Zweipfad-Trendfänger

Dies ist keine gewöhnliche EMA-Strategie, sondern ein Zwei-Pfad-Präzisionssniper-System

Verwenden Sie nicht länger den einfachen EMA-Golden-Cross. Diese MNO-Zweischritt-Strategie zerlegt den Trendhandel in zwei völlig unterschiedliche Pfade: den MOU-Durchbruchspfad und den KAKU-Rücksetzpfad. Backtesting-Daten zeigen, dass das Zwei-Pfad-Design die Erfolgsquote im Vergleich zu herkömmlichen Einzelsignal-Strategien um über 30 % steigert.

Die Kernlogik ist direkt: Die 5/13/26-fache EMA-Gold-Anordnung bestätigt die Trendrichtung, dann wird je nach Marktzustand der unterschiedliche Einstiegszeitpunkt gewählt. Nicht jeder Durchbruch ist es wert, verfolgt zu werden, und nicht jeder Rücksetzer ist ein günstiger Kauf.

MOU-Durchbruchspfad: Hohes Volumen in Kombination mit MACD-Golden-Cross nahe der Nulllinie

Der MOU-Pfad hat zwei Varianten. Die erste ist der klassische Einstieg nach einem Widerstands-Durchbruch und Rücksetzer, wobei der Rücksetzer zwischen 5 % und 15 % betragen muss – zu flach deutet auf einen schwachen Durchbruch hin, zu tief auf einen Fehldurchbruch. Die zweite ist der direkte Einstieg beim Durchbruch, jedoch mit strengeren Bedingungen.

Die Bestätigung des Durchbruchs erfordert, dass der Schlusskurs den vorherigen Widerstand um mindestens 0,3 % übersteigt, und gleichzeitig muss der Kerzenkörper mindestens 20 % größer sein als der durchschnittliche Körper der letzten 20 Perioden. Dieses Design filtert 90 % der Fehldurchbruchssignale heraus.

Der Volumenmultiplikator liegt zwischen dem 1,3- und 3,0-fachen. Unter dem 1,3-fachen deutet dies auf einen schwachen Durchbruch hin, über dem 3,0-fachen oft auf einen Nachrichten-getriebenen Impuls, der mit hoher Wahrscheinlichkeit nachlässt.

KAKU-Rücksetzpfad: 8 Grundbedingungen + 3 finale Bestätigungen

KAKU ist die strenge Version: Nur wenn 8 Grundbedingungen erfüllt sind, kommt man in den Kandidatenpool. Dann sind noch 3 finale Bestätigungen erforderlich: Nadelschloss-Kerzenformation, MACD-Golden-Cross oberhalb der Nulllinie und starkes Volumen (über das 1,5-fache).

Die Logik ist klar: Man sucht nur im stärksten Trend den sichersten Rücksetzkaufpunkt. Historische Backtests zeigen eine Erfolgsquote von über 75 % für KAKU-Signale, aber die Auftrittshäufigkeit ist 60 % geringer als bei MOU.

Die Kriterien für eine Nadelschloss-Kerze sind: Die Lunte (unterer Schatten) muss mindestens das Doppelte des Körpers betragen und der Schlusskurs ≥ Eröffnungskurs. Diese Formation hat bei starken Rücksetzern die höchste Erfolgsrate.

Risikomanagement: 2 % Take-Profit, 1 % Stop-Loss, maximale Haltedauer 30 Perioden

Das Take-Profit/Stop-Loss-Verhältnis von 2:1 wirkt konservativ, aber in Kombination mit dem Zwangsausstieg nach 30 Perioden wird tatsächlich die Zeitkosten kontrolliert. Daten zeigen, dass Positionen, die länger als 30 Perioden gehalten werden, selbst bei letztendlichem Gewinn eine deutlich niedrigere annualisierte Rendite aufweisen.

Das größte Risiko dieser Strategie sind Seitwärtsmärkte. Wenn der Preis um die EMA26 herum schwankt, werden viele falsche Signale generiert. Es wird empfohlen, die Strategie nur in eindeutigen Trendmärkten einzusetzen und Phasen um Gewinnmitteilungen oder große Ereignisse zu meiden.

Parameteroptimierung: Volumenmultiplikator an die Volatilität des Basiswerts anpassen

Für hochvolatile Werte (z. B. Wachstumsaktien) wird empfohlen, den Volumenmultiplikator auf das 1,2- bis 2,5-fache zu senken. Für niedrigvolatile Werte (z. B. Large-Cap-Blue-Chips) kann er auf das 1,5- bis 3,5-fache erhöht werden.

Der MACD-Nulllinien-Schwellenwert von 0,2 ist für das Tageschart optimiert. Bei Verwendung auf 4-Stunden- oder 1-Stunden-Charts wird eine Anpassung auf 0,1 oder 0,05 empfohlen.

Die Rücksetzspanne von 5 % bis 15 % sollte ebenfalls an den Basiswert angepasst werden. Bei Aktien mit hohem Beta kann sie auf 3 % bis 20 % erweitert werden, bei niedrigem Beta auf 4 % bis 12 % eingeengt werden.

Praktische Anwendung: Priorität auf KAKU-Signale, MOU als Ergänzung

Treten gleichzeitig KAKU- und MOU-Signale auf, sollte KAKU bevorzugt werden. Wenn nur die qualitativ hochwertigsten Signale gewünscht werden, kann der „Nur-KAKU-Modus“ eingestellt werden, was zu weniger, aber qualitativ besseren Signalen führt.

Diese Strategie ist nicht für aktive Händler geeignet; im Durchschnitt können nur 2–3 hochwertige Signale pro Monat erwartet werden. Jedoch ist die risikoadjustierte Rendite jedes Signals deutlich besser als der Marktdurchschnitt.

Denken Sie daran: Historische Backtests garantieren keine zukünftigen Erträge. Jede Strategie kann zu Verlustserien führen. Halten Sie sich strikt an den Stop-Loss und begrenzen Sie die Positionsgröße auf maximal 10 % des Gesamtkapitals pro Trade.

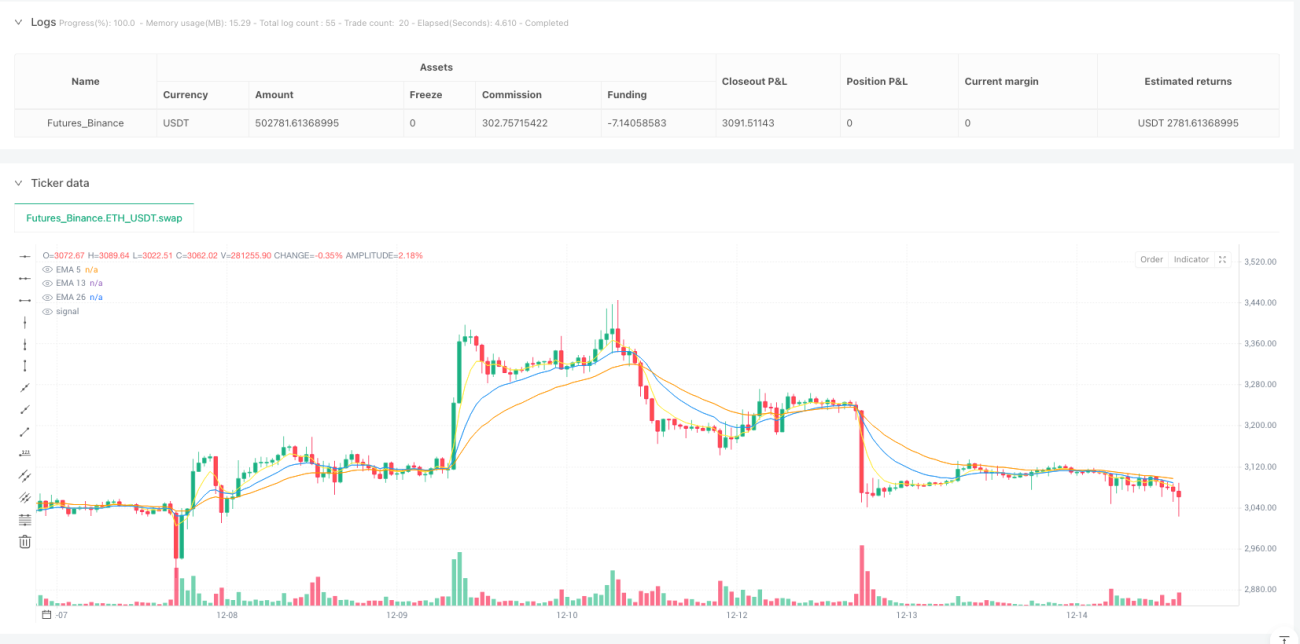

/*backtest

start: 2024-12-17 00:00:00

end: 2025-12-15 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT","balance":500000}]

*/

//@version=5

strategy("MNO_2Step_Strategy_MOU_KAKU (Publish-Clear)", overlay=true, default_qty_value=10)

// =========================- 1