Trendstufen-Mittelungsstrategie: Wie man sich elegant „entspannt“, wenn der Markt seitwärts tendiert?

Warum scheitern traditionelle Trendfolgestrategien in Seitwärtsmärkten regelmäßig?

Als quantitativer Trader werde ich oft gefragt: Warum erleiden Strategien, die in Trendmärkten hervorragend abschneiden, in Seitwärtsbewegungen große Rückschläge?

Die Antwort ist eigentlich einfach: Die meisten Trendfolgestrategien leiden unter einer "Trend-Zwangstörung" – sie versuchen stets, in jedem Marktumfeld mit hoher Frequenz zu handeln, ignorieren jedoch die grundlegende Tatsache: 70 % der Zeit befindet sich der Markt in einer Seitwärtsbewegung.

Die heute zu analysierende "Trend-Stufen-Durchschnittsstrategie" bietet genau für diesen Schmerzpunkt eine interessante Lösung: In Trendmärkten aktiv folgen, in Seitwärtsmärkten elegant stillhalten.

Was ist der "Stufendurchschnitt"? Wie definiert dieses Konzept die Trendfolge neu?

Herkömmliche gleitende Durchschnittsstrategien haben einen fatalen Fehler: Sie ändern sich ständig. Egal, ob der Markt einen starken Trend oder eine Seitwärtsbewegung aufweist – der gleitende Durchschnitt passt sich kontinuierlich an die Kursbewegungen an, was zu vielen Fehlsignalen führt.

Der Kern des "Stufendurchschnitts" ist: Den gleitenden Durchschnitt unter bestimmten Bedingungen "einfrieren".

Die konkrete Implementierungslogik:

-

Trendzustandserkennung: Bestimmung der Trendstärke über den ADX-Indikator

- ADX > 25: Starker Trendmarkt

- Steigung des gleitenden Durchschnitts < 0,3 %: Seitwärtsmarkt

-

Dynamischer Wechsel des gleitenden Durchschnitts:

- Starker Trend: Normale Verfolgung des EMA(21)

- Seitwärts: Der gleitende Durchschnitt wird auf horizontalem Niveau "eingefroren" und bildet Unterstützung/Widerstand

Das Raffinierte an diesem Design: Die Strategie zeigt in verschiedenen Marktumgebungen unterschiedliche "Persönlichkeiten" – im Trend sensibel, in Seitwärtsbewegungen stabil.

Wie wird das "Trend-Capture"-System umgesetzt?

Neben dem grundlegenden Stufendurchschnittsmechanismus integriert die Strategie ein "Trend-Capture"-Modul, das ich für den innovativsten Teil halte:

Schnelle Umkehrmechanik:

- Wenn ein gegensätzlicher starker Trend nach dem Schließen einer Position auftritt

- Schnelle Eröffnung einer neuen Position innerhalb von 3 Perioden

- Bedingung: ADX > 30 und DI+-DI- Differenz > 10

Dieses Design löst ein wichtiges Problem traditioneller Strategien: Wie man Positionen zu Beginn einer Trendumkehr schnell anpasst.

Stellen Sie sich vor: Sie haben gerade eine Long-Position wegen eines Stopp-Losses geschlossen, und der Markt zeigt sofort einen starken Abwärtstrend. Traditionelle Strategien müssten auf ein neues Bestätigungssignal warten, aber dieses "Trend-Capture"-System kann innerhalb von 3 Perioden schnell eine Short-Position eröffnen.

Risikomanagement: Warum zwischen Marktzuständen unterscheiden?

Am lehrreichsten an dieser Strategie ist ihr differenziertes Risikomanagement:

Risikokontrolle im Seitwärtsmarkt:

- Stopp-Loss wird nahe dem Stufendurchschnitt angepasst

- ATR-Multiplikator verringern, Stopps enger setzen

- Ziele konservativer festlegen

Risikokontrolle im Trendmarkt:

- Standard-ATR-Multiplikator für Stopp-Loss verwenden

- Stufenweise Trailing-Stopps aktivieren

- Größere Kursspannen zulassen

Dieses Design spiegelt eine wichtige Handelsphilosophie wider: Verschiedene Marktumgebungen erfordern unterschiedliche Risikoneigungen. In Seitwärtsmärkten sollten wir vorsichtiger sein, in Trendmärkten müssen wir den Gewinnen mehr Raum zum Laufen geben.

Stufenweiser Trailing-Stopp: Wie schützt man Gewinne und folgt dem Trend gleichzeitig?

Herkömmliche Trailing-Stopps sind oft zu mechanisch – entweder zu eng, was zu vorzeitigem Ausstieg führt, oder zu locker, was Gewinne nicht effektiv schützt. Der stufenweise Trailing-Stopp dieser Strategie bietet eine intelligentere Lösung:

Stufen-Setup-Logik:

- Dynamische Berechnung des Stufenabstands auf Basis des ATR

- Maximal 5 Stufen

- Bei jedem Durchbrechen einer Stufe wird der Stopp-Loss entsprechend nach oben angepasst

Der Vorteil dieses Designs: Es schützt Gewinne und lässt dem Trend gleichzeitig genügend Raum zur Entwicklung.

Worauf ist in der praktischen Anwendung zu achten?

Basierend auf meiner Live-Erfahrung sind bei dieser Strategie folgende Punkte zu beachten:

-

Parameter-Optimierungsfallen: Übertreiben Sie es nicht mit der Optimierung des ADX-Schwellenwerts. Werte zwischen 25 und 30 sind in den meisten Märkten stabil.

-

Marktanpassung: Die Strategie eignet sich besser für Märkte mit mittlerer Volatilität. In extrem volatilen Umgebungen müssen möglicherweise die ATR-Multiplikatoren angepasst werden.

-

Geldmanagement: Einzelpositionen sollten nicht mehr als 10 % des Gesamtkapitals betragen, insbesondere bei aktivierter Trend-Capture-Funktion.

-

Backtest-Fallen: Achten Sie besonders auf Slippage und Transaktionskosten, insbesondere bei häufigem Handel in Seitwärtsmärkten.

Wo liegt der innovative Wert dieser Strategie?

Aus Sicht der Entwicklung quantitativer Strategien repräsentiert diese Strategie eine wichtige Evolutionsrichtung: Vom eindimensionalen Denken zur multi-zustandsadaptiven Anpassung.

Traditionelle Strategien versuchen oft, mit einer festen Logik auf alle Marktsituationen zu reagieren, während diese Strategie die Weisheit des "standortangepassten Handelns" zeigt:

- In Trendmärkten verhält sie sich wie ein aggressiver Trendfolger

- In Seitwärtsmärkten verhält sie sich wie ein konservativer Range-Trader

Dieser Designansatz kann für Strategieentwickler von großer Bedeutung sein: Wir sollten Strategien mit "Marktwahrnehmung" ausstatten, anstatt blind feste Logiken auszuführen.

Abschließend sei betont, dass keine Strategie perfekt ist. Diese Stufendurchschnittsstrategie ist zwar theoretisch elegant, muss aber in der praktischen Anwendung je nach spezifischem Marktumfeld und persönlicher Risikoneigung angepasst werden. Denken Sie daran: Die beste Strategie ist immer die, die am besten zu Ihnen passt.

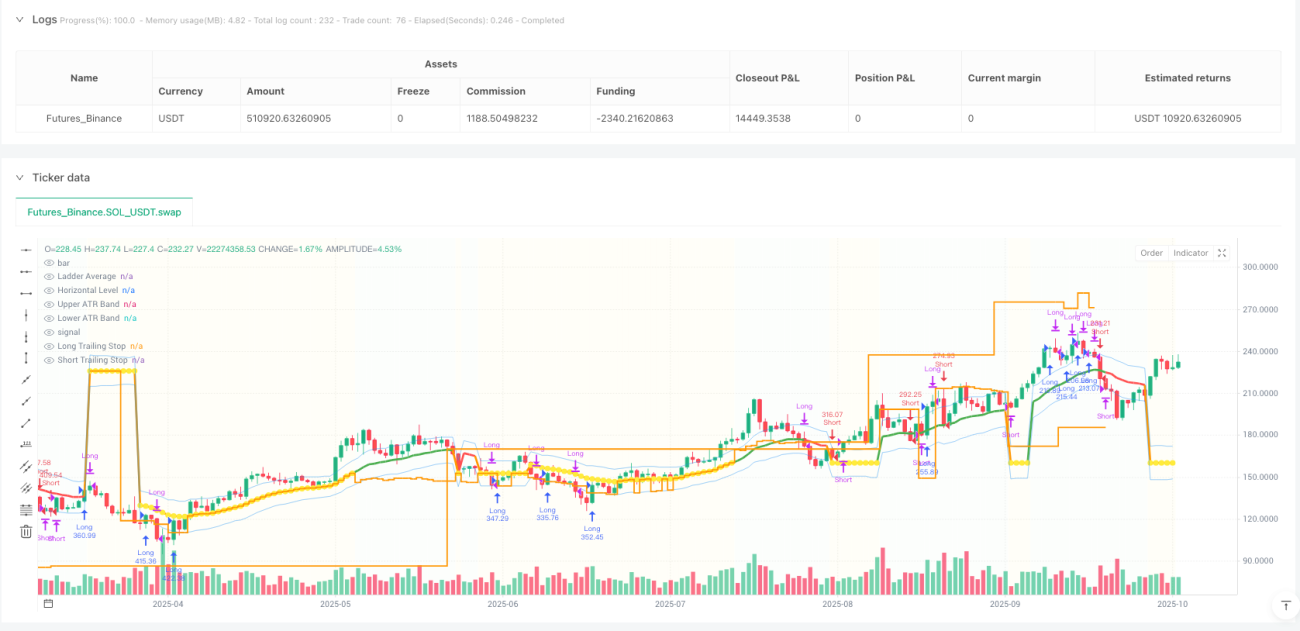

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1