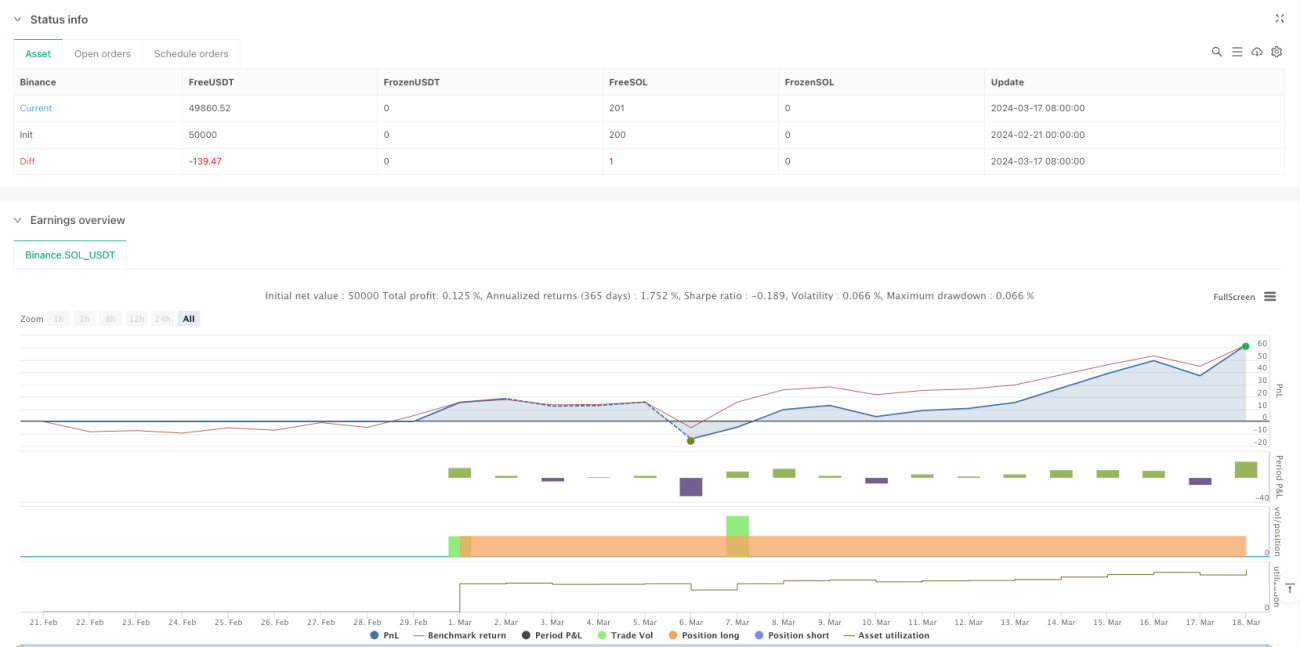

Überblick

Diese Strategie ist ein Trendfolge-Handelssystem, das den Donchian-Kanal (Donchian Channel) mit einem 200-Perioden-einfachen gleitenden Durchschnitt (SMA) kombiniert. Die Strategie erkennt potenzielle Long- und Short-Signale, indem sie den Durchbruch des Preises durch die obere/untere Linie des Donchian-Kanals zusammen mit dem SMA-Verlauf beobachtet. Zusätzlich ist ein dynamischer Stop-Loss-Mechanismus basierend auf der Mittellinie des Kanals implementiert, um das Risiko zu kontrollieren.

Strategieprinzip

Der Kern der Strategie basiert auf den folgenden Schlüsselelementen:

- Verwendung eines 20-Perioden-Intervalls zur Berechnung der oberen, unteren und mittleren Linie des Donchian-Kanals

- Kombination mit dem 200-Perioden-SMA-Verlauf zur Bestimmung der allgemeinen Trendrichtung

- Einstiegssignale:

- Wenn der Preis die obere Linie des Donchian-Kanals nach oben durchbricht und über dem SMA200 liegt, wird ein Long-Signal ausgelöst

- Wenn der Preis die untere Linie des Donchian-Kanals nach unten durchbricht und unter dem SMA200 liegt, wird ein Short-Signal ausgelöst

- Stop-Loss-Einstellung:

- Der Long-Stop-Loss wird unterhalb der Mittellinie des Kanals bei 45% Abstand platziert

- Der Short-Stop-Loss wird oberhalb der Mittellinie des Kanals bei 45% Abstand platziert

Strategievorteile

- Effektive Trendfolge: Durch die Kombination von Donchian-Kanal-Durchbrüchen und SMA200-Trendbestätigung werden mittel- bis langfristige Trends effektiv erfasst

- Angemessenes Risikomanagement: Der auf der Mittellinie basierende dynamische Stop-Loss passt sich je nach Marktvolatilität automatisch an

- Einfache Parametereinstellung: Nur zwei Hauptparameter (Kanalperiode und gleitende Durchschnittsperiode) erforderlich, was das Risiko einer Überoptimierung verringert

- Klare Logik: Ein- und Ausstiegsbedingungen sind eindeutig und leicht verständlich umsetzbar

- Hohe Anpassungsfähigkeit: Auf verschiedene Handelsinstrumente und Zeitrahmen anwendbar

Strategierisiken

- Risiko in Seitwärtsmärkten: In einer range-tradenden Phase können häufige Fehldurchbrüche zu aufeinanderfolgenden Stop-Loss-Verlusten führen

- Slippage-Risiko: Bei schnellen Kursbewegungen kann der tatsächliche Ausführungspreis erheblich vom Signalkurs abweichen

- Trendumkehrrisiko: Bei einer großen Trendwende können erhebliche Rücksetzer auftreten

- Parameterempfindlichkeit: Die Wahl der Kanalperiode und des gleitenden Durchschnitts beeinflusst die Strategieleistung erheblich

Risikomanagement-Empfehlungen:

- Es wird empfohlen, die Signale mit anderen technischen Indikatoren zu validieren

- Ein Trendstärke-Filter kann hinzugefügt werden

- Dynamisches Positionsmanagement in Betracht ziehen

- Regelmäßige Überprüfung und Optimierung der Strategieparameter

Strategieoptimierungsrichtungen

-

Signaloptimierung:

- Einführung eines Volumenbestätigungsmechanismus

- Integration eines Trendstärkeindikators

- Analyse von Preisformationen

-

Stop-Loss-Optimierung:

- Untersuchung des optimalen Stop-Loss-Prozentsatzes

- Hinzufügen eines Trailing-Stop-Mechanismus

- Berücksichtigung eines volatilitätsadaptiven Stop-Loss

-

Positionsmanagement-Optimierung:

- Umsetzung eines volatilitätsbasierten dynamischen Positionskontrollsystems

- Schrittweiser Auf- und Abbau von Positionen

-

Timing-Optimierung:

- Einführung eines Marktumfeld-Erkennungsmechanismus

- Optimierung des Handelszeitfilters

Zusammenfassung

Diese Strategie kombiniert den klassischen Donchian-Kanal mit einem gleitenden Durchschnitt und bildet ein logisch klares, risikokontrollierbares Trendfolgesystem. Die Hauptvorteile liegen in den klaren Signalen und dem angemessenen Risikomanagement, während die Performance in Seitwärtsmärkten möglicherweise nachlässt. Durch die Ergänzung von Volumenbestätigung, Optimierung des Stop-Loss-Mechanismus und Einführung eines dynamischen Positionsmanagements bietet die Strategie noch erhebliches Optimierungspotenzial. Händlern wird empfohlen, bei der praktischen Anwendung ein sorgfältiges Risikomanagement zu betreiben und die Strategie je nach Handelsinstrument und Marktumfeld gezielt anzupassen.

- 1