Multi-Indikator-Trend-Momentum-ATR-Zielpreis-Handelsstrategie

Übersicht

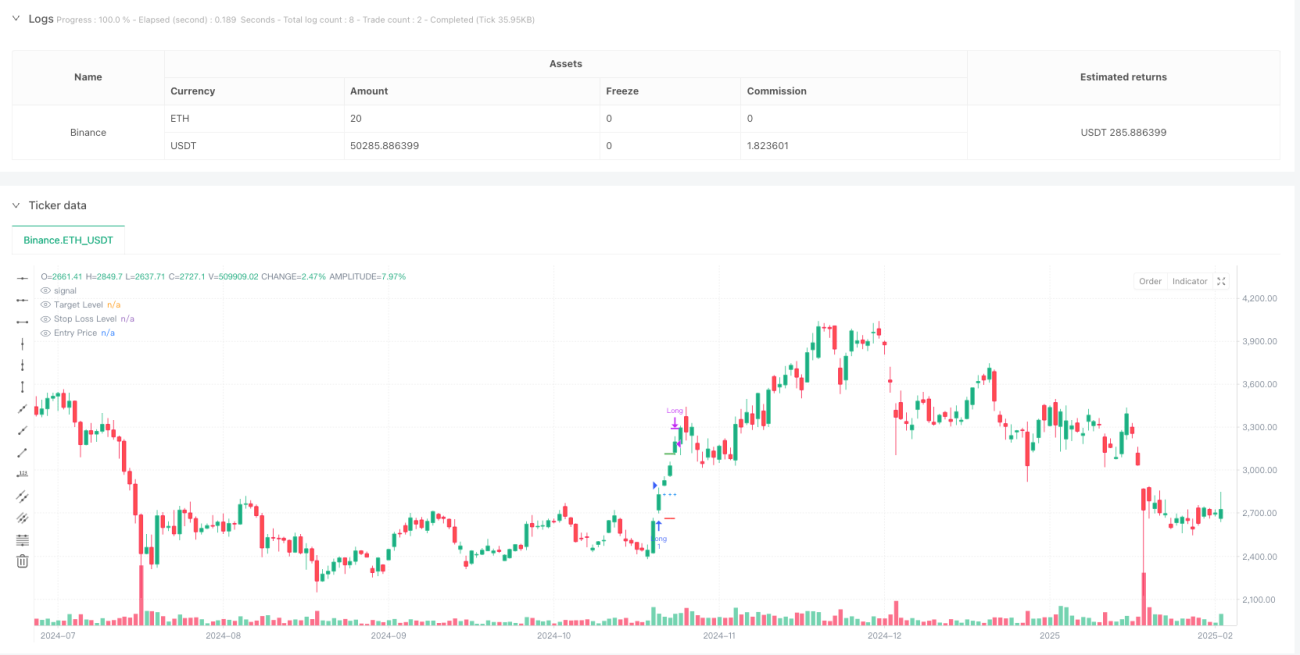

Diese Strategie ist ein Trendfolge- und Momentum-Handelssystem, das auf mehreren technischen Indikatoren basiert. Sie kombiniert hauptsächlich den Average Directional Index (ADX), den Relative-Stärke-Index (RSI) und die Average True Range (ATR), um potenzielle Long-Gelegenheiten zu identifizieren, und nutzt die ATR zur Festlegung dynamischer Gewinn- und Stopp-Loss-Niveaus. Die Strategie eignet sich besonders für den Optionshandel im 1-Minuten-Zeitraum und zielt darauf ab, die Erfolgsquote durch strenge Einstiegsbedingungen und Risikomanagement zu erhöhen.

Strategieprinzip

Die Kernlogik der Strategie umfasst die folgenden Schlüsselkomponenten:

- Trendbestätigung: Verwendung von ADX > 18 und +DI > -DI zur Bestätigung eines Aufwärtstrends.

- Momentum-Überprüfung: Anforderung, dass der RSI über 60 steigt und sich über seinem 20-Perioden-gleitenden Durchschnitt befindet, um das Preismomentum zu bestätigen.

- Einstiegszeitpunkt: Wenn sowohl die Trend- als auch die Momentum-Bedingungen erfüllt sind, wird zum aktuellen Schlusskurs eine Long-Position eröffnet.

- Zielmanagement: Festlegung dynamischer Gewinnziele (2,5-fache ATR) und Stopp-Loss-Niveaus (1,5-fache ATR) basierend auf dem ATR-Wert zum Zeitpunkt des Einstiegs.

Strategievorteile

- Mehrdimensionale Bestätigung: Durch die Kombination von Trend- und Momentum-Indikatoren werden zuverlässigere Handelssignale bereitgestellt.

- Dynamisches Risikomanagement: Verwendung der ATR zur dynamischen Anpassung von Take-Profit- und Stop-Loss-Positionen, um sich an die Marktvolatilität anzupassen.

- Klare Handelsregeln: Eindeutige Ein- und Ausstiegsbedingungen reduzieren Störungen durch subjektive Entscheidungen.

- Anpassungsfähigkeit: Die Strategieparameter können je nach Marktumgebung und Handelsinstrument optimiert werden.

Strategierisiken

- Fehlausbruchsrisiko: Ein RSI-Durchbruch über 60 kann Fehlsignale erzeugen und sollte mit anderen Indikatoren bestätigt werden.

- Slippage-Einfluss: In schnellen Märkten mit 1-Minuten-Zeitraum kann ein erhebliches Slippage-Risiko bestehen.

- Marktabhängigkeit: Die Strategie schneidet in trendstarken Märkten besser ab, während sie in Seitwärtsmärkten häufig Stopps auslösen kann.

- Parameterempfindlichkeit: Die Einstellungen der verschiedenen Indikatorparameter müssen ausgewogen sein; ungeeignete Parameterkombinationen können die Strategieleistung beeinträchtigen.

Optimierungsansätze für die Strategie

- Einstiegsoptimierung: Hinzufügen eines Volumenbestätigungsmechanismus zur Erhöhung der Signalgüte.

- Positionsmanagement: Einführung eines dynamischen Positionsverwaltungssystems, das die Positionsgröße an die Marktvolatilität anpasst.

- Ausstiegsmechanismus: Ergänzung einer Trailing-Stop-Funktion zum besseren Gewinnschutz.

- Zeitfilter: Hinzufügen eines Handelszeitfenster-Filters, um Phasen mit übermäßiger Volatilität oder geringer Liquidität zu vermeiden.

Zusammenfassung

Die Strategie baut durch die integrierte Nutzung mehrerer technischer Indikatoren ein vollständiges Handelssystem auf. Ihr Vorteil liegt in der Kombination von Trend- und Momentum-Analyse sowie einem dynamischen Risikomanagement-Ansatz. Trotz gewisser Risiken kann sie bei angemessener Parameteroptimierung und Risikokontrollmaßnahmen im realen Handel stabile Ergebnisse erzielen. Es wird empfohlen, die Strategie vor dem Live-Einsatz gründlich zu backtesten und zu optimieren sowie sie entsprechend den spezifischen Eigenschaften des gehandelten Instruments anzupassen.

- 1