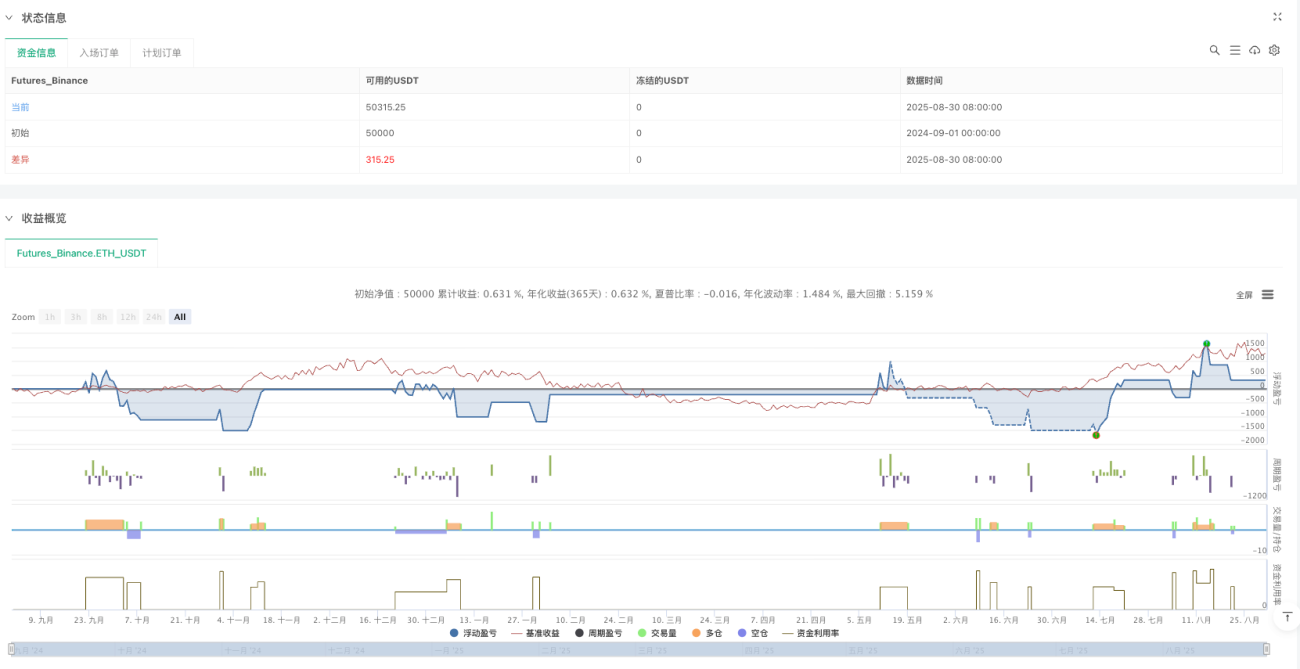

🎯 Wie leistungsstark ist diese Strategie wirklich?

Wusstest du, dass 90 % der Händler auf dem Markt in steigende Kurse einsteigen und fallende verkaufen, doch die wahren Profis suchen nach der „Preislücke“? Dieses Advanced FVG Strategy Pro+ ist die Superwaffe, um genau diese mysteriösen Lücken zu fangen 🚀

FVG (Fair Value Gap) bezeichnet im einfachen Sinne den „leeren Bereich“, der entsteht, wenn der Preis springt – wie beim Überspringen einer Pfütze beim Gehen. Irgendwann kommt der Preis zurück, um die Lücke zu schließen. Diese Strategie lauert zum optimalen Zeitpunkt am „Rand der Lücke“ und wartet darauf, dass der Fisch anbeißt!

💡 Wichtige Punkte! Drei Kern-Hightech-Features

1. Multi-Zeitrahmen-Analyse 📊

Keine Beschränkung mehr auf einen einzigen Zeitraum! Die Strategie kann auf einem 5-Minuten-Chart ausgeführt werden, nutzt aber FVG-Signale vom 1-Stunden-Chart. Das ist, als würde man ferne Berge durch ein Teleskop betrachten und Details mit einer Lupe – ein umfassenderes Blickfeld!

2. IIR-Trendfilter 🌊

Das ist kein gewöhnlicher gleitender Durchschnitt! Der IIR-Tiefpassfilter auf Ingenieurniveau erkennt Trendrichtungen präzise. Stell dir vor, das ist wie ein Trendradar für deinen Handel – du handelst nur mit dem Rückenwind!

3. Intelligentes Risikomanagement 🛡️

Unterstützt sowohl prozentuale als auch feste Beträge für das Risiko, plus einen Mechanismus zum Schutz vor dem Knockout. Wie ein Auto mit Sicherheitsgurt und Airbag – doppelter Schutz für dein Konto!

🎪 Praktische Einsatzszenarien

Am besten geeignet für:

- Jagd nach Ausbruchsmöglichkeiten in Seitwärtsmärkten ⚡

- Einstiegspunkte bei Pullbacks in Trendmärkten 📈

- Präzise Schüsse nahe wichtiger Unterstützungs- und Widerstandszonen 🎯

Fehlervermeidungs-Guide:

- Pausiere bei wichtigen Nachrichten

- Sei vorsichtig bei kleinen Coin-Paaren mit geringer Liquidität

- Passe die Risikoparameter an die Marktvolatilität an

🚀 Warum diese Strategie wählen?

Herkömmliche Strategien verpassen entweder Chancen aufgrund zu weniger Signale oder werden von Fehlausbrüchen hereingelegt – zu viele Signale. Diese Strategie setzt durch mehrfache Filtermechanismen auf „Weniger ist mehr“ – präzise Schläge!

Und das Beste: Alle Parameter sind individuell einstellbar. Wie ein Tontechniker, der den Sound justiert, kannst du je nach Marktumfeld den optimalen Handelsrhythmus „einstellen“ 🎵

Denk daran: Eine gute Strategie bedeutet nicht, jeden Tag zu handeln, sondern dann zuzuschlagen, wenn die Wahrscheinlichkeit am höchsten ist! Das ist die Magie der FVG-Strategie ✨

- 1