Überblick

Die intelligente Handelsstrategie mit mehreren Indikatoren und Gewichtung ist ein umfassendes quantitatives Handelssystem, das Signale mehrerer technischer Indikatoren integriert und mit unterschiedlichen Gewichtungen versieht, um Handelsentscheidungen zu generieren. Die Strategie kombiniert verschiedene technische Analyseinstrumente wie MACD, Stochastic RSI, EMA, Super Trend und gleitende Durchschnitte (Kreuzungen) zu einem umfassenden Handelsrahmen. Das System unterstützt nicht nur mehrstufige Take-Profit- und dynamische Stop-Loss-Mechanismen, sondern passt auch automatisch die Handelsparameter an die Marktbedingungen an, sodass es in verschiedenen Marktumgebungen eine hohe Anpassungsfähigkeit behält. Die Strategie eignet sich besonders für mittel- bis langfristige Trader und macht Handelsentscheidungen durch das Gewichtungssystem robuster und zuverlässiger.

Strategieprinzip

Der Kern der Strategie liegt in ihrem gewichteten Signalsystem, das Handelssignale aus fünf verschiedenen Unterstrategien generiert:

-

MACD-Strategie: Nutzt den Kreuzen der MACD-Linie mit der Signallinie, um die Markttrendrichtung zu bestimmen. Ein Kaufsignal entsteht, wenn die MACD-Linie die Signallinie von unten kreuzt, ein Verkaufssignal beim Kreuzen von oben.

-

Stochastic-RSI-Strategie: Kombiniert die Vorteile von RSI und Stochastic, um überkaufte/überverkaufte Marktzustände zu überwachen. Ein Kaufsignal entsteht, wenn der Stochastic RSI unter den festgelegten überverkauften Schwellenwert fällt, ein Verkaufssignal bei Überschreiten des überkauften Schwellenwerts.

-

EMA-Überkauft/Überverkauft-Strategie: Verwendet EMA, um die Abweichung des Preises vom Durchschnitt zu identifizieren. Ein Kaufsignal entsteht, wenn der RSI unter den überverkauften Schwellenwert fällt, ein Verkaufssignal bei Überschreiten des überkauften Schwellenwerts.

-

Super-Trend-Strategie: Basiert auf ATR-Multiplikatoren, um einen Preiskorridor zu setzen und die Handelsrichtung durch Trendwechsel zu bestimmen. Ein Kaufsignal entsteht, wenn der Super-Trend-Indikator von negativ auf positiv wechselt, ein Verkaufssignal bei Wechsel von positiv auf negativ.

-

Gleitender-Durchschnitt-Kreuzungsstrategie: Nutzt das Kreuzen von zwei gleitenden Durchschnitten unterschiedlicher Perioden zur Markttrendbestimmung. Ein Kaufsignal entsteht, wenn der kurzfristige gleitende Durchschnitt den langfristigen von unten kreuzt, ein Verkaufssignal beim Kreuzen von oben.

Die Strategie gewichtet die Signale der einzelnen Unterstrategien über ein anpassbares Gewichtungssystem. Ein Handel wird nur ausgelöst, wenn die gewichtete Summe einen festgelegten Schwellenwert überschreitet. Zusätzlich enthält die Strategie einen Mechanismus zur Erkennung potenzieller Hochs und Tiefs, der die Positionen bei möglichen Marktumkehrungen anpassen kann.

Diese mehrstufige Signalbestätigung reduziert effektiv Fehlsignale und erhöht die Zuverlässigkeit des Handelssystems, während die flexiblen Parametereinstellungen es der Strategie ermöglichen, sich an verschiedene Handelsinstrumente und Zeitrahmen anzupassen.

Strategievorteile

-

Mehrfache Signalbestätigung: Die gewichtete Berechnung der Signale aus fünf unabhängigen technischen Indikatoren reduziert die Irreführung durch einzelne Indikatoren und verbessert die Qualität und Zuverlässigkeit der Handelssignale.

-

Adaptives Gewichtungssystem: Jeder Unterstrategie können unterschiedliche Gewichte zugewiesen werden, sodass der Trader den Schwerpunkt der Strategie basierend auf seinem Vertrauen in die einzelnen Indikatoren und ihrer historischen Performance anpassen kann, was die Flexibilität erhöht.

-

Umfassendes Risikomanagement: Die Strategie verfügt über mehrstufige Risikokontrollmechanismen, darunter Stop-Loss, mehrstufige Take-Profits und dynamische Nachführung von Stop-Loss-Positionen, um bei ungünstigen Marktbewegungen schnell Risiken zu kontrollieren.

-

Automatisierte Erkennung potenzieller Hochs/Tiefs: Durch die umfassende Analyse von RSI, Handelsvolumen und Preisbewegungen kann die Strategie potenzielle Markt-Hochs und -Tiefs identifizieren und zu geeigneten Zeitpunkten Teilpositionen schließen, um Gewinne zu sichern oder Verluste zu begrenzen.

-

Hohe Anpassbarkeit: Nahezu alle Parameter können angepasst werden, einschließlich der Berechnungszeiträume der Indikatoren, Gewichtungswerte, Take-Profit/Stop-Loss-Prozentsätze usw., sodass der Trader die Strategie an seinen persönlichen Stil und unterschiedliche Marktbedingungen optimieren kann.

-

Integrierter Verzögerungsmechanismus: Um zu frühe Einstiege oder Handelsentscheidungen auf Basis von Rauschen zu vermeiden, verwendet die Strategie einen Verzögerungsbestätigungsmechanismus, der sicherstellt, dass nur anhaltende Signale einen Handel auslösen, wodurch der Einfluss kurzfristiger Schwankungen reduziert wird.

-

Zeitfilterfunktion: Die Strategie ermöglicht die Festlegung von Start- und Enddaten für den Handel, sodass der Trader die Performance über bestimmte Zeiträume im Backtest testen oder bekannte Phasen anomaler Marktschwankungen vermeiden kann.

Strategierisiken

-

Risiko der Parameterüberoptimierung: Aufgrund der vielen Parameter besteht die Gefahr der Überanpassung an historische Daten, was zu einer schlechten Performance im Live-Handel führen kann. Lösung: Backtest über mehrere Zeiträume und Instrumente durchführen, relativ robuste Parametereinstellungen verwenden und eine übermäßige Optimierung auf bestimmte historische Daten vermeiden.

-

Risiko sich ändernder Marktbedingungen: Die Performance der Strategie kann in Trend- und Seitwärtsmärkten unterschiedlich sein; plötzliche Änderungen der Marktlage können die Wirksamkeit beeinträchtigen. Lösung: Ein Marktzustandserkennungsmechanismus einführen, um Parameter anzupassen oder den Handel in verschiedenen Marktphasen auszusetzen.

-

Risiko von Signalwidersprüchen: Die gleichzeitige Verwendung mehrerer Indikatoren kann zu widersprüchlichen Signalen führen, was die Entscheidungsfindung erschwert. Lösung: Die Gewichtungen der Indikatoren angemessen setzen, zuverlässigere Indikatoren betonen und sicherstellen, dass die Signalschwellenwerte sinnvoll sind, um Konflikte zu reduzieren.

-

Risiko unangemessenen Geldmanagements: Obwohl die Strategie Stop-Loss-Mechanismen enthält, kann ein unangemessenes Geldmanagement dennoch zu schnellem Kapitalverlust führen. Lösung: Den Kapitalanteil pro Handel streng kontrollieren, um sicherzustellen, dass das maximale Risiko pro Handel im akzeptablen Bereich liegt.

-

Risiko technischer Störungen: Automatisierte Handelssysteme können unter Netzwerkunterbrechungen, Datenverzögerungen und anderen technischen Problemen leiden. Lösung: Manuelle Eingreifmechanismen einrichten, den Systemstatus regelmäßig überwachen und Ausnahmen zeitnah behandeln.

Optimierungsrichtungen

-

Hinzufügen eines Marktumgebungsfilters: Entwicklung eines Indikators, der erkennt, ob der aktuelle Markt trendend oder seitwärts ist, und die Gewichtung der Unterstrategien dynamisch anpasst – Stärkung der Trendfolgestrategien in Trendmärkten und der Oszillatorstrategien in Seitwärtsmärkten.

-

Integration von maschinellem Lernen: Einsatz von maschinellem Lernen zur automatischen Anpassung der Parameter und Gewichtungen der einzelnen Indikatoren, damit die Strategie kontinuierlich aus den neuesten Marktdaten lernen und sich anpassen kann, wodurch die dynamische Anpassungsfähigkeit erhöht wird.

-

Erweiterung der Volumenanalyse: Volumenveränderungen als zusätzliches Bestätigungssignal verwenden – Trades nur dann ausführen, wenn das Volumen die Erwartungen unterstützt, um die Glaubwürdigkeit der Signale zu erhöhen.

-

Optimierung des Erkennungsalgorithmus für potenzielle Hochs/Tiefs: Verbesserung der bestehenden Logik zur Erkennung von Hochs/Tiefs durch Hinzufügen weiterer Bestätigungsfaktoren wie Preisformationen, mehrperiodische Bestätigungen usw., um die Genauigkeit zu erhöhen.

-

Integration von Stimmungsindikatoren: Einbeziehung von Marktstimmungsindikatoren wie dem VIX (Angstindex), Put/Call-Ratio usw., um bei extremer Marktstimmung die Handelsstrategie anzupassen oder den Handel auszusetzen und übermäßigen Handel in Phasen hoher Volatilität zu vermeiden.

-

Entwicklung dynamischer Take-Profit/Stop-Loss-Mechanismen: Automatische Anpassung von Take-Profit- und Stop-Loss-Niveaus basierend auf der Marktvolatilität: in Märkten mit hoher Volatilität breitere Stop-Loss-Spannen, in Märkten mit niedriger Volatilität engere Stop-Loss-Spannen – für ein flexibleres und effektiveres Risikomanagement.

-

Optimierung der Zeitrahmen: Erweiterung um eine Multi-Timeframe-Analyse, bei der sowohl höhere als auch niedrigere Zeitrahmen das Signal bestätigen müssen, um Fehlausbrüche und Fehlsignale zu reduzieren.

Zusammenfassung

Die intelligente Handelsstrategie mit mehreren Indikatoren und Gewichtung baut durch die Integration verschiedener technischer Analyseinstrumente und die Zuweisung unterschiedlicher Gewichtungen ein umfassendes und flexibles Handelssystem auf. Diese Strategie verfügt nicht nur über mehrfache Signalbestätigung, ein adaptives Gewichtungssystem und umfassende Risikomanagementfunktionen, sondern auch über einen automatisierten Mechanismus zur Erkennung potenzieller Hochs und Tiefs, der ihr eine hohe Anpassungsfähigkeit in komplexen und sich ständig ändernden Marktumgebungen verleiht.

Obwohl potenzielle Risiken wie Parameterüberoptimierung, sich ändernde Marktbedingungen und Signalwidersprüche bestehen, können diese durch angemessene Parametereinstellungen, Marktumgebungserkennung und strenges Geldmanagement kontrolliert werden. Zukünftige Optimierungsrichtungen umfassen das Hinzufügen von Marktumgebungsfiltern, die Integration von maschinellem Lernen, die Verbesserung der Volumenanalyse und die Optimierung des Erkennungsalgorithmus für potenzielle Hochs/Tiefs. Diese Verbesserungen werden die Stabilität und Rentabilität der Strategie weiter steigern.

Für Anleger, die einen systematischen Handelsansatz suchen, bietet diese intelligente Handelsstrategie mit mehreren Indikatoren und Gewichtung einen überlegenswerten Rahmen. Sie reduziert nicht nur den Einfluss emotionaler Faktoren auf Handelsentscheidungen, sondern optimiert die Handelsleistung kontinuierlich auf datengesteuerte Weise. Bei der Implementierung dieser Strategie wird empfohlen, mit konservativen Parametereinstellungen zu beginnen, diese schrittweise anzupassen und die Performance der Strategie genau zu überwachen, um die Konfiguration zu finden, die am besten zur persönlichen Risikoneigung und den Marktbedingungen passt.

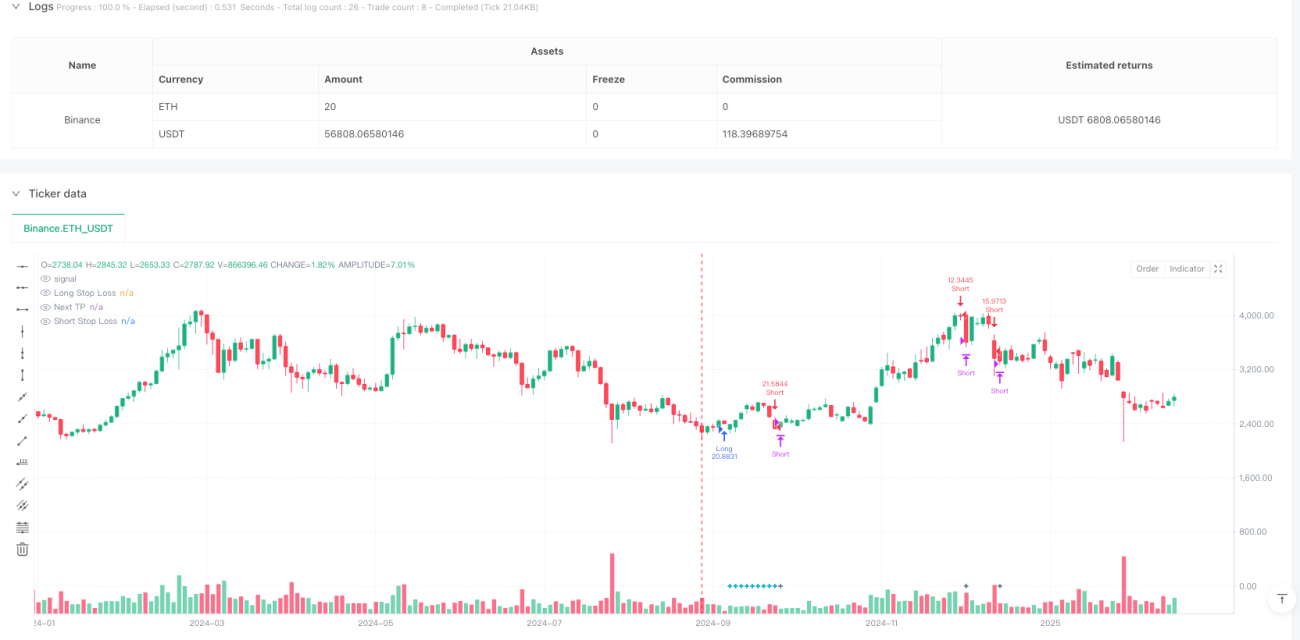

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1