RSI Dual-rail Oscillation Line Long and Short Bi-directional Trading Strategy

Overview

The RSI Dual-rail Oscillation Line Long and Short Bi-directional Trading Strategy is a bi-directional trading strategy utilizing the RSI indicator. It implements efficient bi-directional opening and closing of positions through the overbought and oversold principles of RSI, combined with dual-rail settings and moving average trading signals.

Strategy Logic

The strategy mainly makes trading decisions based on the overbought and oversold principles of the RSI indicator. It first calculates the RSI value vrsi, as well as the upper rail sn and lower rail ln of the dual rails. A long signal is generated when the RSI value crosses below the lower rail ln, and a short signal is generated when the RSI value crosses above the upper rail sn.

The strategy also detects the rise and fall of candlesticks to further generate long and short signals. Specifically, a long signal longLocic is generated when the candlestick breaks out upwards, and a short signal shortLogic is generated when the candlestick breaks out downwards. In addition, the strategy provides parameter switches to go long only, short only, or reverse signals.

After generating long and short signals, the strategy will count the number of signals to control the number of openings. Different pyramiding rules can be set through parameters. Position closing conditions include take profit, stop loss, trailing stop loss, etc., with customizable profit and loss percentages.

In summary, the strategy integrates RSI indicators, moving average crossovers, statistical pyramiding, stop profit and stop loss and other technical means to achieve automated long and short bi-directional trading.

Advantages of the Strategy

- Utilize the overbought and oversold principles of RSI to establish long and short positions at reasonable levels.

- Dual rails prevent wrong signals. The upper rail prevents premature closing of long positions, while the lower rail prevents premature closing of short positions.

- Moving average trading signals filter false breakouts. Signals are only generated when the price breaks through the moving average, avoiding false signals.

- Count signal and pyramiding times to control risks.

- Customizable profit and loss percentages for controllable profitability and risk.

- Trailing stop loss to further lock in profits.

- Go long only, short only or reverse signals to adapt to different market environments.

- Automated trading system reduces manual operation costs.

Risks of the Strategy

- RSI reversal failure risk exists. RSI entering overbought or oversold zones does not necessarily reverse.

- Fixed take profit and stop loss risks being trapped. Improper settings may cause premature stop loss or profit taking.

- Reliance on technical indicators has optimization risks. Improper indicator parameters negatively impact strategy performance.

- Simultaneous triggering of multiple conditions risks missing trades.

- Automated trading systems have abnormal error risks.

To address the above risks, parameters can be optimized, stop profit and loss strategies can be adjusted, liquidity filters can be added, signal logic can be improved, and exception monitoring can be increased.

Optimization Directions

- Test parameter optimization of RSI parameters on different timeframes.

- Test different take profit and stop loss percentage settings.

- Add volume or profitability filters to avoid insufficient liquidity.

- Optimize signal logic and improve moving average crossovers.

- Backtest across multiple time periods to verify stability.

- Consider adding other indicators to improve signal quality.

- Incorporate position sizing strategies.

- Add exception handling and error monitoring.

- Optimize automatic trailing stop algorithms.

- Consider incorporating machine learning to improve the strategy.

Summary

The RSI Dual-rail Oscillation Line Long and Short Bi-directional Trading Strategy integrates RSI indicators, statistical opening and stop loss principles and other technical tools to achieve automated bi-directional trading. The strategy is highly customizable for users to adapt parameters to different market environments. There is also room for improvement via optimizing parameters, risk management, signal logic etc. Overall, it provides an efficient quantitative trading solution.

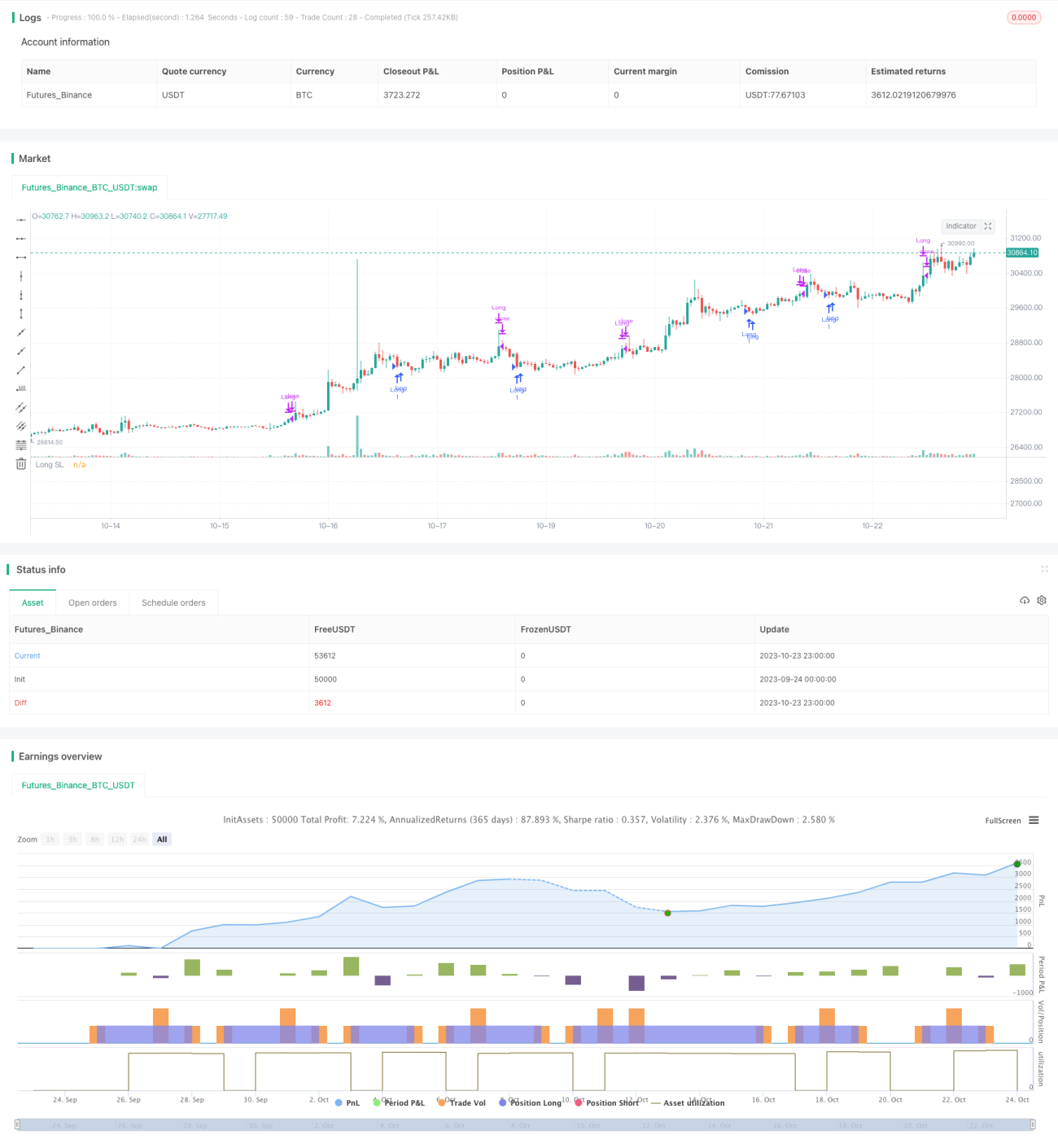

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// Learn more about Autoview and how you can automate strategies like this one here: https://autoview.with.pink/

// strategy("Autoview Build-a-bot - 5m chart", "Strategy", overlay=true, pyramiding=2000, default_qty_value=10000)

// study("Autoview Build-a-bot", "Alerts")- 1