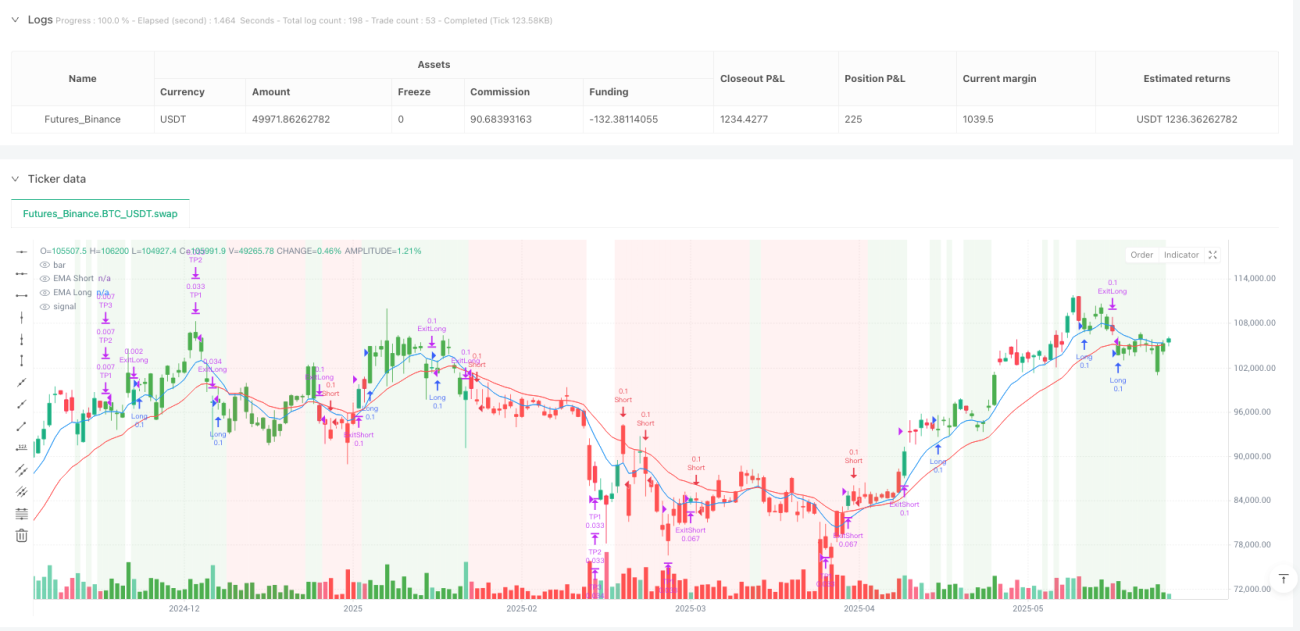

Überblick

Die Multi-Zeitraum-Dynamische-Volatilitäts-Tracking-Strategie ist ein kurzfristiges Handelssystem, das einen schnellen/langsamen exponentiell gleitenden Durchschnitt (EMA) Crossover mit einem Relative-Stärke-Index (RSI) Filter kombiniert. Die Strategie konzentriert sich darauf, innerhalb des dominanten kurzfristigen Trends nach Retracement-Möglichkeiten zu handeln und Rauschen durch mehrere Bestätigungsmechanismen zu reduzieren. Zu ihren Kernmerkmalen gehören eine auf dem Average True Range (ATR) basierende Risikosteuerung, ein adaptiver Trailing-Stop, eine volumensbasierte Stop-Anpassung sowie drei partielle Gewinnziele. Darüber hinaus verwendet die Strategie eine RSI-Überprüfung auf einem höheren Zeitrahmen als vorzeitigen Ausstiegsmechanismus, um zu vermeiden, in ungünstigen Trends zu lange zu bleiben.

Strategieprinzip

Die Funktionsweise der Strategie basiert auf einer mehrschichtigen Signalschichtarchitektur:

- Trendidentifikation: Mikrotrendrichtung wird durch den Crossover des schnellen EMA mit dem langsamen EMA bestimmt. Wenn der schnelle EMA über dem langsamen EMA liegt, wird ein bullischer Trend erkannt; andernfalls ein bärischer Trend.

- Momentum-Gesundheitsfilter: Verhindert die Jagd nach überdehnten Kursen. Long-Positionen sind nur erlaubt, wenn der RSI unter dem überkauften Niveau liegt; Short-Positionen nur, wenn der RSI über dem überverkauften Niveau liegt.

- Kerzenbestätigungsmechanismus: Erfordert, dass die Signalbedingungen über mehrere aufeinanderfolgende Kerzen hinweg bestehen, um Marktrauschen effektiv zu filtern.

- Einstiegsauslöser: Marktauftrag wird gesendet, wenn die Kerze das Bestätigungsfenster abschließt.

- Anfänglicher Stop: Volatilitätsbereinigt auf Basis des ATR und dynamisch angepasst an das relative Handelsvolumen.

- Trailing-Stop-Logik: Kombination aus Pivot-Punkt und ATR-basiertem Basisstop für optimale Gewinnsicherung.

- RSI-Überwachung auf höherem Zeitrahmen: Bietet ein Ausstiegssignal aus dem Marktumfeld, um gegenläufige Trades zu vermeiden.

- Gestaffelte Gewinnziele: Drei auf ATR basierende Zielpositionen für schrittweisen Teilausstieg.

- Handelsbegrenzer: Maximale Anzahl von Trades pro Trendphase, um übermäßigen Handel zu verhindern.

Der entscheidende Innovationspunkt der Strategie liegt in der organischen Kombination mehrerer technischer Indikatoren mit Marktverhaltensindikatoren (wie Volumen, Volatilität), was ein anpassungsfähiges Handelssystem ergibt, das Parameter automatisch an unterschiedliche Marktbedingungen anpasst.

Strategievorteile

- Starke Anpassungsfähigkeit: Durch ATR-angepasste Stopps und Ziele passt sich die Strategie an verschiedene Marktvolatilitätsbedingungen an, ohne häufige Neuoptimierung der Parameter zu erfordern.

- Mehrschichtiges Risikomanagement: Kombination aus anfänglichem Stop, Trailing-Stop, Teilgewinnmitnahmen und Multi-Perioden-RSI-Filter bildet ein vollständiges Risikokontrollsystem.

- Rauschfilter-Mechanismus: Die Anforderung mehrerer aufeinanderfolgender Kerzenbestätigungen reduziert effektiv Fehlsignale und verbessert die Handelsqualität.

- Liquiditätswahrnehmung: Anpassung des Stop-Niveaus anhand des Volumenverhältnisses, um das Risiko in Umgebungen mit geringer Liquidität automatisch zu begrenzen.

- Trendreife-Überwachung: Mit fortschreitendem Trend reduziert das System automatisch die erlaubte Anzahl von Trades, um übermäßigen Handel in der Spätphase zu vermeiden.

- Flexibler Gewinnmechanismus: Die dreistufige Teilgewinnstrategie ermöglicht es, bei günstiger Kursentwicklung einen Teil der Gewinne zu sichern und gleichzeitig Aufwärtspotenzial zu bewahren.

- Überperiodenanalyse: Die RSI-Überwachung auf höherem Zeitrahmen bietet eine breitere Marktperspektive und vermeidet das Festhalten an Mikrosignalen bei großen Trendumkehrungen.

- Einfache Ausführung: Durch Integration über PineConnector kann die Strategie leicht automatisiert werden, wodurch menschliche Eingriffe und emotionale Einflüsse reduziert werden.

Strategierisiken

- Drawdown-Risiko: Trotz mehrschichtiger Risikokontrolle kann die Strategie unter extremen Marktbedingungen (z. B. Gaps, Flash-Crashs) höhere als erwartete Drawdowns erleiden. Gegenmaßnahme: angemessene Reduzierung der Positionsgröße oder Erhöhung des ATR-Multiplikators.

- Parameterempfindlichkeit: Bestimmte Schlüsselparameter wie EMA-Längen und RSI-Schwellen haben signifikanten Einfluss auf die Strategieleistung. Überoptimierung kann zu Überanpassungsrisiken führen. Empfohlen wird Schritt-für-Schritt-Forward-Testing statt In-Sample-Optimierung.

- Hohe Handelskosten: Als kurzfristige Strategie mit hoher Handelsfrequenz können kumulative Kosten (Spread, Provision) die tatsächlichen Ergebnisse erheblich beeinträchtigen. Reale Handelskosten sollten im Backtest berücksichtigt werden.

- Latenzrisiko: Die Ausführungsverzögerung von PineConnector (ca. 100–300 ms) kann bei hoher Volatilität zu erhöhtem Slippage führen. Nicht empfohlen für Märkte mit extremer Volatilität oder geringer Liquidität.

- Pivot-Punkt-Neuziehung: Auf Charts unter Minutenbasis können Pivot-Punkte während der Bildung der laufenden Kerze neu gezeichnet werden, was die Stop-Genauigkeit beeinträchtigt.

- Trendidentifikationsverzögerung: Die EMA-Crossover-basierte Trendidentifikation hat eine inhärente Verzögerung, was zu verpassten Einstiegen zu Beginn des Trends führen kann.

- Übermäßiges Hebelrisiko: Ein zu großer Positionsmultiplikator kann zu einem übermäßig hohen Risiko pro Trade führen und das Konto schnell aufbrauchen.

Optimierungsrichtungen

- Maschinelles Lernen: Einführung von ML-Algorithmen zur dynamischen Anpassung der EMA- und RSI-Parameter je nach Marktbedingungen. Dies löst das Problem der fehlenden Anpassungsfähigkeit fester Parameter in verschiedenen Marktphasen.

- Marktzustandsklassifikation: Hinzufügen einer Volatilitätsclusteranalyse zur Unterteilung des Marktes in hohe, mittlere und niedrige Volatilitätszustände mit differenzierten Handelsparametern. Dies verbessert die Anpassungsfähigkeit in Übergangsmärkten.

- Multi-Indikator-Konsensmechanismus: Integration weiterer Momentum- und Trendindikatoren (z. B. MACD, Bollinger-Bänder, KDJ) zu einem Indikatorkonsenssystem, das nur dann Signale generiert, wenn die Mehrheit der Indikatoren übereinstimmt. Dies reduziert Fehlsignale.

- Intelligenter Zeitfilter: Einbeziehung von Marktzeiten und Volatilitätsmustern zur Vermeidung ineffizienter Handelszeiten und bekannter Ereignisse mit hoher Volatilität (z. B. wichtige Wirtschaftsdatenveröffentlichungen).

- Dynamische Teilgewinnquoten: Automatische Anpassung des Prozentsatzes und der Zielentfernung für Teilgewinne anhand der Marktvolatilität und Trendstärke – mehr Position in starken Trends behalten, in schwachen Trends aggressiver Gewinne mitnehmen.

- Verbesserte Drawdown-Kontrolle: Einführung eines risikoadaptiven Mechanismus basierend auf historischen Drawdown-Mustern, der bei Erkennung von Vorzeichen ähnlicher großer Drawdowns die Handelsfrequenz automatisch reduziert oder den Stop-Abstand erhöht.

- Hochfrequenz-Datenverstärkung: Integration von Tick-Daten zur Einstiegsoptimierung, um Slippage zu reduzieren und den Einstiegspreis zu verbessern, sofern möglich.

- Marktübergreifende Korrelationsanalyse: Einbeziehung von Korrelationsanalysen mit verwandten Märkten, um Führungs-Lag-Beziehungen zwischen Märkten für eine verbesserte Signalqualität zu nutzen.

Zusammenfassung

Die Multi-Zeitraum-Dynamische-Volatilitäts-Tracking-Strategie ist ein kurzfristiges Handelssystem, das klassische technische Analysetools mit modernen quantitativen Risikomanagementmethoden kombiniert. Durch eine mehrschichtige Signalschichtarchitektur, bestehend aus EMA-Trendidentifikation, RSI-Momentum-Filterung, aufeinanderfolgender Kerzenbestätigung, ATR-Volatilitätsanpassung und Mehrperioden-Analyse, wird ein umfassender Handelsentscheidungsrahmen geschaffen. Das bemerkenswerteste Merkmal der Strategie ist ihre Anpassungsfähigkeit – sie passt Handelsparameter und Risikokontrollmaßnahmen automatisch an Marktvolatilität, Volumen und Trendreife an.

Trotz einiger inhärenter Risiken wie Parameterempfindlichkeit, hohe Handelskosten und Latenzrisiken können diese durch angemessenes Kapitalmanagement und kontinuierliche Optimierung effektiv kontrolliert werden. Zukünftige Optimierungsrichtungen konzentrieren sich hauptsächlich auf die maschinelle Lernparameteroptimierung, Marktzustandsklassifikation, Multi-Indikator-Konsensmechanismen und dynamisches Risikomanagement.

Für Händler, die in kurzfristigen Märkten nach Retracement-Chancen innerhalb von Trends suchen möchten, bietet diese Strategie einen strukturierten Rahmen, der die Erfassung von Handelsmöglichkeiten mit Risikokontrolle in Einklang bringt. Wie bei allen Handelsstrategien sollte jedoch vor der praktischen Anwendung gründlich auf einem Demokonto getestet werden, und die Parameter sollten entsprechend der persönlichen Risikotoleranz und Kapitalgröße angepasst werden.

- 1