Swing-Erkennungs-Bewertungsstrategie

Dies ist keine gewöhnliche Swing-Strategie, sondern ein präzises Sniper-System mit KI-Bewertung

Wo liegt das Problem traditioneller Swing-Strategien? Zu viele Signale, uneinheitliche Qualität, häufige Fehlausbrüche. Diese Strategie löst den Schmerzpunkt direkt: Jedes Signal erhält eine Qualitätsbewertung von 1 bis 5 Punkten, es werden nur Signale mit 4 Punkten oder mehr gehandelt.

Die Kernlogik ist einfach und direkt: Erkennen von Higher Lows und Lower Highs, dann Bewertung des Signals anhand von 4 Dimensionen. Erst ab mindestens 4 Punkten wird eröffnet – das filtert sofort 80 % der schlechten Signale heraus.

Warum ist ein 5‑dimensionales Bewertungssystem besser als ein einzelner Indikator?

1 Punkt Basiswert: Bestätigung der Swing-Formation

+1 Punkt Volumenbestätigung: Volumen über 1,2-fachem 20-Perioden-Durchschnitt – signalisiert Zustimmung des Kapitals

+1 Punkt RSI-Position: RSI im Bereich 30-70 – vermeidet überkaufte/überverkaufte Fehlsignale

+1 Punkt Kerzenkörper: Körperanteil über 60 % – schließt zögerliche Formationen wie Dojis aus

+1 Punkt Trendausrichtung: Preis, MA20 und MA50 zeigen alle in dieselbe Richtung

Ergebnis: Signale mit 5 Punkten haben die höchste Trefferquote, Signale ab 4 Punkten sind handelbar, Signale mit 3 Punkten oder weniger werden ignoriert.

Stop-Loss-Design: Extremwerte der letzten 10 Perioden, kein willkürlicher ATR

Die Stop-Loss-Logik ist klar:

- Long-Stop = Tiefstpunkt der letzten 10 Kerzen

- Short-Stop = Höchstpunkt der letzten 10 Kerzen

Warum 10 Perioden? Da Swing-Strategien kurzfristige Umkehrungen nutzen, bieten 10 Perioden dem Kurs genügend Atemraum, ohne dass der Abstand zu groß wird. Dies entspricht der Marktstruktur besser als ein fester ATR-Multiplikator.

Fehlgeschlagene Signale sind ebenfalls Handelschancen

Die Strategie erkennt auch „gescheiterte Swings":

- Gescheiterte Higher Lows: Ein Higher Low wird gebildet, dann aber unterschritten

- Gescheiterte Lower Highs: Ein Lower High wird gebildet, dann aber überschritten

Diese Fehlschläge deuten oft auf eine Trendbeschleunigung hin und sind ideale Gelegenheiten für Gegengeschäfte.

Aufeinanderfolgende Signale = Trendbestätigung

Wenn bei zwei aufeinanderfolgenden Kerzen gleichgerichtete Bestätigungssignale auftreten, wird dies mit einem Diamant-Symbol angezeigt. Dies bedeutet in der Regel:

- Aufeinanderfolgend bullisch: Aufwärtstrend etabliert

- Aufeinanderfolgend bärisch: Abwärtstrend etabliert

Die Trefferquote aufeinanderfolgender Signale ist in der Regel 15‑20 % höher als bei Einzelsignalen.

Anwendungsszenario: Seitwärtsmarkt mit bullischem/bärischem Bias

Beste Umgebung für die Performance:

- Märkte mit klarem Trend, aber häufigen Rücksetzern

- Moderate Volatilität (weder extrem ruhig noch extrem wild)

- Relativ stabile Volumenwerte

Zu vermeidende Szenarien:

- Einseitige starke Kursausschläge (Swing-Signale werden häufig durchbrochen)

- Seitwärtsmärkte mit extrem niedriger Volatilität (seltene Signale und schlechte Qualität)

- Nischenprodukte mit sehr instabilem Volumen

Risikohinweis: Historische Backtests sind kein Garant für zukünftige Gewinne

Klare Risiken:

- Die Strategie kann zu Verlustserien führen, insbesondere in Trendwechselphasen

- Signale mit 4+ Punkten sind zwar qualitativ hochwertig, haben aber dennoch eine Fehlerrate von 30‑40 %

- Der Stop-Loss ist relativ großzügig, einzelne Verluste können erheblich sein

- Die Performance variiert stark je nach Marktumfeld

Empfehlung zum Geldmanagement: Einzelrisiko nicht über 2 % des Kontos; nach 3 aufeinanderfolgenden Verlusten pausieren und das Marktumfeld neu bewerten.

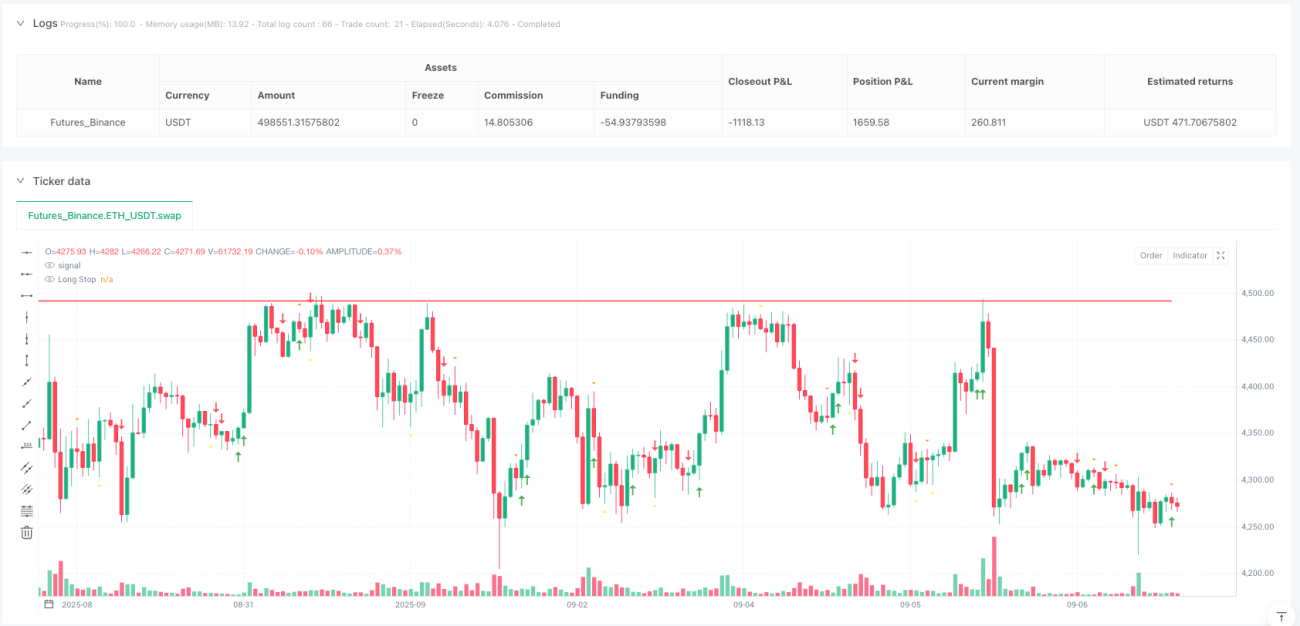

/*backtest

start: 2024-09-09 00:00:00

end: 2025-09-07 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT","balance":500000}]

*/

//@version=6

strategy("Higher Lows, Lower Highs & Failures with Signal Quality Scoring", overlay=true)

// --- Higher Low detection ---- 1