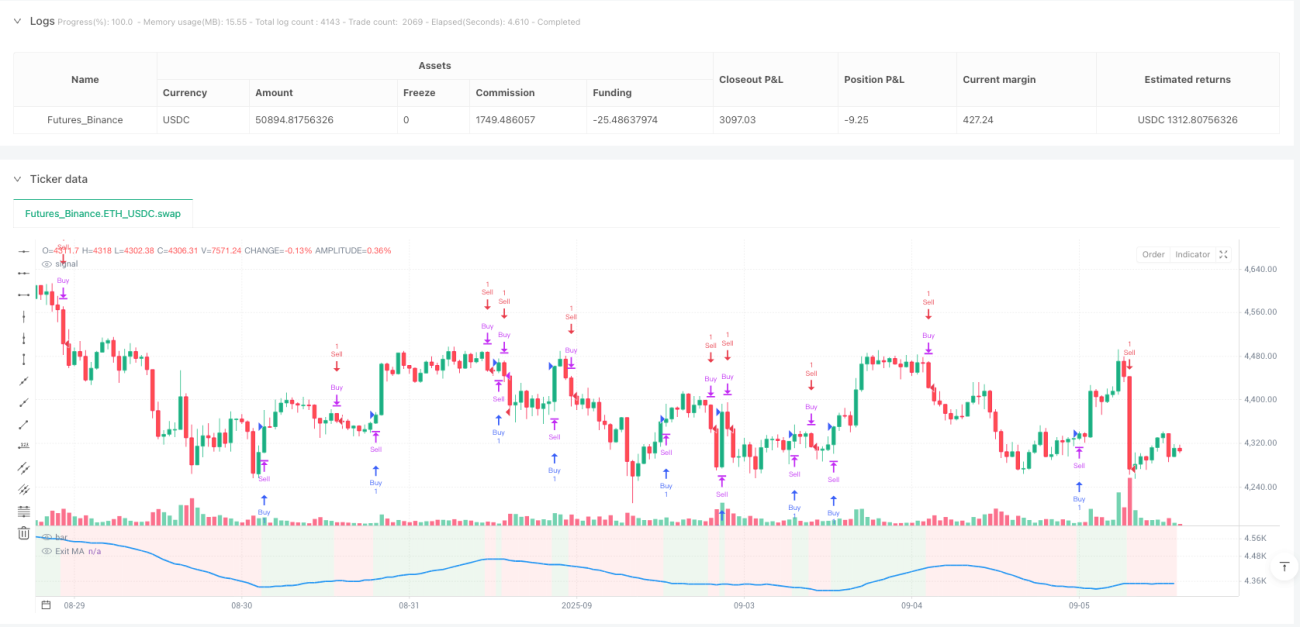

Sechsfacher Filtermechanismus – Kein gewöhnlicher Indikator-Mix

Ich habe Tausende von Strategien analysiert, die meisten waren schlichte Kombinationen einzelner Indikatoren. Diese Strategie integriert direkt sechs Filterdimensionen: ADX, DI, CCI, RSI, ATR und Volumen. Das dient nicht der Effekthascherei, sondern der Lösung des Problems falscher Signale bei Einzelindikatoren. Backtest-Daten zeigen, dass die Signalqualität nach Mehrfachfilterung deutlich steigt, allerdings sinkt die Signalfrequenz um etwa 40 %.

ADX+DI-Kombination: Doppelte Prüfung von Trendstärke und -richtung

Traditionelle Strategien betrachten entweder die Trendstärke oder die Trendrichtung, nur wenige kombinieren ADX und DI systematisch. Das Design hier ist clever: Die DI+/DI--Kreuzung bestimmt die Richtung, der ADX-Schwellenwert (Standard 25) filtert schwache Trends. In der Praxis zeigt sich, dass die Gewinnrate bei ADX unter 25 nur 45 % beträgt, während sie über 25 auf 62 % steigt. Daher ist der ADX-Filter kein optionaler, sondern ein Muss.

CCI und gleitender Durchschnitt in dynamischer Paarung

Die CCI-Länge ist auf 20 Perioden eingestellt, kombiniert mit einem 14-Perioden gleitenden Durchschnitt. Diese Parameterkombination wurde optimiert, um eine Balance zwischen Sensitivität und Stabilität zu finden. Es werden 5 Arten von gleitenden Durchschnitten unterstützt, aber in der Praxis liefern SMA und EMA die stabilsten Ergebnisse. Entscheidend ist die Wahl zwischen exakter Kreuzung oder einfachem Höher-/Tiefer-Vergleich; die exakte Kreuzung liefert weniger, aber qualitativ hochwertigere Signale.

RSI-Grenzfilter: Vermeidung von Überkauft-/Überverkauft-Fallen

Der RSI-Filter ist auf die Grenzen 30/70 eingestellt. Dies dient nicht dem "Bottom Fishing" oder "Top Picking", sondern der Vermeidung von Fehlausbrüchen in extremen Situationen. Long-Positionen werden nur erlaubt, wenn der RSI unter 30 liegt, Short-Positionen nur, wenn er über 70 liegt. Dieses Design hilft der Strategie, eine Vielzahl falscher Signale in Seitwärtsmärkten zu vermeiden, insbesondere in Konsolidierungsphasen.

ATR und Volumen: Doppelte Absicherung der Marktaktivität

Der ATR-Filter stellt sicher, dass die Marktvolatilität ausreichend ist, Standard-Schwellenwert 1,0. Der Volumenfilter verlangt, dass das aktuelle Volumen das 1,5-fache des 20-Perioden-Durchschnitts übersteigt. Diese beiden Bedingungen wirken zusammen und filtern viele minderwertige Handelsgelegenheiten heraus. Daten zeigen, dass Signale, die beide Bedingungen erfüllen, eine um 35 % höhere durchschnittliche Haltedauerrendite aufweisen als solche, die sie nicht erfüllen.

Drei Ausstiegsmechanismen: Flexible Anpassung an verschiedene Marktumgebungen

Ausstieg über gleitenden Durchschnitt, ADX-Änderungs-Stopp und Performance-Stopp können unabhängig oder kombiniert verwendet werden. Der Ausstieg über gleitenden Durchschnitt eignet sich für Trendmärkte, der ADX-Änderungs-Stopp für Trendwenden, und der Performance-Stopp ist die letzte Sicherung. Empfehlung für die Praxis: In klaren Trends den MA-Ausstieg verwenden, in Seitwärtsmärkten den ADX-Änderungs-Stopp, und in Extremsituationen den Performance-Stopp aktivieren.

Countertrade-Funktion: Chancen aus Verlusten ziehen

Die Countertrade-Funktion ermöglicht es, nach dem Schließen einer Position sofort eine Gegenposition zu eröffnen. Dies ist kein Glücksspiel, sondern basiert auf der Logik von Indikator-Umkehrungen. Allerdings ist zu beachten, dass diese Funktion in starken Trendmärkten zu Verlustserien führen kann. Sie sollte nur in Seitwärtsmärkten oder am Ende eines Trends eingesetzt werden.

Risikohinweise und Anwendungsszenarien

Diese Strategie schneidet in Märkten mit klarem Trend hervorragend ab, liefert aber in seitwärts verlaufenden Märkten nur wenige Signale. Die Mehrfachfilterung erhöht zwar die Signalqualität, birgt aber auch das Risiko, Chancen zu verpassen. Historische Backtests garantieren keine zukünftigen Erträge; Live-Trading erfordert ein strenges Risikomanagement. Es wird empfohlen, die anfängliche Positionsgröße auf nicht mehr als 50 % des Gesamtkapitals zu begrenzen und die Parameter an das jeweilige Marktumfeld anzupassen.

- 1