Intelligentes mehrdimensionales adaptives Trendhandelssystem

Überblick

Diese Strategie ist ein intelligentes Handelssystem, das mehrere technische Indikatoren kombiniert und durch die umfassende Analyse von Fair Value Gap (FVG), Trendsignalen und Preisbewegungen Marktchancen identifiziert. Das System verwendet eine duale Strategiemechanik, die Trendfolge und Swing-Trading vereint, und optimiert die Handelsleistung durch dynamisches Positionsmanagement und mehrdimensionale Ausstiegsmechanismen. Die Strategie legt besonderen Wert auf Risikokontrolle und verbessert die Signalqualität durch Volatilitätsfilter und Volumenbestätigung.

Strategieprinzip

Die Kernlogik der Strategie basiert auf den folgenden Dimensionen:

- FVG-Lückenidentifikation – Berechnung der Größe von Preisabständen, um potenzielle Handelsmöglichkeiten zu finden

- Trendbestätigungssystem – Kombination von 200-Tage-Durchschnitt, SuperTrend-Indikator und MACD zur Bestätigung des Markttrends

- Smart-Money-Bestätigung – Nutzung von RSI-Überkauft/Überverkauft, abnormalem Volumen und Preisverhaltensmustern als Auslöser für Trades

- Dynamisches Positionsmanagement – Anpassung der Positionsgröße basierend auf der ATR-Volatilität, um einheitliches Risikoengagement sicherzustellen

- Mehrstufiger Ausstiegsmechanismus – Kombination von trailing Stop und gewinnorientiertem Ziel zur Steuerung von Trade-Ausstiegen

Strategievorteile

- Hohe Anpassungsfähigkeit – Die Strategie passt Parameter und Positionen automatisch an die Marktvolatilität an

- Umfassende Risikokontrolle – Risikominimierung durch mehrstufige Filter und striktes Positionsmanagement

- Zuverlässige Signalqualität – Verbesserung der Genauigkeit von Handelssignalen durch Bestätigung mehrerer Indikatoren

- Flexible Handelsweise – Gleichzeitige Erfassung von Chancen in Trend- und Seitwärtsmärkten

- Wissenschaftliches Geldmanagement – Prozentuales Risikomanagement für eine sinnvolle Kapitalallokation

Strategierisiken

- Parameterempfindlichkeit – Die Einstellung mehrerer Parameter kann die Strategieleistung beeinflussen und erfordert kontinuierliche Optimierung

- Abhängigkeit vom Marktumfeld – In manchen Märkten können falsche Ausbruchssignale auftreten

- Slippage-Einfluss – In illiquiden Märkten kann es zu erheblichen Slippages kommen

- Rechenkomplexität – Die Berechnung vieler Indikatoren kann zu Signalverzögerungen führen

- Hoher Kapitalbedarf – Für die vollständige Umsetzung der Strategie ist ein erhebliches Anfangskapital erforderlich

Optimierungsrichtungen der Strategie

- Optimierung der Indikatorgewichte – Einführung maschineller Lernmethoden zur dynamischen Anpassung der Gewichtung der Indikatoren

- Verbesserung der Marktanpassungsfähigkeit – Hinzufügung eines adaptiven Mechanismus für die Marktvolatilität

- Verbesserung der Signalfilter – Einbeziehung weiterer Mikrostrukturindikatoren des Marktes

- Optimierung des Ausführungsmechanismus – Einführung intelligenter Order-Splitting-Mechanismen zur Reduzierung von Marktauswirkungen

- Aufwertung der Risikokontrolle – Hinzufügung eines dynamischen Risikobudget-Managementsystems

Zusammenfassung

Die Strategie baut durch die kombinierte Nutzung mehrerer technischer Indikatoren und Handelsmethoden ein vollständiges Handelssystem auf. Ihr Vorteil liegt in der Fähigkeit, sich an Marktveränderungen anzupassen, während gleichzeitig eine strenge Risikokontrolle gewahrt bleibt. Obwohl es Optimierungspotenzial gibt, handelt es sich insgesamt um eine gut entworfene quantitative Handelsstrategie.

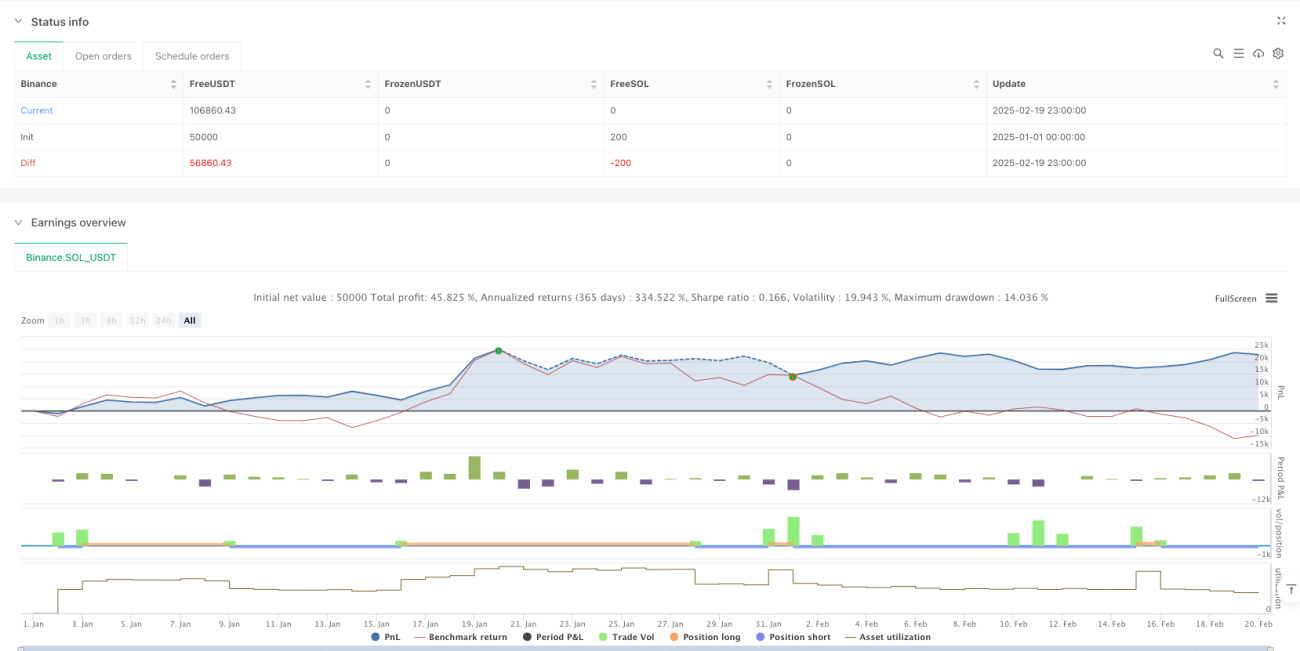

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging Options- 1