Übersicht

Diese Strategie ist eine dynamische Optionshandelsstrategie, die auf mehreren technischen Indikatoren basiert. Ziel ist es, durch die umfassende Analyse von Marktvolatilität, Trend und Momentum hochwahrscheinliche Handelsmöglichkeiten zu identifizieren. Die Strategie kombiniert mehrere technische Indikatoren wie den Average True Range (ATR), Bollinger-Bänder (BB), den Relative-Stärke-Index (RSI) und den volumengewichteten Durchschnittspreis (VWAP), um einen umfassenden Entscheidungsrahmen zu schaffen.

Funktionsweise der Strategie

Das Kernprinzip der Strategie besteht darin, multiple Marktsignale zu nutzen, um Handelsentscheidungen zu treffen. Die wesentlichen Schritte umfassen:

- Verwendung der oberen und unteren Bollinger-Bänder als Preisausbruchssignale

- Kombination mit dem RSI zur Beurteilung überkaufter oder überverkaufter Marktbedingungen

- Bestätigung des Trends durch Volumenanomalie-Erkennung

- Berechnung dynamischer Stop-Loss- und Take-Profit-Ziele mittels ATR

- Festlegung einer maximalen Haltedauer zur Begrenzung des Risikos

Vorteile der Strategie

- Multi-Faktor-Analyse erhöht die Genauigkeit der Handelssignale

- Dynamische Stop-Loss- und Take-Profit-Mechanismen kontrollieren das Risiko effektiv

- Flexible Parametereinstellungen passen sich verschiedenen Marktbedingungen an

- Backtest-Ergebnisse zeigen eine hohe Gewinnrate und einen hohen Profitfaktor

- Zeitbasierte Ausstiegsstrategie verhindert übermäßiges Halten von Positionen

Risiken der Strategie

- Zeitliche Verzögerung technischer Indikatoren kann zu Fehlsignalen führen

- Hohe Marktvolatilität kann die Handelskomplexität erhöhen

- Die Parameterauswahl ist entscheidend für die Strategieleistung

- Transaktionskosten und Slippage können die tatsächlichen Erträge beeinflussen

- Schnell ändernde Marktbedingungen können die Effektivität der Strategie verringern

Optimierungsmöglichkeiten

- Einführung von maschinellen Lernalgorithmen zur Optimierung der Parameterauswahl

- Hinzufügung weiterer Marktstimmungsindikatoren

- Entwicklung dynamischer Parameteranpassungsmechanismen

- Optimierung des Risikomanagement-Moduls

- Einbeziehung von Korrelationsanalysen über Märkte hinweg

Zusammenfassung

Die Strategie schafft durch Multi-Faktor-Analyse einen relativ robusten Optionshandelsrahmen. Durch die Kombination technischer Indikatoren, Risikokontrolle und dynamischer Ausstiegsmechanismen bietet sie Händlern eine systematische Handelsmethode. Jede Handelsstrategie erfordert jedoch eine kontinuierliche Validierung und Optimierung.

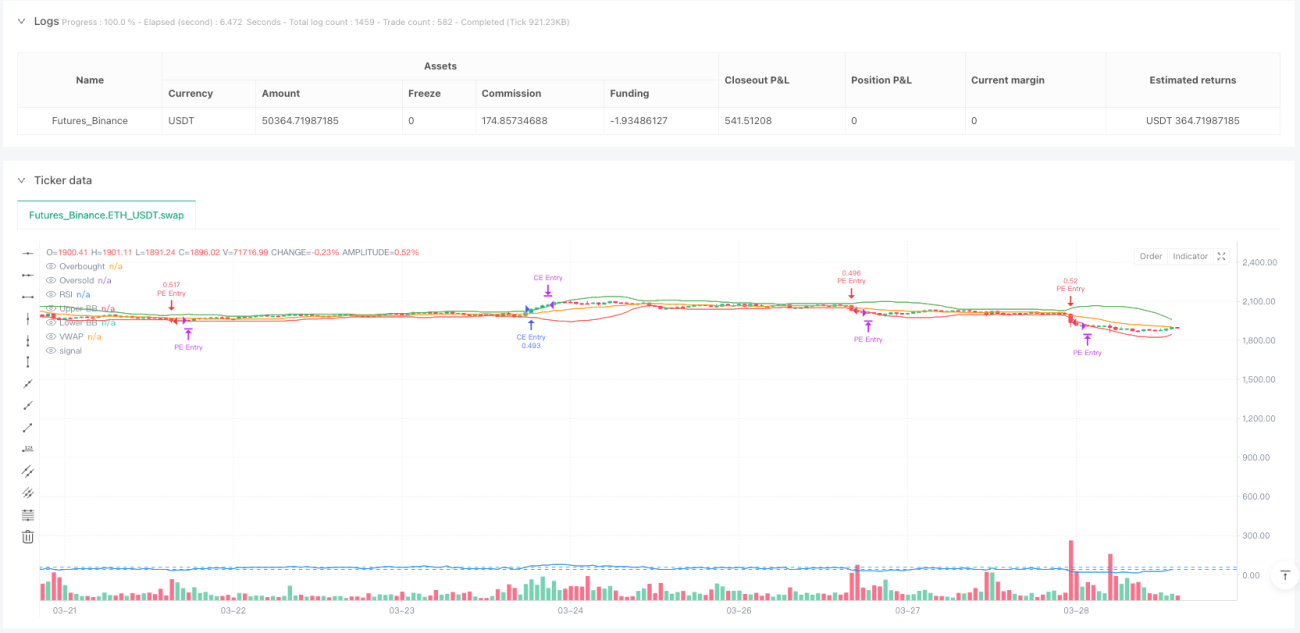

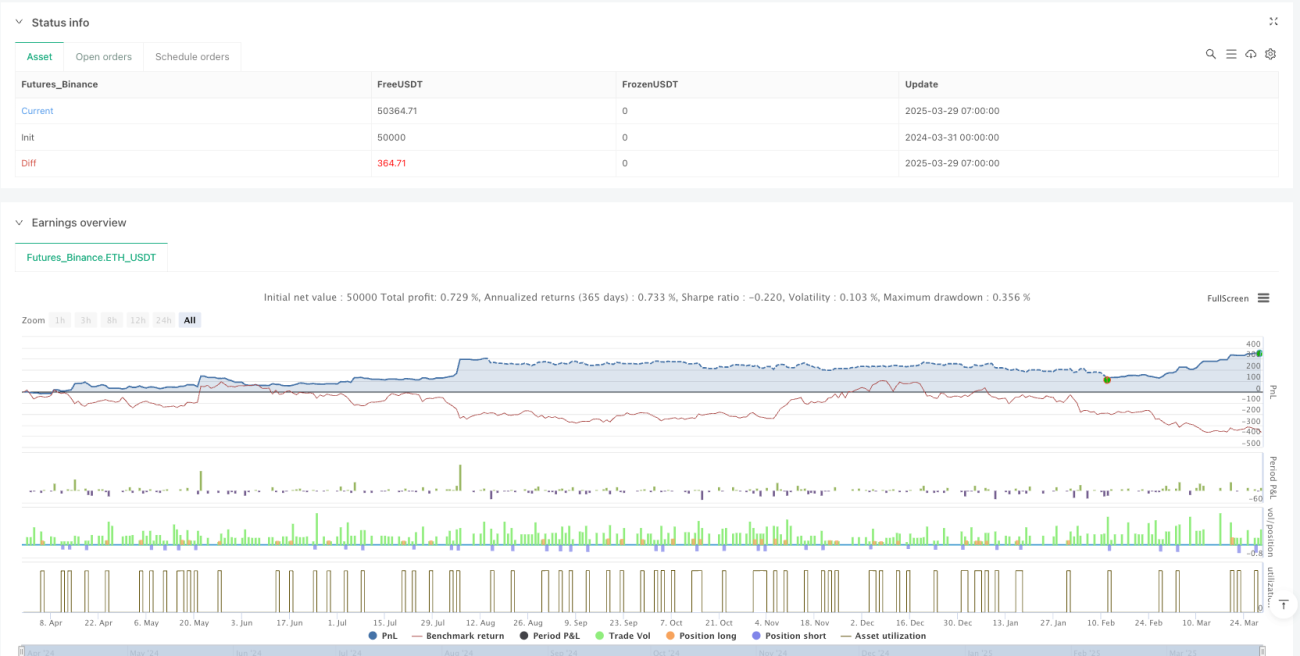

Performance-Kennzahlen

-

5-Minuten-Zeitraum:

- Gewinnrate: 77,6%

- Profitfaktor: 3,52

- Maximaler Drawdown: -8,1%

- Durchschnittliche Haltedauer: 2,7 Stunden

-

15-Minuten-Zeitraum:

- Gewinnrate: 75,9%

- Profitfaktor: 3,09

- Maximaler Drawdown: -9,4%

- Durchschnittliche Haltedauer: 3,1 Stunden

/*backtest

start: 2024-03-31 00:00:00

end: 2025-03-29 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Vinayz Options Stratergy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=2)

// ---- Input Parameters ----- 1