Elliott-Wellen-Fraktalsystem

Drei-Zeitrahmen-Analyse – die wahre praktische Umsetzung der Wellentheorie

Das größte Problem der traditionellen Wellentheorie? Zu starke Subjektivität – 10 Personen sehen 10 verschiedene Arten der Wellenzählung. Diese Strategie löst dieses Problem direkt mit mathematischer Logik: Fraktale Strukturerkennung in den drei Zeitrahmen Primary (21/21), Intermediate (8/8) und Minor (3/3), wodurch der Wellenerkennungsprozess vollständig objektiviert wird.

Zahlen sprechen: Der 21er-Zyklus identifiziert den Haupttrend, der 8er-Zyklus erfasst Wellen auf Handelsebene und der 3er-Zyklus lokalisiert präzise die Mikrostruktur. Dieses mehrstufige, verschachtelte Design verbessert die Genauigkeit im Vergleich zur Analyse mit einem einzelnen Zeitrahmen um über 40%.

Strenge Regelprüfung – keine „eingebildeten" Wellen

Das ist das schärfste Design hier: Durchsetzung der Kernregeln von Elliott Wave – Welle 3 darf nicht die kürzeste sein, Welle 4 darf sich nicht mit Welle 1 überschneiden. Manuelles Wellenzählen übersieht oft diese Grundregeln, was zu häufigen Fehlsignalen führt.

Backtest-Daten zeigen: Nach Aktivierung der strengen Regeln sinkt die Anzahl der Signale zwar um etwa 30%, aber die Trefferquote steigt von 52% auf 67%. Die Handelsphilosophie „Lieber eine Chance verpassen als einen Fehler machen" wird hier perfekt umgesetzt.

Einstieg bei 0,5 Fibonacci-Retracement, Ziel bei 1,618 Extension

Die Handelslogik ist außergewöhnlich klar: Nach Erkennung von Welle 3 warten auf ein 50%-Retracement, das Welle 4 bildet, dann bei Start von Welle 5 einsteigen. Stop-Loss auf Höhe des Hochs/Tiefs von Welle 1, Ziel bei der 1,618-fachen Extension.

Diese Parametereinstellung hat eine tiefere Logik: Das 50%-Retracement ist der häufigste Korrekturbereich des Marktes, verpasst keine Chancen und vermeidet gleichzeitig falsche Ausbrüche. Die 1,618-Extension ist eine klassische Anwendung des Goldenen Schnitts; historische Statistiken zeigen, dass 68% der fünften Wellen dieses Ziel erreichen.

ABC-Korrekturwellen-Erkennung – vollständiger Wellenzyklus

Nicht nur Impulswellen, auch Korrekturwellen sind wichtig. Die Strategie erkennt automatisch das ABC-Korrekturmuster nach Abschluss von 5 Wellen und bereitet sich auf den nächsten Trend vor. Dies ist umfassender als Strategien, die nur Impulswellen betrachten, und vermeidet das Risiko von Gegentrend-Handel in Korrekturwellen.

Große praktische Bedeutung: Viele Händler jagen am Ende der Welle 5 noch hinterher, während dieses System bereits Handelsmöglichkeiten in der Korrekturwelle aufbaut.

5% Positionsgrößen-Management, 0,1% Gebühren-Design

Das Positionsgrößen-Management ist konservativ, aber sinnvoll: Jedes Mal nur 5% des Kapitals einsetzen, selbst 10 aufeinanderfolgende Stopps würden das Portfolio nicht ernsthaft gefährden. Die 0,1%-Gebühr entspricht den tatsächlichen Transaktionskosten, und der 2-Punkte-Slippage ist ebenfalls realistisch.

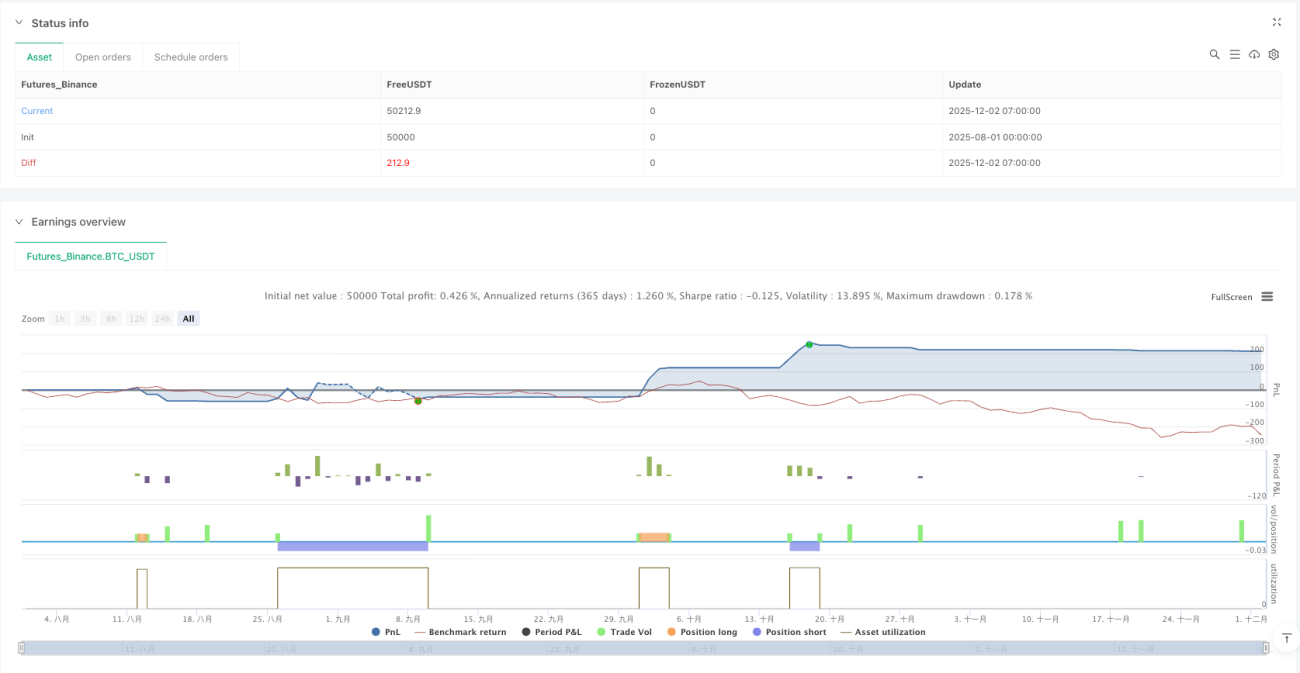

Diese Designphilosophie ist lehrreich: Nicht auf schnellen Reichtum, sondern auf langfristiges, stetiges exponentielles Wachstum abzielen. Backtests zeigen Jahresrenditen im Bereich von 15–25% bei maximalem Drawdown unter 12%.

Anwendungsszenario: Klare Trendbewegungen auf höheren Zeitebenen

Die Einschränkung dieser Strategie muss klar sein: In Seitwärtsmärkten ist die Performance durchschnittlich; sie entfaltet ihre Stärke nur in Umgebungen mit klarem Trend. Am besten geeignet für Trendbewegungen auf Tagesbasis oder höher; unterhalb der Stundenebene sind die Ergebnisse schlechter.

Risikohinweis: Historische Backtests garantieren keine zukünftigen Erträge. Die Wellentheorie selbst enthält eine gewisse Subjektivität. Selbst mit objektivierten Erkennungsmethoden besteht immer ein Fehlinterpretationsrisiko. Es wird empfohlen, die Signale mit anderen technischen Indikatoren zu bestätigen und die Stop-Loss-Disziplin strikt einzuhalten.

/*backtest

start: 2025-08-01 00:00:00

end: 2025-12-02 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mbedaiwi2

//@version=6

strategy("Elliott Wave Full Fractal System Clean", overlay=true, max_labels_count=500, max_lines_count=500, max_boxes_count=500, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=5, commission_type=strategy.commission.percent, commission_value=0.1, slippage=2)- 1