Überblick

Diese Strategie ist ein Multi-Indikator-Handelssystem, das technische Indikatoren wie den exponentiellen gleitenden Durchschnitt (EMA), den Relative-Stärke-Index (RSI) und den Average True Range (ATR) kombiniert und den Average Directional Index (ADX) integriert, um die Genauigkeit der Trendbestimmung zu verbessern. Das System verwendet mehrere Signale, um Einstiegszeitpunkte zu bestätigen, und nutzt den ATR zur dynamischen Verwaltung von Stop-Loss und Take-Profit, um eine effektive Risikokontrolle zu erreichen.

Strategieprinzip

Der Kern der Strategie besteht darin, durch das Zusammenspiel mehrerer technischer Indikatoren Markttrends zu erfassen und Geschäfte zu tätigen. Im Einzelnen:

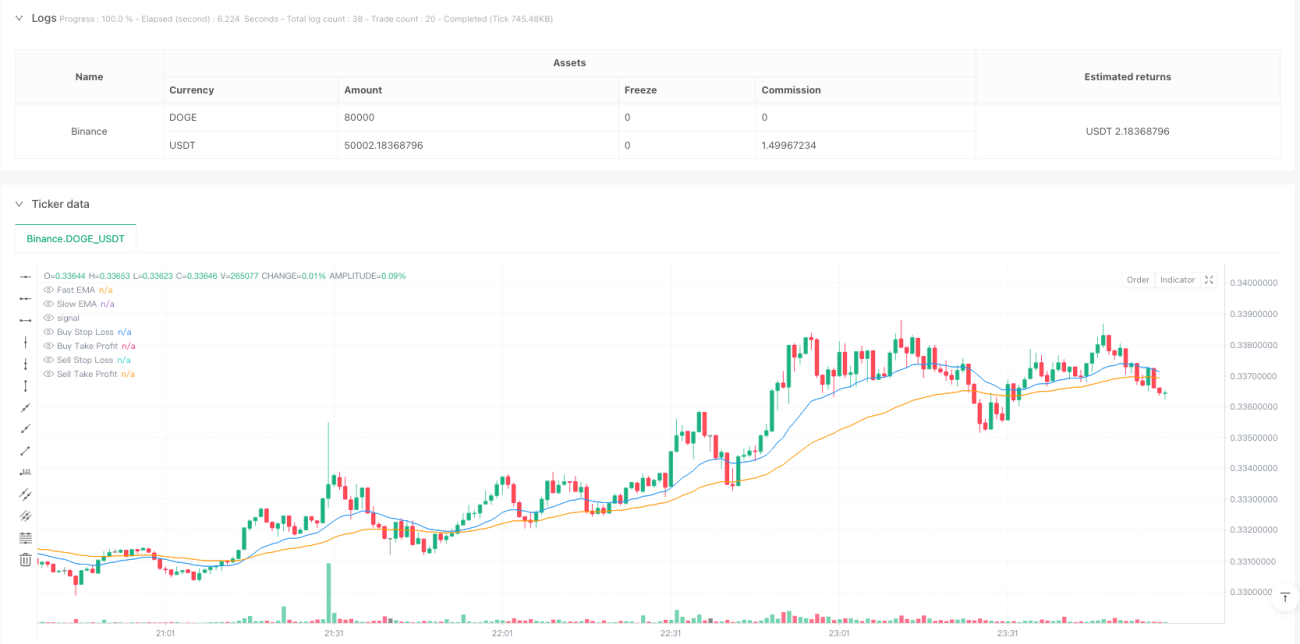

- Verwendung eines schnellen (20-Perioden) und eines langsamen (50-Perioden) EMA zur Bestimmung der Trendrichtung.

- Kombination mit ADX (14-Perioden) zur Bestätigung der Trendstärke; ein ADX > 20 bestätigt einen gültigen Trend.

- Nutzung des RSI (14-Perioden) zur Identifizierung von überkauften/überverkauften Gelegenheiten; RSI-Durchbruch über 30 löst einen Kauf aus, Unterschreitung von 70 löst einen Verkauf aus.

- Berechnung dynamischer Stop-Loss- und Take-Profit-Niveaus mittels ATR (14-Perioden) mit einem Risiko-Ertrags-Verhältnis von 2:1.

Strategievorteile

- Mehrere Signale erhöhen die Genauigkeit des Handels und vermeiden Fehlsignale.

- Die Einbindung des ADX-Indikators verbessert die Zuverlässigkeit der Trendbestimmung.

- Der dynamische Stop-Loss- und Take-Profit-Mechanismus passt sich an die Marktvolatilität an.

- Strenge Risikokontrolle stellt sicher, dass jedes Geschäft beherrschbar ist.

- Die Strategielogik ist klar und die Parameter sind gut anpassbar.

Strategierisiken

- Mehrere Indikatoren können zu Signalverzögerungen führen und den Einstiegszeitpunkt beeinträchtigen.

- In Seitwärtsmärkten kann es zu häufigen Handelsaktivitäten kommen.

- Der ADX-Indikator kann unter bestimmten Marktbedingungen verzögerte Signale liefern.

- Die Parametereinstellungen müssen je nach Marktumfeld optimiert werden.

Optimierungsmöglichkeiten

- Hinzufügen eines Volumenindikators zur Erhöhung der Signalezuverlässigkeit.

- Einführung eines Volatilitätsfilters zur Anpassung der Positionsgröße in Phasen hoher Volatilität.

- Entwicklung eines adaptiven Parameter-Mechanismus zur dynamischen Anpassung an den Marktzustand.

- Aufnahme einer Trendstärkeklassifizierung zur dynamischen Positionsverwaltung.

- Optimierung der Stop-Loss/Take-Profit-Logik durch Einführung eines trailing stops.

Zusammenfassung

Diese Strategie schafft durch die sinnvolle Kombination mehrerer technischer Indikatoren ein vollständiges Trendfolge-Handelssystem. Während sie eine hohe Handelsgenauigkeit gewährleistet, stellt sie durch strenge Risikokontrolle die Sicherheit der Geschäfte sicher. Obwohl es Optimierungspotenzial gibt, bietet das Gesamtgerüst einen guten praktischen Nutzen und Erweiterbarkeit.

/*backtest

start: 2025-01-20 00:00:00

end: 2025-01-31 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"DOGE_USDT"}]

*/

//@version=5

strategy("Enhanced GBP/USD Strategy with ADX", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=1)

// === Input Parameters ===- 1