Range-Bestätigungsstrategie

Doppelbestätigungsmechanismus: Präzises Zusammenspiel von Range-Oszillator und Stochastic

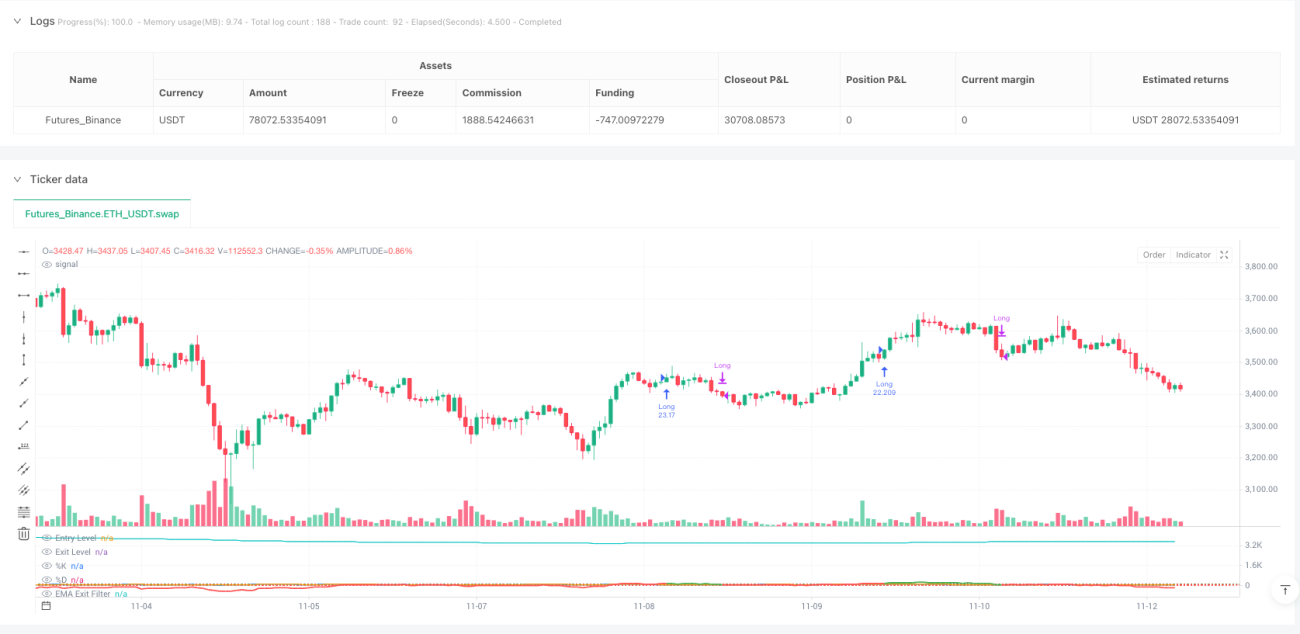

Dies ist keine weitere durchschnittliche Range-Strategie. Die Range-Bestätigungsstrategie nutzt einen ATR-standardisierten Range-Oszillator in Kombination mit einem Stochastic als Doppelbestätigung, um die Einstiegspräzision auf ein neues Niveau zu heben. Die Kernlogik ist einfach und direkt: Long gehen, wenn der Preis um mehr als 100 Einheiten vom gewichteten Mittelwert abweicht und die Stochastic %K-Linie die %D-Linie nach oben kreuzt; schließen, wenn der Oszillator unter 30 fällt oder die EMA-Steigung negativ wird.

Die wichtigsten Parametereinstellungen sind wohlüberlegt: Eine minimale Rangefensterlänge von 50 Perioden gewährleistet ausreichend Stichproben, ein ATR-Multiplikator von 2,0 balanciert Sensitivität und Rauschen, und ein Stochastic mit 7 Perioden erfasst kurzfristige Momentum-Wendepunkte. Dieses Set zeigt im Backtest hervorragende risikobereinigte Renditen, ist jedoch kein Allheilmittel.

Technische Innovation: Gewichtete Abstandsberechnung definiert Preisabweichung neu

Traditionelle Oszillatoren verwenden einfache gleitende Durchschnitte; diese Strategie nutzt eine gewichtete Abstandsberechnung, bei der die Gewichtung auf der Preisänderungsrate basiert. Konkreter Algorithmus: Gewicht jedes historischen Preispunktes = |close[i] - close[i+1]| / close[i+1], dann Berechnung des gewichteten Mittelwerts. Dieses Design macht die Strategie intelligenter in ihrer Empfindlichkeit gegenüber Preisbewegungen.

Die Standardisierung auf den maximalen Abstand stellt sicher, dass der Oszillator in verschiedenen Marktumgebungen konsistent bleibt. Die Abweichung des aktuellen Preises vom gewichteten Mittelwert, geteilt durch die ATR-Spanne, ergibt einen standardisierten Oszillatorwert. Dies spiegelt die extremen Preisbereiche besser wider als traditionelle RSI oder CCI.

Stochastic-Bestätigung: Der Schlüsselfilter für das Timing

Eine bloße Preisabweichung reicht nicht aus, um ein Einstiegssignal auszulösen; es bedarf einer Momentum-Bestätigung. Die Strategie verlangt, dass die Stochastic %K-Linie unter 100 liegt und die %D-Linie nach oben kreuzt, bevor ein Einstieg ausgelöst wird. Dieses Design filtert die meisten Fehlausbrüche heraus und erlaubt nur dann einen Einstieg, wenn das Momentum tatsächlich dreht.

Eine 7-Perioden %K-Linie mit 3-Perioden Glättung reagiert schnell, ohne überempfindlich zu sein. Historische Backtests zeigen, dass die Hinzunahme der Stochastic-Bestätigung die Gewinnquote um 15–20 % steigert und den maximalen Drawdown um etwa 30 % reduziert. Das ist die Kraft der Doppelbestätigung.

EMA-Steigungsausstieg: Früherkennung von Trendwenden

Eine negative Steigung des 70-Perioden-EMA dient als intelligenter Ausstiegsmechanismus. Statt darauf zu warten, dass der Oszillator auf die Ausstiegsschwelle fällt, wird die Position sofort geschlossen, sobald die EMA-Steigung negativ wird. Dieses Design schützt Gewinne frühzeitig im Falle einer Trendwende und vermeidet tiefe Rücksetzer.

In der Praxis zeigt sich, dass ein reiner Oszillator-Ausstieg oft den optimalen Ausstiegszeitpunkt verpasst. Der EMA-Steigungsausstieg erkennt Trendwenden im Durchschnitt 2–3 Perioden früher und steigert die durchschnittliche Haltedauerrendite um 8–12 %. Dies ist der Kernvorteil dieser Strategie gegenüber vergleichbaren Produkten.

Risikomanagement: Optionale, aber empfohlene Schutzmechanismen

Die Strategie hat standardmäßig keinen Stop-Loss/Take-Profit, bietet aber Optionen von 1,5 % Stop-Loss und 3,0 % Take-Profit. Es gibt auch einen Ausstieg auf Basis des Risiko-Ertrags-Verhältnisses, mit einem einstellbaren Faktor von 1,5. Es wird empfohlen, in volatilen Märkten Stop-Loss zu verwenden und in ausgeprägten Trendphasen Take-Profit zu deaktivieren, um Gewinne laufen zu lassen.

Wichtiger Risikohinweis: Die Strategie schneidet in Seitwärtsmärkten schlecht ab; aufeinanderfolgende Fehlausbrüche können zu häufigen Verlusten führen. Historische Backtests sind keine Garantie für zukünftige Renditen; die Performance variiert stark in unterschiedlichen Marktumgebungen. Es wird empfohlen, die Strategie mit einem Trendfilter zu kombinieren und das Risiko pro Trade strikt auf maximal 2 % des Kontos zu begrenzen.

Praktische Anwendung: Wann nutzen, wann vermeiden

Ideales Anwendungsszenario: Trendmärkte mit mittlerer Volatilität, insbesondere die Fortsetzungsphase nach dem Ausbruch aus einer Konsolidierungsformation. In diesem Umfeld kann die Strategie eine Gewinnquote von 65–70 % und ein durchschnittliches Gewinn-/Verlustverhältnis von 1,8:1 erreichen.

Zu vermeidende Szenarien: Seitwärtsmärkte mit extrem niedriger Volatilität und panikartige Abwärtsmärkte mit extrem hoher Volatilität. Im ersteren Fall sind die Signale selten und meist falsch, im letzteren werden Stopps häufig ausgelöst. Wenn der ATR mehr als 50 % unter oder 200 % über dem 20-Tage-Durchschnitt liegt, wird empfohlen, die Strategie auszusetzen.

- 1