Mehrstufige RSI-Crossover-Rückkehr-Aufbaustrategie

Überblick

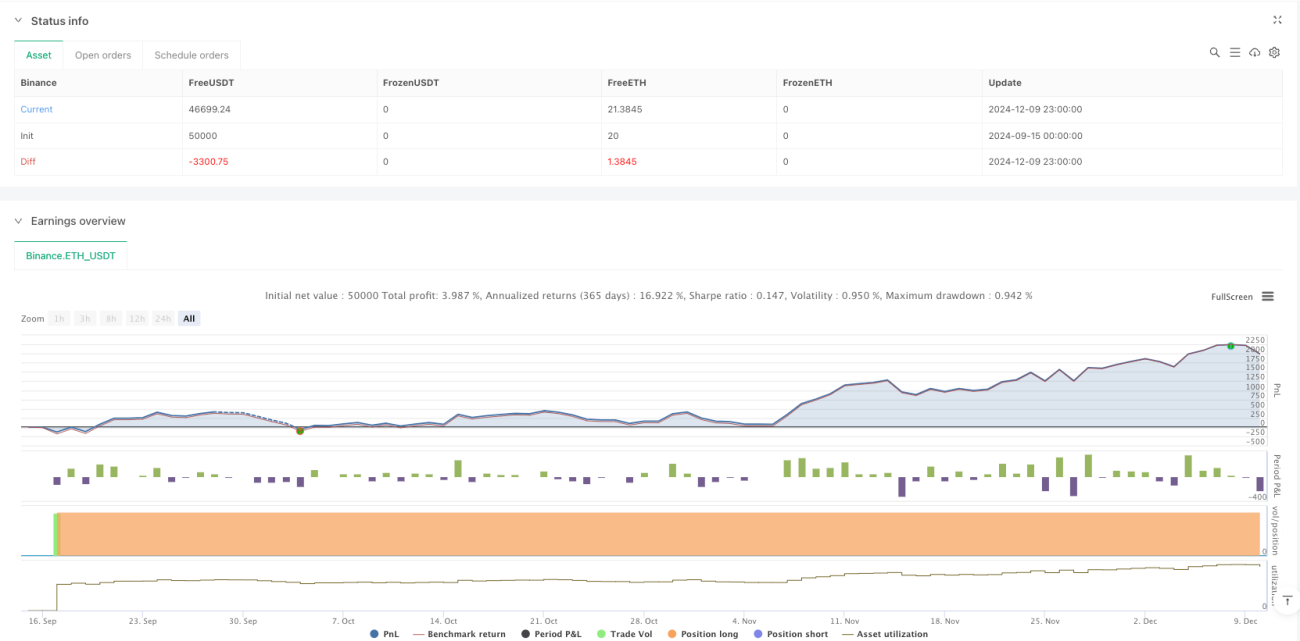

Diese Strategie ist ein automatisiertes Handelssystem, das auf dem Relative-Stärke-Index (RSI) basiert und hauptsächlich darauf abzielt, potenzielle Erholungen durch die Identifizierung überverkaufter Marktbedingungen zu erfassen. Die Strategie verwendet einen schrittweisen Positionsaufbau, bei dem mehrere Positionen bei niedrigen RSI-Kreuzen aufgebaut werden, und das Risiko durch die Festlegung von Gewinnzielen kontrolliert wird. Das System verfügt über einen flexiblen Geldmanagement-Mechanismus, bei dem jede Transaktion 6,6 % des gesamten Kontokapitals nutzt und maximal 15 pyramidenartige Nachkäufe erlaubt sind.

Strategieprinzip

Die Kernlogik der Strategie basiert auf den folgenden Schlüsselelementen:

- Einstiegssignal: Ein Kaufsignal wird ausgelöst, wenn der 14-Perioden-RSI-Indikator das überverkaufte Niveau von 28,5 nach unten durchbricht.

- Positionsmanagement: Ein einzelner Positionsaufbau verwendet 6,6 % des Kontokapitals, maximal 15 schrittweise Positionsaufbauten sind erlaubt.

- Gewinnmitnahme: Wenn der Preis einen Anstieg von 900 % über den durchschnittlichen Einstiegspreis erreicht, werden 50 % der Position geschlossen.

- Visuelle Anzeige: Kauf- und Verkaufssignale, die RSI-Kurve, Einstiegspreise und Zielpreise werden auf dem Chart markiert.

Die Strategie beurteilt die Marktbewegung durch die Beobachtung des RSI-Indikators im überverkauften Bereich. Wenn ein überverkauftes Signal auftritt, wird die Position schrittweise aufgebaut, um die Einstiegskosten zu senken.

Strategievorteile

- Systematischer Positionsaufbau: Handelsmöglichkeiten werden automatisch durch voreingestellte RSI-Parameter identifiziert, wodurch subjektive Verzerrungen durch menschliche Entscheidungen vermieden werden.

- Risikostreuung: Durch den schrittweisen Positionsaufbau werden mehrere Positionen zu unterschiedlichen Kursen eröffnet, wodurch das Risiko effektiv gestreut wird.

- Flexible Anpassung: Die Strategieparameter können an verschiedene Marktbedingungen und individuelle Risikopräferenzen angepasst werden.

- Gewinnsicherung: Ein klares Gewinnziel ist festgelegt; bei Erreichen des Ziels wird die Position automatisch reduziert, um einen Teil der Gewinne zu sichern.

- Kapitaleffizienz: Durch eine angemessene Positionskontrolle und einen Nachkaufmechanismus wird die Effizienz der Kapitalnutzung verbessert.

Strategierisiken

- Trendrisiko: In starken Abwärtstrends kann es zu häufigen Positionseröffnungssignalen kommen, was zu Kapitalverlusten führt.

- Parameterempfindlichkeit: Eine falsche Einstellung von RSI-Parametern oder Positionsgrößen kann die Strategieleistung beeinträchtigen.

- Marktliquidität: In Märkten mit geringer Liquidität kann es schwierig sein, Transaktionen zum Zielpreis durchzuführen.

- Geldmanagement: Übermäßiges Nachkaufen kann zu einem zu großen Risikoengagement führen.

Lösungen:

- Einführung eines Trendfilters, der den Positionsaufbau in klaren Abwärtstrends pausiert.

- Optimierung der Parametereinstellungen durch Backtesting.

- Festlegung eines maximalen Drawdown-Limits.

- Dynamische Anpassung der Nachkaufschwellen.

Strategieoptimierungsrichtung

- Dynamische Parameter: Automatische Anpassung der RSI-Parameter und Einstiegsbedingungen basierend auf der Marktvolatilität.

- Stop-Loss-Mechanismus: Einführung einer Trailing-Stop-Loss-Funktion zur besseren Risikokontrolle.

- Marktfilter: Hinzufügen von Filtern wie Volumen und Trend, um die Signalqualität zu verbessern.

- Ausstiegsoptimierung: Entwicklung eines flexibleren Gewinnmitnahmemechanismus, z. B. schrittweiser Positionsabbau.

- Risikokontrolle: Hinzufügen maximaler Drawdown-Limits und Kontrolle des Risikoengagements.

Zusammenfassung

Die Strategie identifiziert überverkaufte Gelegenheiten mithilfe des RSI-Indikators und kombiniert pyramidenartiges Nachkaufen mit einem festen prozentualen Gewinnmitnahmemechanismus, um ein vollständiges Handelssystem zu bilden. Der Vorteil der Strategie liegt in systematischem Handeln und Risikostreuung, jedoch muss der Einfluss von Markttrends und Parametereinstellungen auf die Strategieleistung beachtet werden. Durch die Hinzufügung von Optimierungen wie dynamischer Parameteranpassung, Stop-Loss-Mechanismen und Marktfiltern kann die Stabilität und Rentabilität der Strategie weiter verbessert werden.

/*backtest

start: 2024-09-15 00:00:00

end: 2024-12-10 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("RSI Cross Under Strategy", overlay=true, initial_capital=1500, default_qty_type=strategy.percent_of_equity, default_qty_value=6.6)

// Input parameters- 1