Dynamische Multi-Zeitraum-Trendprognose mit Moving-Average-Filterstrategie

Überblick

Diese Strategie ist ein Trendfolgesystem, das traditionelle technische Analyse mit modernen Methoden der künstlichen Intelligenz kombiniert. Es verwendet hauptsächlich den exponentiellen gleitenden Durchschnitt (EMA) und den einfachen gleitenden Durchschnitt (SMA) als Trendfilter und führt gleichzeitig ein Vorhersagemodell ein, um den Einstiegszeitpunkt zu optimieren. Die Strategie ist speziell für das Tagesintervall optimiert und zielt darauf ab, mittel- bis langfristige Markttrends zu erfassen.

Strategieprinzip

Die Kernlogik der Strategie besteht aus drei Hauptkomponenten:

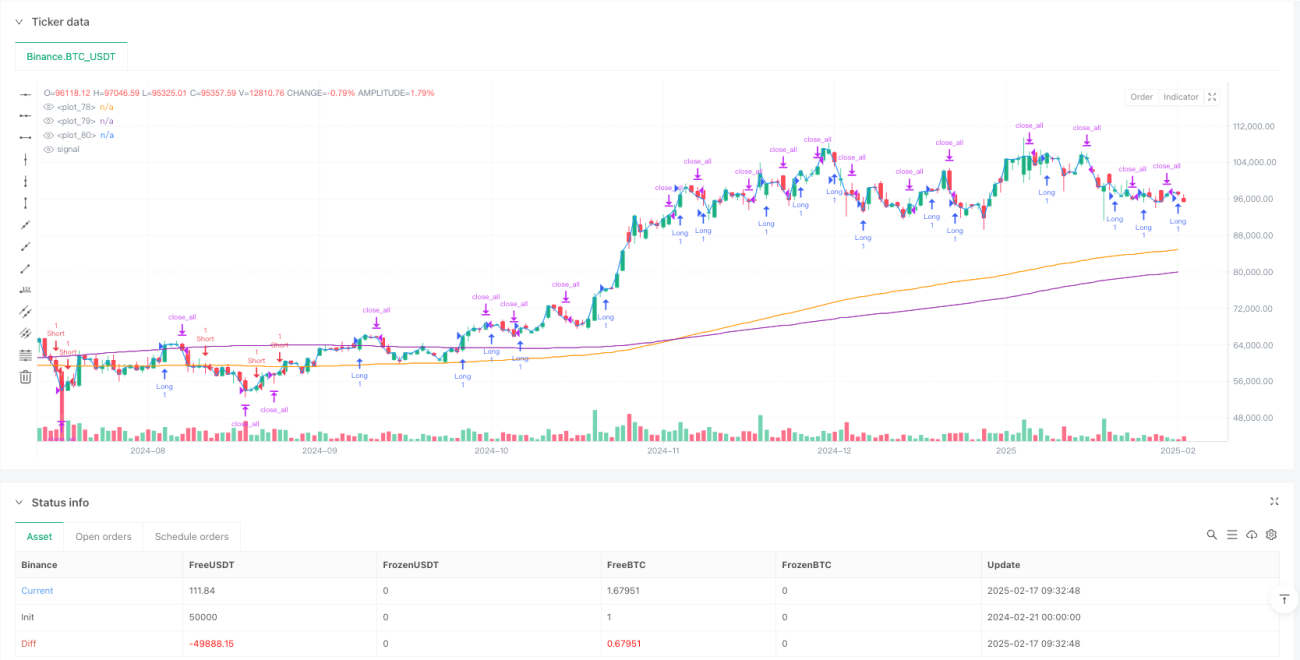

- Trendbewertungssystem – Verwendung eines 200-Perioden-EMA und SMA als primäre Trendfilter. Die aktuelle Trendrichtung wird anhand der Position des Kurses relativ zu den gleitenden Durchschnitten bestimmt.

- Vorhersagemodul – Implementierung eines erweiterbaren Vorhersagebausteins. Derzeit wird eine simulierte Vorhersage verwendet, die später durch ein maschinelles Lernmodell ersetzt werden kann.

- Positionsmanagement – Festlegung eines festen Haltezeitraums von 4 Kerzen, um die Haltedauer und das Risiko zu kontrollieren.

Die Erzeugung von Handelssignalen erfordert die Übereinstimmung von Trendrichtung und Vorhersagesignal:

- Long-Signal: Der Kurs liegt über EMA und SMA, und der Vorhersagewert ist positiv.

- Short-Signal: Der Kurs liegt unter EMA und SMA, und der Vorhersagewert ist negativ.

Strategievorteile

- Klare Struktur – Die Logik der Strategie ist einfach und intuitiv, leicht zu verstehen und zu warten.

- Kontrolliertes Risiko – Durch einen festen Haltezeitraum und eine doppelte gleitende Durchschnittsfilterung wird das Risiko effektiv begrenzt.

- Hohe Erweiterbarkeit – Das Vorhersagemodul ist flexibel gestaltet und kann je nach Bedarf mit verschiedenen Vorhersagemodellen verbunden werden.

- Gute Anpassungsfähigkeit – Parameter können angepasst werden, um sich an verschiedene Marktbedingungen anzupassen.

- Angemessene Handelsfrequenz – Die Operation auf Tagesbasis reduziert die Transaktionskosten und den psychischen Druck.

Strategierisiken

- Trendumkehrrisiko – An Wendepunkten des Trends können Verluste in Folge auftreten.

- Parameterempfindlichkeit – Die Wahl der gleitenden Durchschnittsperiode und des Haltezeitraums hat erheblichen Einfluss auf die Strategieleistung.

- Modellabhängigkeit – Die Genauigkeit des Vorhersagemoduls beeinflusst direkt die Effektivität der Strategie.

- Slippage-Einfluss – Operationen auf Tagesbasis können mit größerem Slippage verbunden sein.

- Marktabhängigkeit – In Seitwärtsmärkten kann die Performance schlecht sein.

Optimierungsmöglichkeiten

- Vorhersagemodell-Upgrade – Einführung von maschinellem Lernen als Ersatz für die derzeitige Zufallsvorhersage.

- Dynamischer Haltezeitraum – Anpassung der Haltedauer an die Marktvolatilität.

- Stop-Loss-Optimierung – Hinzufügung eines dynamischen Stop-Loss-Mechanismus zur Verbesserung der Risikokontrolle.

- Positionsmanagement – Einführung eines auf der Volatilität basierenden Positionsmanagementsystems.

- Mehrdimensionale Filter – Hinzunahme von Hilfsindikatoren wie Volumen und Volatilität.

Zusammenfassung

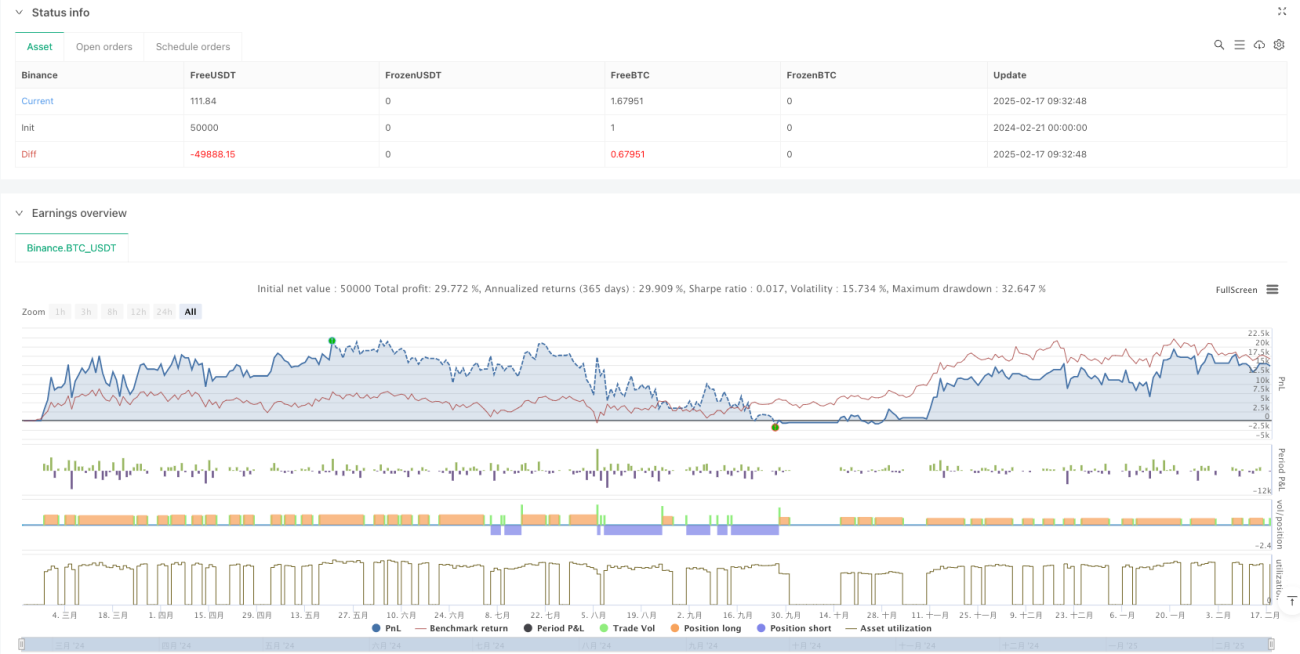

Diese Strategie konstruiert ein robustes Trendfolgesystem durch die Kombination von traditioneller technischer Analyse und modernen Vorhersagemethoden. Ihre Hauptvorteile liegen in der klaren Logik, dem kontrollierten Risiko und der hohen Erweiterbarkeit. Durch Optimierungen, insbesondere bei der Verbesserung des Vorhersagemodells und der Risikokontrolle, kann die Stabilität und Rentabilität der Strategie weiter gesteigert werden. Die Strategie eignet sich für Anleger, die mittel- bis langfristig stabile Erträge anstreben.

- 1