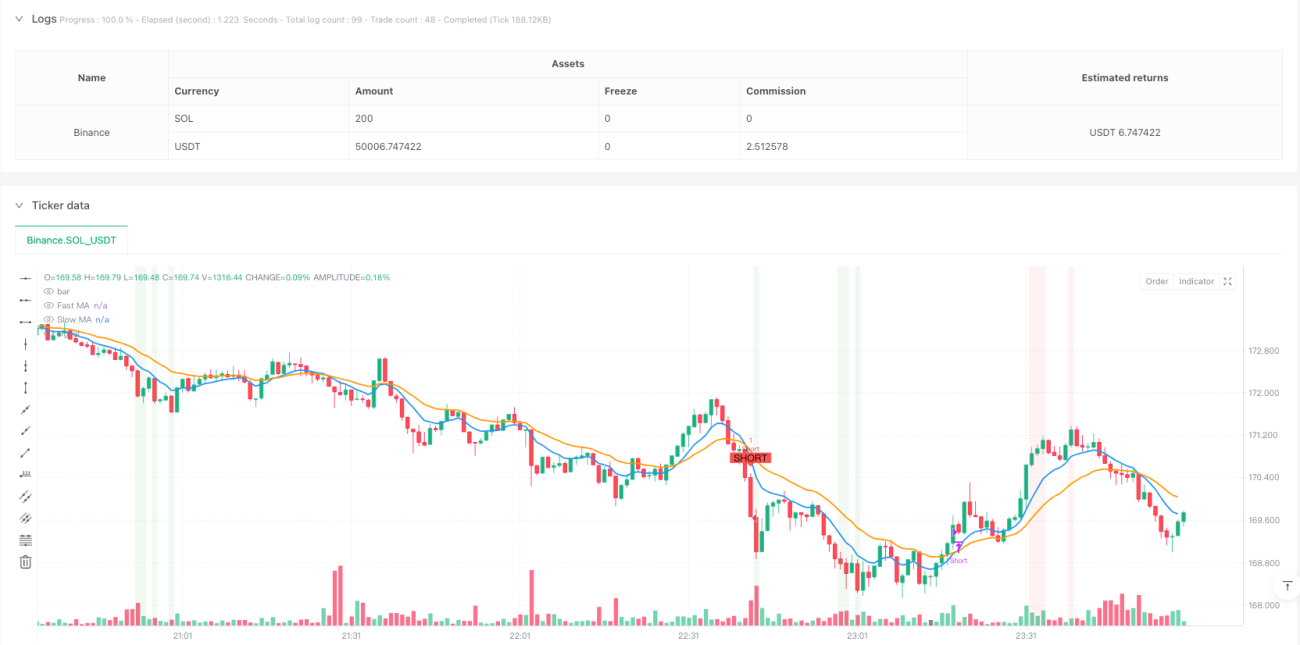

Übersicht

Diese Strategie ist ein intelligentes Handelssystem, das auf Trendfolge und Momentum-Trading basiert und speziell für kurzfristige und schnelle Handelsumgebungen entwickelt wurde. Der Kern der Strategie verwendet ein kombiniertes Entscheidungssystem aus exponentiellen gleitenden Durchschnitten (EMA), dem Relative-Stärke-Index (RSI) und der durchschnittlichen wahren Schwankungsbreite (ATR) und ist mit einem prozentbasierten intelligenten Stop-Loss ausgestattet. Die Strategie eignet sich besonders für den Handel auf kürzeren Zeitrahmen wie 1-Minuten- und 5-Minuten-Charts, indem sie Parameter dynamisch an unterschiedliche Marktbedingungen anpasst.

Strategieprinzip

Die Strategie nutzt drei technische Kernindikatoren, um ein Handelssignal-System aufzubauen:

- Kreuzungssystem aus schnellem und langsamem Exponentiellem Gleitendem Durchschnitt (EMA) – Verwendung einer EMA-Kombination von 9 und 21 Perioden, um Trendrichtung durch Golden Cross und Dead Cross zu bestimmen.

- RSI-Überkauft/Überverkauft-Filter – Verwendung eines 14-Perioden-RSI mit Schwellenwerten von 70 und 30 für überkauft/überverkauft, um Einstiege in extremen Situationen zu vermeiden.

- ATR-Volatilitätsbestätigungsmechanismus – Nutzung des ATR zur Messung der Marktvolatilität, um sicherzustellen, dass Trades nur bei ausreichender Stärke eines Ausbruchs ausgeführt werden.

Die Handelslogik ist klar definiert: Ein Long-Einstieg erfordert, dass die schnelle Linie die langsame Linie nach oben kreuzt, der RSI unter 70 liegt und der Preis das ATR-Mehrfache überschreitet; ein Short-Einstieg erfordert, dass die schnelle Linie die langsame Linie nach unten kreuzt, der RSI über 30 liegt und der Preis das ATR-Mehrfache unterschreitet. Das System ist mit einem dynamischen Stop-Loss von 1 % ausgestattet, um das Risiko effektiv zu kontrollieren.

Strategievorteile

- Mehrere technische Indikatoren überprüfen sich gegenseitig, was die Zuverlässigkeit der Signale erhöht.

- Dynamisches Parameteranpassungssystem, geeignet für verschiedene Zeitrahmen.

- ATR-basierter Volatilitätsfilter reduziert Fehlsignale.

- Intelligenter Stop-Loss-Mechanismus zur strengen Kontrolle des Risikos pro Trade.

- Vollständiges Visualisierungssystem mit klaren grafischen Markierungen und Hintergrundhinweisen.

Strategierisiken

- In Seitwärtsmärkten können häufige Handelssignale entstehen, was die Handelskosten erhöht.

- Ein fester prozentualer Stop-Loss ist möglicherweise nicht für alle Marktbedingungen geeignet.

- In Zeiten hoher Volatilität kann das Risiko von Slippage auftreten.

- Die Parameteroptimierung erfordert kontinuierliche Überwachung und Anpassung.

Zur Risikominderung wird Folgendes empfohlen:

- Anpassung des Stop-Loss-Prozentsatzes je nach Eigenschaften des Instruments.

- Einführung eines Trendstärke-Bestätigungsmechanismus.

- Echtzeit-Überwachung der Marktvolatilität.

- Aufbau eines umfassenden Kapitalmanagementsystems.

Optimierungsrichtungen der Strategie

- Einführung eines adaptiven Stop-Loss-Mechanismus, der die Stop-Loss-Prozentsätze dynamisch an die Marktvolatilität anpasst.

- Hinzufügen eines Trendstärke-Filters zur Verbesserung der Signalqualität.

- Entwicklung eines intelligenten Zeitfiltersystems zur Vermeidung von Handelszeiten mit geringer Liquidität.

- Integration von Volumenindikatoren zur Erhöhung der Signalzuverlässigkeit.

- Entwicklung eines dynamischen Parameteroptimierungssystems zur automatischen Anpassung der Strategie.

Zusammenfassung

Diese Strategie nutzt das Zusammenspiel mehrerer technischer Indikatoren, um ein vollständiges Handelssystem zu schaffen. Das System bleibt flexibel und gewährleistet gleichzeitig durch strenge Risikokontrollen die Handelssicherheit. Obwohl es gewisse Einschränkungen gibt, bietet die Strategie durch kontinuierliche Optimierung und Verbesserung gutes Anwendungspotenzial und Entwicklungsperspektiven.

- 1