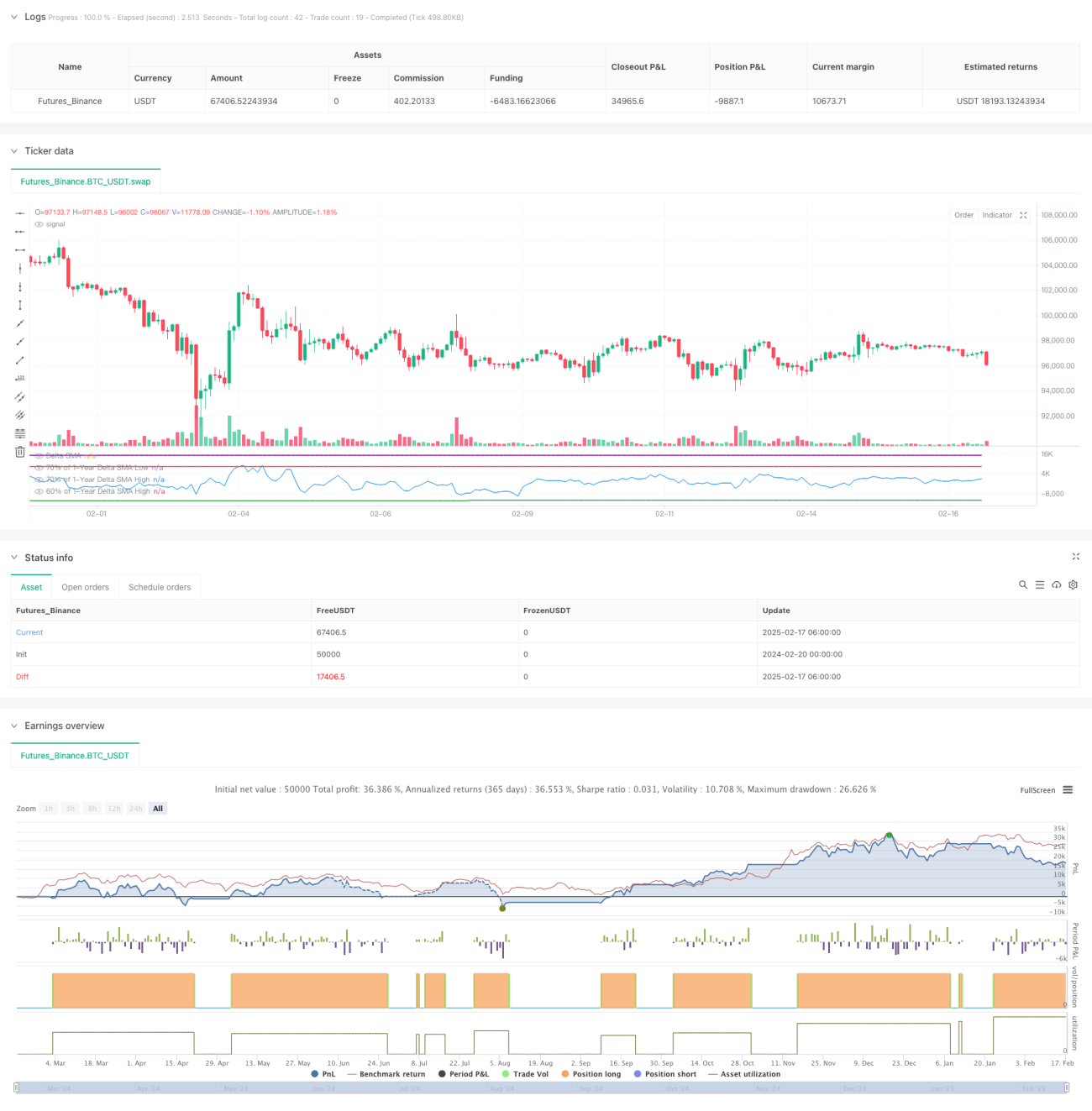

Diese Handelsstrategie basiert auf der Analyse von Hoch- und Tiefpunkten eines einfachen gleitenden Durchschnitts (SMA) des Handelsvolumen-Delta-Werts über einen Zeitraum von einem Jahr. Die Strategie berechnet den gleitenden Durchschnitt der Differenz zwischen Kauf- und Verkaufsvolumen und vergleicht diesen mit historischen Hoch- und Tiefpunktschwellen, um potenzielle Handelssignale zu identifizieren. Der Rückblickzeitraum ist lang, wodurch die Strategie für den mittel- bis langfristigen Trendhandel geeignet ist.

Funktionsweise der Strategie

Der Kern der Strategie basiert auf den folgenden wichtigen Schritten:

- Delta-Berechnung: Die Differenz zwischen Kauf- und Verkaufsvolumen wird durch die Analyse der Kursentwicklung ermittelt. Wenn der Schlusskurs über dem Eröffnungskurs liegt, wird das Volumen als Kaufvolumen erfasst, andernfalls als Verkaufsvolumen.

- SMA-Glättung: Der Delta-Wert wird mit einem gleitenden Durchschnitt über 14 Perioden geglättet, um Rauschen zu reduzieren.

- Bestimmung der Hoch- und Tiefpunkte über ein Jahr: Es werden der höchste und niedrigste Wert des Delta-SMA im letzten Jahr berechnet.

- Signalauslösungsbedingungen:

- Kaufsignal: Tritt ein, wenn der Delta-SMA, nachdem er 70 % unter dem Jahrestief lag, die Nulllinie nach oben durchbricht.

- Verkaufssignal: Tritt ein, wenn der Delta-SMA, nachdem er 90 % des Jahreshöchststandes überschritten hat, unter 60 % fällt.

Vorteile der Strategie

- Starke Erkennung langfristiger Trends: Durch die Analyse historischer Daten über ein Jahr hinweg können Haupttrends effektiv erfasst werden.

- Gute Rauschunterdrückung: Die Verwendung von SMA-Glättung und mehreren Schwellenbedingungen reduziert Fehlsignale wirksam.

- Angemessenes Risikomanagement: Klare Einstiegs- und Ausstiegsbedingungen verhindern übermäßigen Handel.

- Anpassungsfähigkeit: Die Parameter der Strategie können je nach Marktbedingungen angepasst werden.

Risiken der Strategie

- Verzögerungsrisiko: Aufgrund der Verwendung von SMA und langen Rückblickzeiträumen können Signale verzögert auftreten.

- Risiko falscher Ausbrüche: In Seitwärtsmärkten können Fehlsignale entstehen.

- Marktabhängigkeit: In Märkten ohne klaren Trend kann die Leistung nachlassen.

- Parameterempfindlichkeit: Die Schwellenwerte haben einen großen Einfluss auf die Strategieleistung.

Optimierungsansätze

- Dynamische Schwellenanpassung: Die Hoch- und Tiefpunktschwellen können je nach Marktvolatilität dynamisch angepasst werden.

- Zusätzliche Indikatoren: Kombination mit anderen technischen Indikatoren zur Erhöhung der Signalzuverlässigkeit.

- Einführung eines Stop-Loss-Mechanismus: Dynamische Stop-Losses zur Risikobegrenzung.

- Marktumfeld-Filter: Hinzufügen einer Logik zur Marktumfeldbewertung, um die Strategie nur in geeigneten Phasen zu aktivieren.

Zusammenfassung

Diese Strategie ist ein mittel- bis langfristiger Trendfolgeansatz, der auf Volumenanalyse basiert. Durch die Analyse historischer Hoch- und Tiefpunkte der Differenz zwischen Kauf- und Verkaufsvolumen werden Markttrends erfasst. Die Strategie ist sinnvoll aufgebaut und das Risikomanagement angemessen. Allerdings müssen die Anpassungsfähigkeit an das Marktumfeld und die Parameteroptimierung beachtet werden. Durch die vorgeschlagenen Optimierungsansätze besteht noch Potenzial für weitere Verbesserungen.

- 1