Multi-Zeitraum-Bitcoin-Trendhandelsstrategie basierend auf der dynamischen Momentumstärke von Multi-Level-EMA und RSI

Übersicht

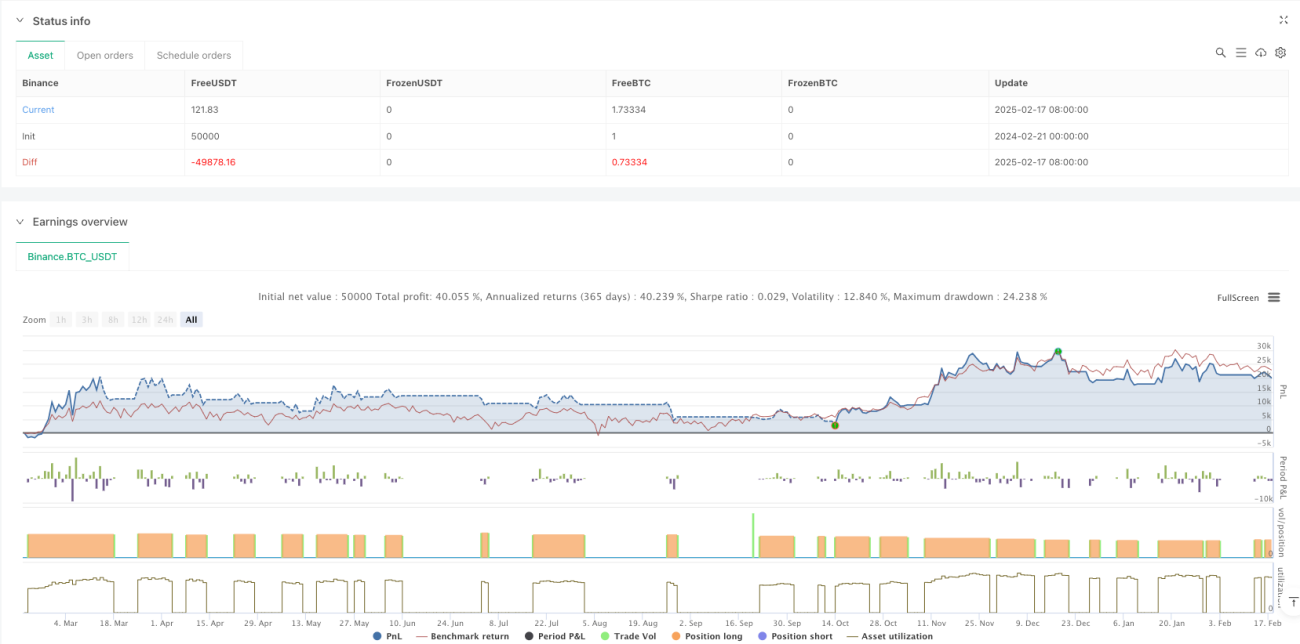

Diese Strategie ist ein Trendfolge-Handelssystem, das auf einer Mehrfachzeitanalyse basiert. Es kombiniert EMA (Exponentielle Gleitende Durchschnitte) auf Wochen- und Tagesbasis sowie den RSI-Indikator, um Markttrends und Momentum zu identifizieren. Die Strategie nutzt die Trendkonsistenz über mehrere Zeitrahmen hinweg, um Handelsmöglichkeiten zu bestimmen, und verwendet einen dynamischen Stop-Loss basierend auf dem ATR zur Risikosteuerung. Das System wendet ein Kapitalmanagement an, bei dem pro Handel 100 % des Kontokapitals eingesetzt werden, und berücksichtigt Handelsgebühren von 0,1 %.

Strategieprinzip

Die Kernlogik der Strategie basiert auf den folgenden Schlüsselelementen:

- Verwendung des wöchentlichen EMA als Haupttrendfilter, in Kombination mit dem Tages-Schlusskurs im Verhältnis zum wöchentlichen EMA zur Bestimmung des Marktstatus

- Dynamische Anpassung der Trendbestimmungsschwelle durch den ATR-Indikator, um die Anpassungsfähigkeit der Strategie zu erhöhen

- Integration des RSI-Momentumindikators als zusätzlicher Handelsfilter

- Verwendung eines Trailing-Stop-Systems basierend auf dem 7-Tage-Tiefstkurs und dem ATR

- Wenn ein Warnsignal für übermäßigen Anstieg auftritt, setzt die Strategie die Eröffnung neuer Positionen aus, um Risiken zu vermeiden

Strategievorteile

- Die Analyse über mehrere Zeitrahmen bietet eine umfassendere Marktperspektive und filtert effektiv falsche Ausbrüche

- Der dynamische Stop-Loss passt sich automatisch an die Marktvolatilität an und bietet eine flexible Risikokontrolle

- Der RSI-Momentumfilter hilft, die Trendstärke zu bestätigen und verbessert die Einstiegsqualität

- Die Warnmechanismen für übermäßigen Anstieg tragen dazu bei, das Risiko von Kursrücksetzern zu vermeiden

- Die Parameter der Strategie sind anpassbar und können leicht an verschiedene Marktumgebungen optimiert werden

Strategierisiken

- In seitwärts tendierenden Märkten kann häufiges Ein- und Aussteigen zu erhöhten Handelskosten führen

- Der Einsatz von 100 % des Kapitals pro Handel birgt ein hohes Risiko von Drawdowns

- Die Abhängigkeit von technischen Indikatoren kann bei unerwarteten Marktereignissen zu Verzögerungen bei der Reaktion führen

- Die Analyse über mehrere Zeitrahmen kann zu widersprüchlichen Signalen auf verschiedenen Ebenen führen

- Der Trailing-Stop kann bei starken Schwankungen vorzeitig ausgelöst werden

Optimierungsmöglichkeiten

- Einführung eines Volatilitätsfilters zur Reduzierung der Handelsfrequenz in Zeiten geringer Volatilität

- Hinzufügen eines Positionsmanagementsystems, das die Positionsgröße dynamisch an den Marktstatus anpasst

- Integration fundamentaler Indikatoren für eine zusätzliche Marktumfeldbewertung

- Optimierung der Trailing-Stop-Parameter zur besseren Anpassung an verschiedene Marktphasen

- Einbeziehung der Volumenanalyse, um die Genauigkeit der Trendbestimmung zu erhöhen

Fazit

Diese Strategie ist ein strukturiertes und logisch klares Trendfolgesystem. Durch die Analyse über mehrere Zeitrahmen und dynamische Indikatorfilter kann sie Haupttrends gut erfassen. Obwohl es inhärente Risiken gibt, bietet die Strategie durch Parameteroptimierung und das Hinzufügen ergänzender Indikatoren erhebliches Verbesserungspotenzial. Es wird empfohlen, vor dem Echtzeithandel umfassende Backtests durchzuführen und die Parameter je nach spezifischer Marktumgebung anzupassen.

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

// @version=6

strategy("Bitcoin Regime Filter Strategy", // Strategy name

overlay=true, // The strategy will be drawn directly on the price chart

initial_capital=10000, // Initial capital of 10000 USD- 1