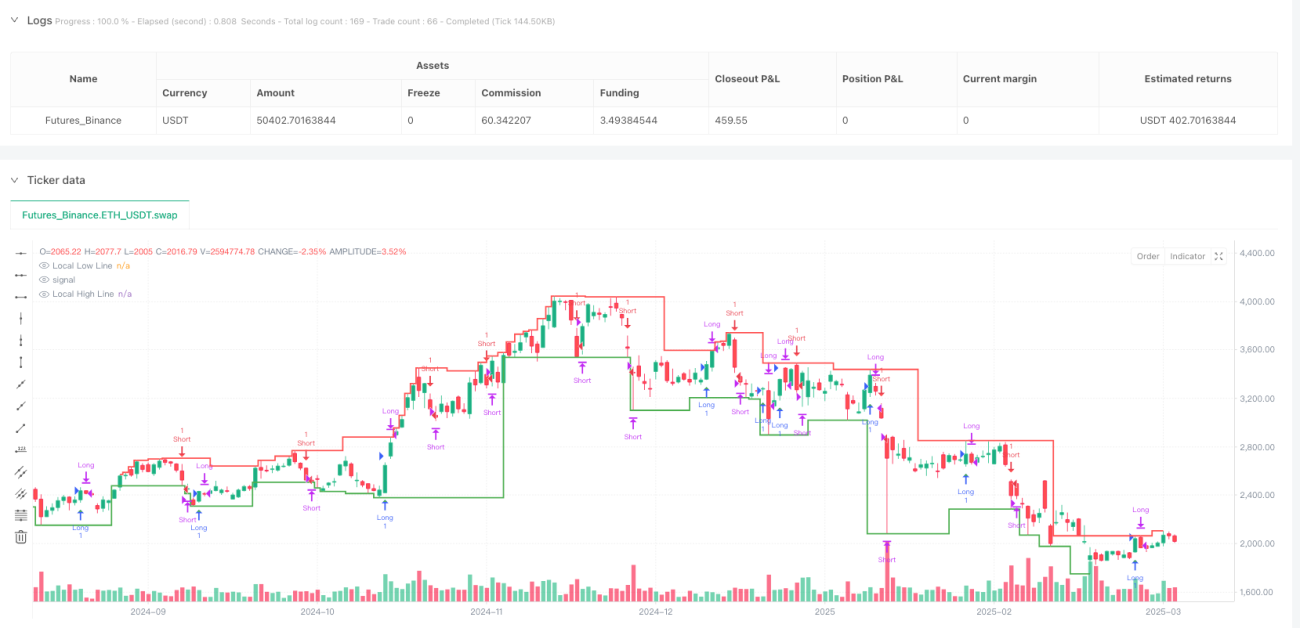

Überblick

Dies ist eine innovative Handelsstrategie, die Liquiditätszonenanalyse mit internen Marktstrukturdynamiken kombiniert, um Einstiegspunkte mit hoher Wahrscheinlichkeit zu identifizieren. Die Strategie verfolgt die Interaktion des Preises mit wichtigen Marktniveaus und nutzt interne Marktumschaltungen, um Handelsauslöser zu generieren. Sie bietet Händlern eine flexible und präzise Methode zum Einstieg in den Markt.

Strategieprinzip

Der Kernlogik der Strategie liegen zwei Schlüsselkomponenten zugrunde: die Identifizierung von Liquiditätszonen und die interne Marktumschaltung. Liquiditätszonen werden dynamisch durch die Analyse lokaler Hochs und Tiefs bestimmt, während die interne Marktumschaltung auf dem Durchbruch des Preises durch vorherige bullische oder bärische Niveaus basiert, um eine Richtungsänderung des Marktes zu erkennen.

Die Strategie zeichnet sich durch folgende Kernfunktionen aus:

- Interne Marktumschaltungslogik: Sie verlässt sich nicht auf traditionelle Candlestick-Muster, sondern auf Preisausbrüche durch entscheidende Niveaus.

- Liquiditätszonenverfolgung: Dynamische Identifizierung wichtiger Liquiditätszonen, um den Handel unter schwachen Marktbedingungen zu vermeiden.

- Modusflexibilität: Es werden drei Handelsmodi angeboten: "Both", "Bullish Only" und "Bearish Only".

- Risikomanagement: Anpassbare Stop-Loss- und Take-Profit-Niveaus.

- Zeitbereichskontrolle: Präzise Steuerung der Handelszeitspanne.

Strategievorteile

- Dynamische Anpassungsfähigkeit: Die Strategie kann schnell auf Veränderungen der Marktstruktur reagieren.

- Präziser Einstieg: Durch die Kombination von Liquiditätszonen und interner Marktumschaltung wird die Einstiegsgenauigkeit erhöht.

- Kontrolliertes Risiko: Integrierte Stop-Loss- und Take-Profit-Mechanismen.

- Hohe Flexibilität: Je nach Marktbedingungen kann der Handelsmodus gewählt werden.

- Mehrdimensionale Analyse: Gleichzeitige Berücksichtigung von Preisverhalten, Liquidität und Marktstruktur.

Strategierisiken

- Starke Marktschwankungen können dazu führen, dass Stop-Loss ausgelöst wird.

- In Seitwärtsmärkten können häufige Signale die Handelskosten erhöhen.

- Falsche Parametereinstellungen können die Strategieleistung beeinträchtigen.

- Backtest-Ergebnisse können von Live-Ergebnissen abweichen.

Optimierungsmöglichkeiten

- Einführung von Algorithmen des maschinellen Lernens zur adaptiven Parameteroptimierung.

- Hinzufügen weiterer Filterbedingungen wie Volumen, Volatilitätsindikatoren.

- Entwicklung eines Bestätigungsmechanismus über mehrere Zeitrahmen.

- Optimierung der Stop-Loss- und Take-Profit-Algorithmen unter Berücksichtigung dynamischer Anpassungen an die Marktvolatilität.

Zusammenfassung

Dies ist eine innovative Handelsstrategie, die Liquiditätsanalyse und Dynamik der Marktstruktur vereint. Durch eine flexible interne Marktumschaltungslogik und präzise Liquiditätszonenverfolgung bietet sie Händlern ein leistungsstarkes Handelswerkzeug. Der Schlüssel der Strategie liegt in ihrer Anpassungsfähigkeit und mehrdimensionalen Analysefähigkeit, die es ermöglicht, unter verschiedenen Marktbedingungen eine hohe Ausführungseffizienz beizubehalten.

- 1